By Rob Williams, Director of Research, Sage Advisory

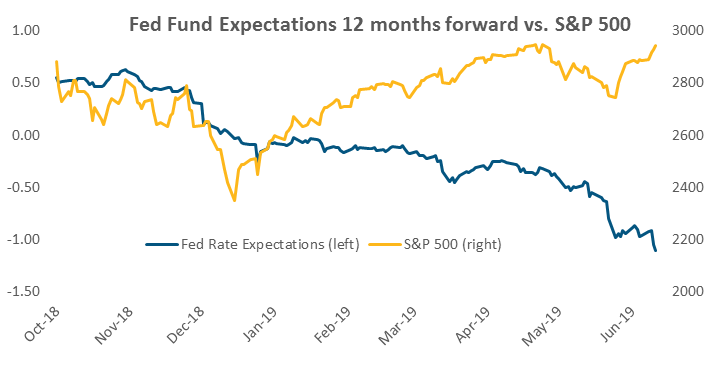

Policy Pivot and Markets

The Fed and the other major central banks have turned decidedly dovish in the face of trade concerns and a more obviously weakening global economy. This has bolstered risk markets and sent global rates falling. We believe this trend is likely to continue in the near-term, as the policy shift has been dramatic and central bank dialogue has highlighted the commitment to easing and stimulus as needed.

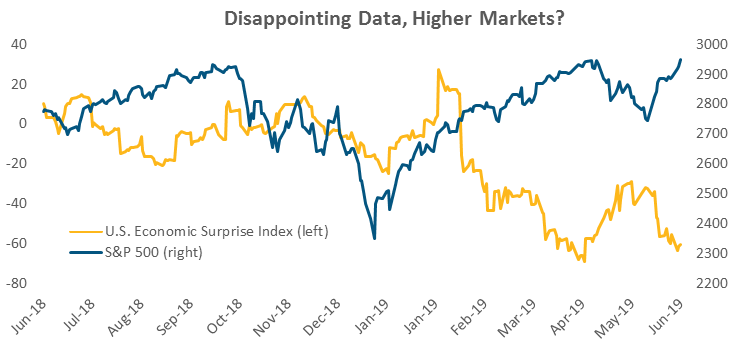

Bad is Good Again

We appear to be entering a period we have become all too familiar with in this recovery; one where bad data equals good returns – all due to policy expectations. As shown below, economic data has been surprising to the downside while the S&P 500 keeps climbing. This suggests staying risk-on in the near-term. Unfortunately for investors, the difficult questions have yet to be answered. Namely, is this policy shift a temporary boost that will reverse the economic slowdown, or the beginning of a long easing cycle to manage us through a recession?

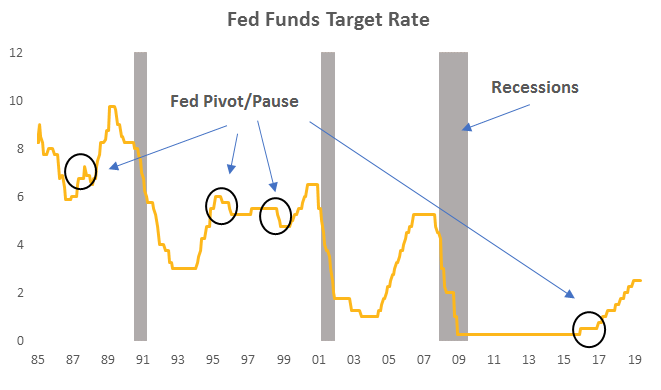

Pivot vs. Precursor to Recession

Only time and the evolution of data will give us the true answer, but we can look back and see some historical precedence as to when the Fed paused or eased temporarily between tightening regimes. Over the last 40 years we have had three easing cycles, which were all associated with recession. We have also seen the Fed pivot four times in response to market and economic stress.

Good for Bonds Either Way, but Risk Asset Outcomes Diverge

Examining historical returns of these two types of easing periods highlights the fact that bonds benefit from easing, no matter the outcome. But the fate of risk assets is ultimately tied to the ability policy has to affect the actual data.

Conclusion – Hold the Door

While we would not be hitting the exit button with respect to risk assets at this time, given policy support, we would keep the door cracked open and ready for an exit. Although we expect easing policy to affect asset prices, we are skeptical that it will have any meaningful impact on actual growth. Global rates are already low, and shaving even 100 basis points off rates over 12 months is unlikely to be a game changer. If risk markets continue to push higher on policy optimism in the face of poor global growth momentum, we would view this as a good opportunity to lower risk.

This article was written by Rob Williams, Director of Research at Sage Advisory, a participant in the ETF Strategist Channel.

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our web site at www.sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.