Stringer Asset Management: Annual 2022 Client Video from Stringer Asset Management on Vimeo.

Overall, we are optimistic about the U.S. economy going into 2022. While we have no way of accurately forecasting the direction the pandemic will take, we have seen that the economic impact of each successive wave has been smaller than the one before. Assuming that this trend continues, we largely look past COVID headlines to focus on economic fundamentals and valuations to find attractive risk-adjusted opportunities. Our collection of near-term indicators suggests U.S. economic momentum will continue over the coming year. Our view on foreign economies is more mixed and dependent upon the specific circumstances of each country and region.

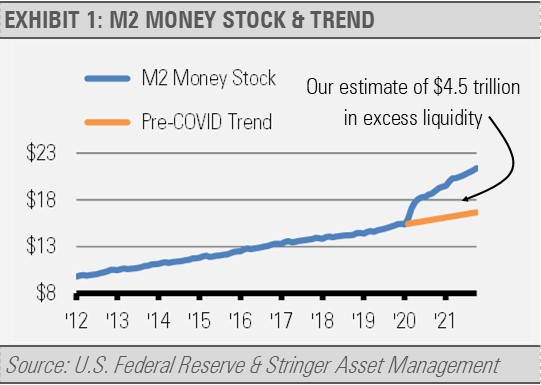

We think that the Fed has fallen behind the curve and will have to raise interest rates persistently over the coming years. The unemployment rate has been falling precipitously for months and dropped to 3.9% in December. By the time the unemployment rate fell to 3.9% during the previous business cycle, the Fed had already increased short-term interest rates by nearly 2% over the course of more than two years. While the Fed continues to purchase Treasury bonds and agency mortgage-backed securities as the last remnants of its Quantitative Easing policy to stimulate economic growth and help with the COVID pandemic recovery, the U.S. financial system already has an excess of $4.5 trillion in liquidity. This is equal to nearly 20% of the size of the entire U.S. economy.

Though M2 liquidity growth, which is currency and coins held by the non-bank public, checking accounts, savings accounts, and retail money market mutual funds, has slowed markedly after the cessation of most of the Fed’s stimulus programs, it is still growing at 13% year-over-year. That pace of liquidity growth is more than double the previous cycle average of 5.9%.

Even if the Fed begins to tighten monetary policy sooner and more persistently than had been previously anticipated, as the minutes from the December Federal Open Markets Committee meeting imply, inflation is still likely to persist. Our work suggests that the Fed is well behind the curve and will end up raising interest rates to a level higher than would have been the case otherwise. Given its history of raising interest rates incrementally over time, we expect that the Fed rate hikes will continue well into 2023.

Some of the biggest challenges facing the economy today are supply chain shortages, which includes a lack of workers. The Fed cannot do anything about those issues. With the economy operating close to its full potential and the tight labor market contributing to wage pressures, excess liquidity should ultimately lead to more inflation and higher asset prices.

Still, the U.S. economy has plenty of strength and momentum to be able to absorb the coming rate hikes at least for the next year or more. Persistent U.S. economic growth should result in higher household income and higher corporate earnings overall.

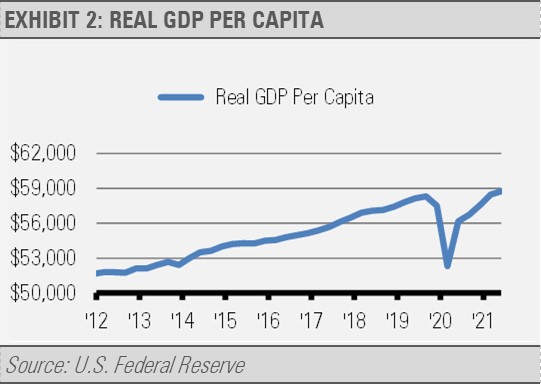

We think that economic growth is strong enough to continue fueling these positive trends. For example, economically speaking, the standard of living is driven by per capita real, inflation-adjusted, economic growth. Essentially, it’s the growth in national income per person, adjusted for inflation. As the following graph illustrates, per capita real GDP has fully recovered from the COVID pandemic induced recession and is now the highest it has ever been in U.S. history. As a result, the aggregate standard of living in the U.S. is the highest it as ever been from an economic perspective.

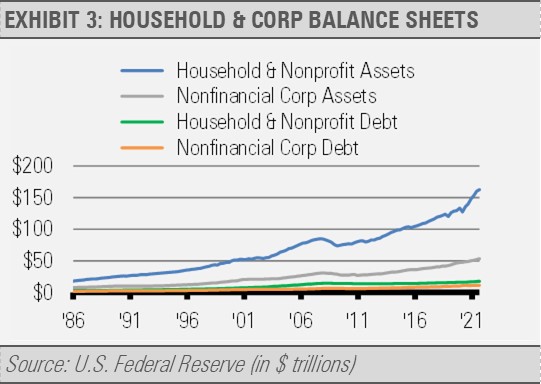

As it stands, business and household balance sheets are in great shape. Net worth, which is assets minus liabilities, for households and nonfinancial corporations are at all-time highs (exhibit 3). Much discussion has been made about the amount of debt in the U.S. financial system, but assets have grown even faster. As a result, both household and nonfinancial corporate net worth are at record levels. Our nation has never been wealthier than it is today. In short, both the corporate and household sectors are in great shape to propel economic growth forward and ride out any storms that may come along the way.

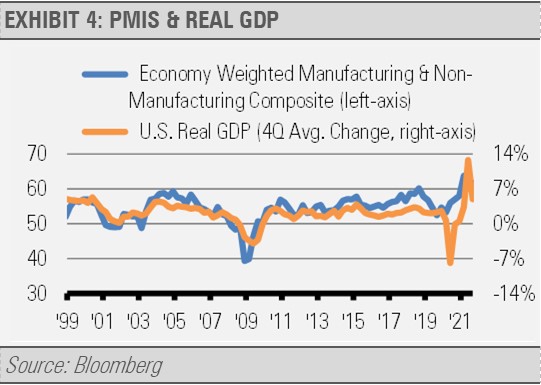

Other leading economic indicators that we track, such as Purchasing Manager Indices (PMIs), continue to look strong with the service sector PMI readings just off its all-time high (exhibit 4). In addition, the prices of industrial metals continue an uptrend. This would not likely be the case if the global economy was on the verge of a downturn as a drop in demand would push these prices down not up. These indicators suggest that U.S. economic growth will continue.

INVESTMENT IMPLICATIONS

Overall, we think that U.S. equity prices appear stretched by almost any measure. The lack of significant volatility in the equity markets may be an additional cause for concern. However, given the fundamental strength in the economy, we think that these factors reduce return expectations for the year ahead rather than forecasting an outright decline. We would use pockets of volatility as an opportunity to add to equity positions.

Our work suggests that we are in the middle part of the current economic business cycle. The first phase is characterized by the cyclical rebound. The second phase, which is where we think we are now, is when the pace of growth slows towards the long-term trend. During this phase of the cycle, we want to emphasize quality earnings while paying attention to valuations.

Specifically, we favor the information technology, financials, and health care sectors. We think that each of these sectors has quality earnings potential and the latter two are especially attractive based on current valuations.

On the fixed income side, we expect the 10-year Treasury yield to rise above 2% as economic growth and inflation persist in the years to come. We anticipate that short-term interest rates will move up at a faster pace and by a greater magnitude than long-term interest rates. As a result, we are selectively focused on floating and variable rate securities on the short-end of the curve as well as high quality corporates, mortgage-backed, and asset-backed securities in the 3-year to 5-year range.

Though U.S. equity market and bond valuations appear stretched in aggregate, we are finding opportunities in areas that we think can deliver in this shifting environment. These include equity sectors with quality earnings as well as floating rate short-term and intermediate duration high quality fixed income.

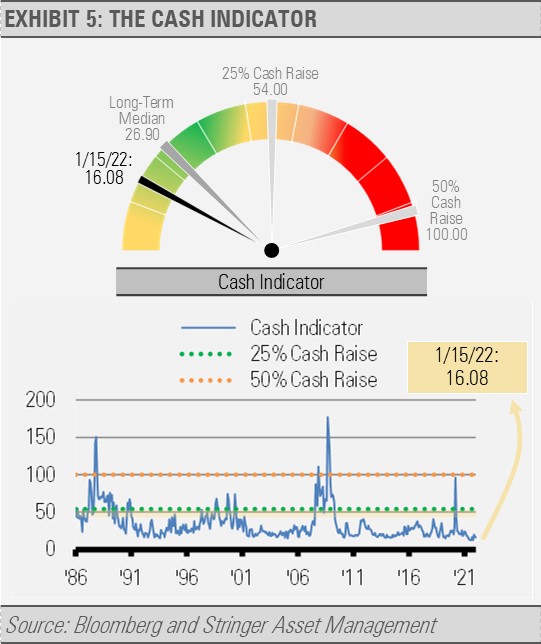

THE CASH INDICATOR

Recent volatility has shifted the Cash Indicator (CI) around the low end of its normal range, which suggests some complacency in markets.

Complacency tends to lead to increased volatility. Overall, we remain fully invested and we are seeing tactical opportunities to both manage risk and take advantage of potential for gains.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not be taken as an advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.