The yield curve measures the difference between short-term, intermediate-term, and long-term Treasury yields. Typically, short-term yields are lower than long-term yields. Occasionally, this relationship is reversed though these instances are usually brief. The current yield curve inversion is the longest on record and seems to be nearing an end.

Higher short-term interest rates have been the catalyst for a large amount of assets flowing into short-term money market funds and Treasury bills.

Additionally, bond investors are currently in a difficult position as they attempt to play off the Fed’s shifting policies and mixed macroeconomic data. This presents the question of when will the yield curve normalize and what does the path back look like?

Using the popular 10-year Treasury yield compared to the 2-year yield, we can see the yield curve is getting closer to normal. Recently, the yield on the 2-year Treasury has fallen faster than the yield on the 10-year Treasury. However, with a historical average spread of roughly 0.86%, this measure of the yield curve still has much farther to go before being considered “normal.”

Our base-case scenario represented below suggests that short-term yields will continue to fall faster than long-term yields as the expected Fed interest rate cuts become a reality. We think this process will probably take at least a year, and likely closer to two years given that the Fed will almost certainly reduce rates incrementally over that time. With longer-term rates close to fairly priced, we would expect long rates to anchor near current levels as illustrated below.

Notably, the yield curve began to adjust before the Fed initiated interest rate cuts. For example, between April 30th and September 6th, the 2-year Treasury yield declined 1.38% while the 5-year yield fell 1.22% and the 10-year yield eased 0.97%. Meanwhile, shorter-term interest rates, such as the 3-month and the 1-year Treasury, have fallen only 0.33% and 0.75%, respectively. From here, we think markets are likely to push these shorter-term yields down faster than the 2-year, 5-year, and 10-year yields as Fed rate cuts come into effect.

Looking ahead, slower jobs growth and slowing inflation give the Fed more leeway to reduce short-term interest rates. The market is now pricing in at least 0.75% in rate cuts before the end of 2024, which would reduce short-term interest rates and money market yields by a similar amount.

As yields on these shorter-term instruments as well as money markets decline, we think the 5-year bond yield looks attractive as this income should prove to be more stable. Also, a further decline in yields going forward should result in continued capital appreciation for intermediate fixed income investments in addition to the still attractive yields they offer.

For example, while money market funds pay attractive yields today, the income provided by these funds should drop precipitously as soon as the Fed begins to lower interest rates. Conversely, allocations to investment grade intermediate fixed income are unlikely to see a significant reduction in current income when the Fed cuts rates. This positioning exhibits more income stability because these investments have locked in today’s attractive rates for a longer period of time.

INVESTMENT IMPLICATIONS

While holding assets in money market funds or T-Bills has its merits, our Three Layers of Risk Management framework leads us to additional opportunities that have the potential for attractive gains and principal protection.

Our work suggests that the investment grade fixed income space looks attractive. We think core intermediate duration fixed income is set to offer attractive returns for years to come. Within that space, we favor defined maturity Treasury and corporate bond ETFs.

On the equity side, our allocations are tilted towards high quality U.S. and foreign equities that exhibit consistent earnings and low financial leverage as well as more defensive dividend payers. Finally, in the alternative space, we are allocated to equity option strategies that overlay U.S. blue-chips to either enhance current yield or offer downside protection.

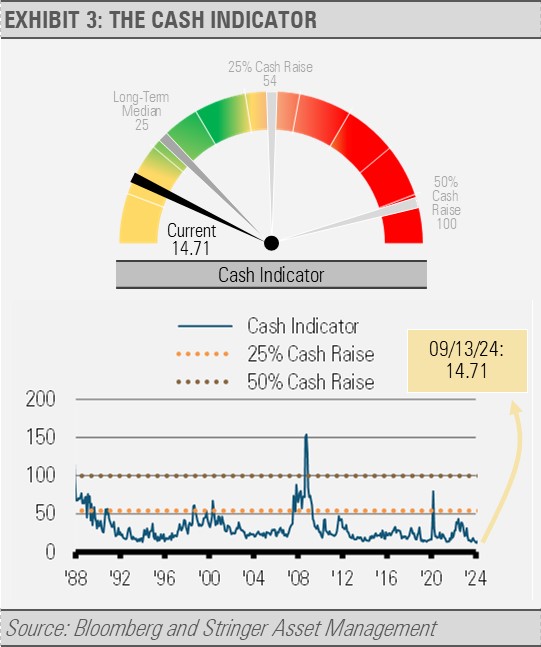

CASH INDICATOR

While the Cash Indicator (CI) has risen recently in light of increased equity market volatility, the level remains below historical norms. With the backdrop of continued economic growth, we view equity market drawdowns as opportunities to increase investments in high quality businesses.

For more news, information, and strategy, visit the ETF Strategist Channel.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.