With the backdrop of U.S. Federal Reserve (Fed) headlines in addition to the shifting narratives of the election season, we have been focusing on what we are calling the Great Normalization as overall economic trends in the U.S. are getting back to normal. More than three years after the last pandemic related stimulus package, the U.S. continues to emerge from the unprecedented economic disruptions caused by the COVID-19 pandemic and the accompanying government interventions.

The Great Normalization encompasses the gradual return to pre-pandemic economic norms despite significant structural changes and new challenges to navigate. As we move forward, we expect a more measured economic environment with key indicators, such as GDP growth, jobs creation, and inflation, trending towards historical averages.

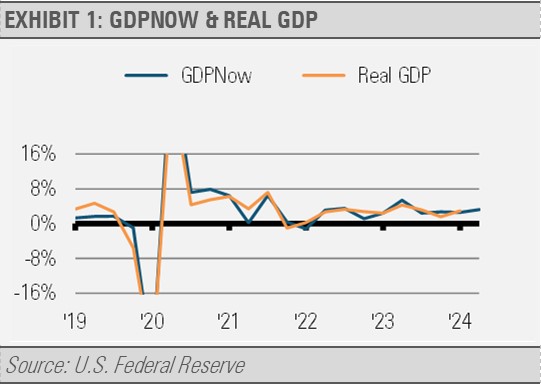

We can see economic growth trending towards a more normal rate through both the Federal Reserve Bank of Atlanta’s GDPNow, which attempts to measure economic growth in real time, as well as the official GDP numbers that are published with a lag. As the graph below shows, following the steep drop and dramatic recovery, measures of broad economic activity have been stabilizing around a healthy rate of growth.

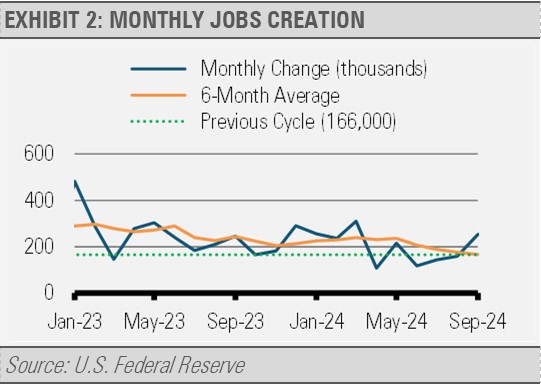

In addition to analyzing monthly employment reports, we track monthly jobs creation on a rolling 6-month average to smooth out the volatility around the monthly figures. The following graph shows jobs creation slowing recently and getting back to the approximately 166,000 new jobs per month average of the previous business cycle from July 2009 through February 2020.

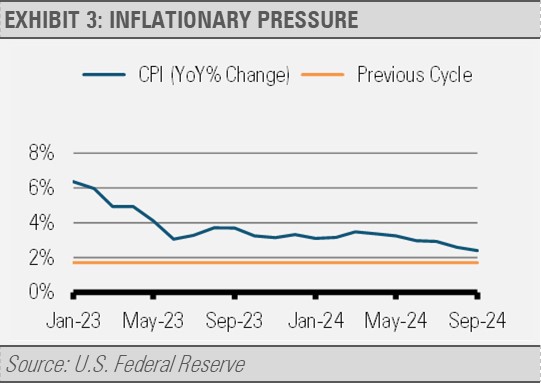

Similarly, we are seeing inflationary pressure normalizing as well. While the current business cycle average may end up being higher than the previous cycle’s 1.7% due to the massive domestic industrial buildout in the United States, annual inflation of roughly 2.5%-3.0% that we expect would be consistent with longer-term U.S. history.

A central aspect of this normalization process is our expectation of a reduction in government involvement in the economy. After unprecedented interventions, the Fed has recently embarked on what we think will be a gradual path to lower short-term interest rates to more typical levels. We also anticipate a deceleration in fiscal spending growth, which potentially leads to a decrease in federal expenditures as a percentage of economic activity over time.

The private sector, including businesses and households, is poised to take a leading role in driving economic growth during this normalization period.

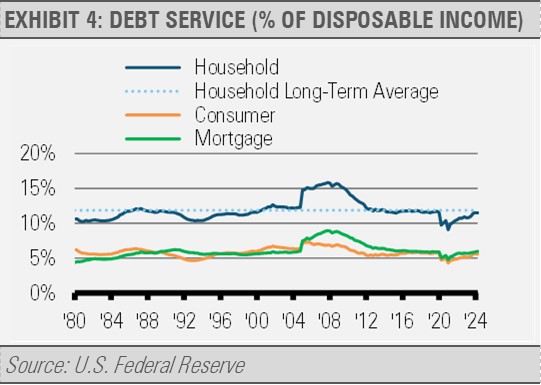

Personal income growth continues to outpace the rate of inflation while household debt levels are generally manageable, particularly outside the lowest income quintile. Healthy household balance sheets and rising incomes leave plenty of room for consumer spending.

The following graph shows the percentage of disposable (after-tax) income that households dedicate to servicing specific types of debt. The graph has four lines: the green line shows mortgage debt, the orange line shows consumer debt (credit card, auto, and personal loans), and the navy line shows household debt service (the sum of the green and orange lines) while the dashed line is the average of this calculation since 1980. Financial burdens vary based on the principal amount as well as interest rates on the debt. Household debt service (the navy line: mortgage debt plus consumer debt) has increased recently towards the long-term average with the economy reopening. Still, the current household debt ratio is well below the highs seen in the 2000s and leaves room for further economic expansion near historical rates.

Corporate balance sheets are similarly robust, especially among larger firms. This should lead to a continuation of the significant investments in plant and equipment, as well as research and development currently underway. Together, these datapoints suggest strong future economic growth prospects.

However, the normalization process is not without its challenges and disparities. Recent data from the global Purchasing Managers’ Index reports indicate a widening gap between the global manufacturing and service sectors. While service providers, particularly in healthcare and finance, are experiencing accelerating growth, the global manufacturing sector continues to face headwinds with contractions in output, new orders, and employment.

Geographically, economic performance varies significantly. Countries like India and the United States are showing strong growth, while others, such as Germany and Canada, are experiencing economic contractions or stagnation. This uneven recovery underscores the complex nature of the global economic landscape.

The Great Normalization represents a critical phase in the U.S. economic recovery characterized by a rebalancing of public and private sector roles, a moderation of extreme policy measures, and a gradual return to more sustainable economic patterns. While challenges remain, particularly in addressing sectoral and geographic disparities, the overall trajectory suggests a move towards a more stable and predictable economic environment.

INVESTMENT IMPLICATIONS

As this process unfolds, we are finding a substantial number of attractive investment opportunities in high quality U.S. equities and fixed income, as well as foreign companies that pay consistent dividends. We believe that it will be essential for investors to remain adaptable and responsive to the evolving economic landscape. This changing environment is a focus of our Three Layers of Risk Management process as we continue to manage risk in real time.

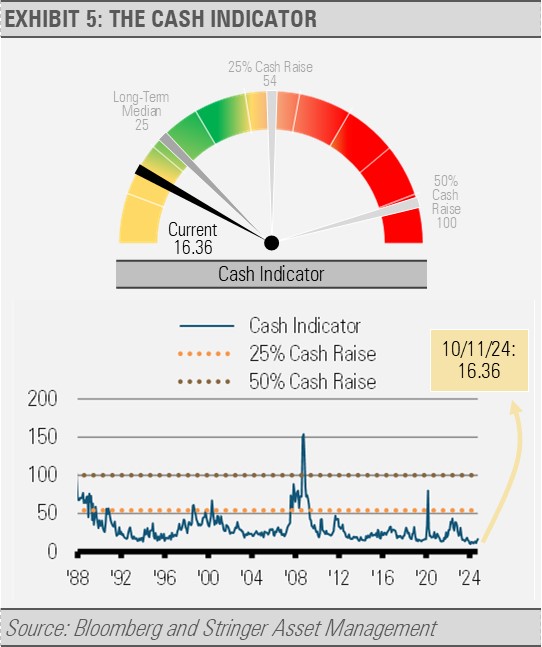

CASH INDICATOR

The Cash Indicator (CI) level has increased recently but remains below historical norms. The increase reflects an uptick in equity market volatility that has gone from well below historical averages to moving back in line with typical equity markets. Holding the CI below historical norms are persistently tight credit spreads. By this measure, the bond market may be overly complacent. Still, with a positive economic backdrop, we view downside volatility as a buying opportunity.

For more news, information, and strategy, visit the ETF Strategist Channel.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.