By Kevin Nicholson, CFA, Global Fixed Income CIO | Co-Head of Investment Committee

SUMMARY

- Now is the time to begin adding fixed income, in our view.

- Our balanced portfolios now hold Treasuries, investment grade bonds, and high yield.

- We are combining the assets to increase yield and enhance protection.

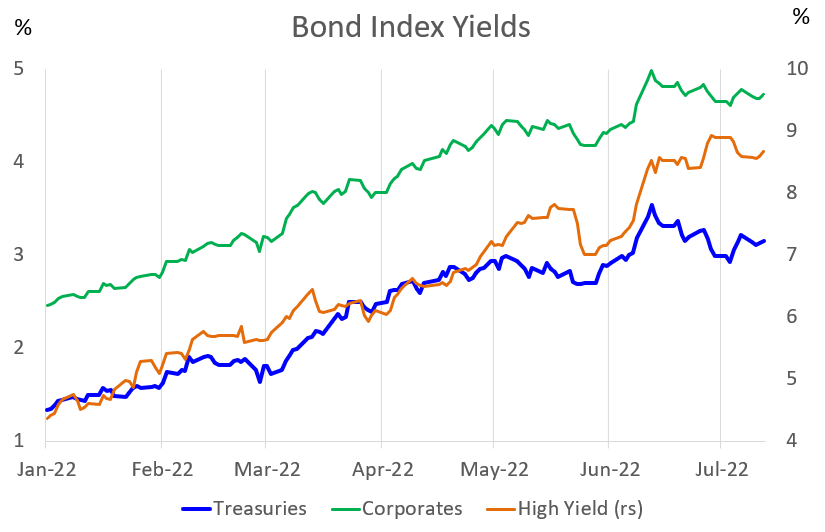

Since the start of the year, yields have more than doubled across most of the yield curve. During this time, our portfolios have maintained a significant underweight to fixed income vs. our comparable benchmarks and carried elevated cash. However, as yields have risen above 3% and the yield curve has flattened due to the Federal Reserve’s (Fed) commitment to fight inflation, we believe that fixed income is once again attractive. Thus, we think that the time has come to begin adding fixed income back to our portfolios.

Source: RiverFront, Factset. Chart shown for illustrative purposes only. Past performance is no guarantee of future results. Not indicative of RiverFront portfolio performance. Data as of 7.15.22.

Our portfolios have employed different strategies to gain exposure to fixed income this year, depending on the time horizon and risk tolerance of the portfolio. The short-horizon portfolios focused on investment grade corporate bonds with maturities of five years or shorter in combination with senior loans to gain exposure to fixed income when Treasuries and longer maturity corporates were deemed unattractive for shorter-term investors. Conversely, the longer horizon portfolios used a barbell approach, pairing short maturity high yield bonds and senior loans, with long maturity Treasury bonds to mitigate the equity exposure of the portfolios. Two different approaches with the same objective – to generate income and provide risk mitigation from price depreciation.

Fast forward to today, the landscape and our perception of fixed income returns has changed, resulting in the need to adjust our portfolio positioning. We think Fixed Income now offers the opportunity for respectable income and the potential for price appreciation if a recession is indeed not far away. While much has been written regarding the repricing of Treasuries, the rest of the bond landscape such as investment grade corporate bonds, high yield bonds, and senior loans have all undergone journeys of their own. We endeavor to state our current opinion on each of these fixed income assets in the sections below.

Treasuries:

The first half of the year was defined by both the bond and equity markets moving in the same direction – down. However, as the Fed has turned more hawkish and begun Quantitative Tightening (QT), the two asset classes have become less correlated as it pertains to price movements. Given our stance that equities will remain rangebound at best with pressure to the downside over the next 3 to 6 months, we believe that it is appropriate to gradually add back some longer duration securities, – specifically Treasuries – to act as a shock-absorber during periods of stock market weakness. Currently, we believe the 20-year part of the yield curve offers a better risk/reward relative to the 30-year part of the curve,

We expect macro uncertainty around inflation will likely stoke additional recession fears causing the yield curve over the next couple of months to further invert; the condition when shorter maturity bonds have a higher yield than longer maturity bonds. Under this scenario, we believe that longer maturity Treasuries will outperform as their yields will be capped as the economy slows. Therefore, we believe that it is now important to gain exposure to the long end of the yield curve. Hence, our portfolios that contain fixed income have invested in the long end of the curve recently.

Investment Grade Corporates:

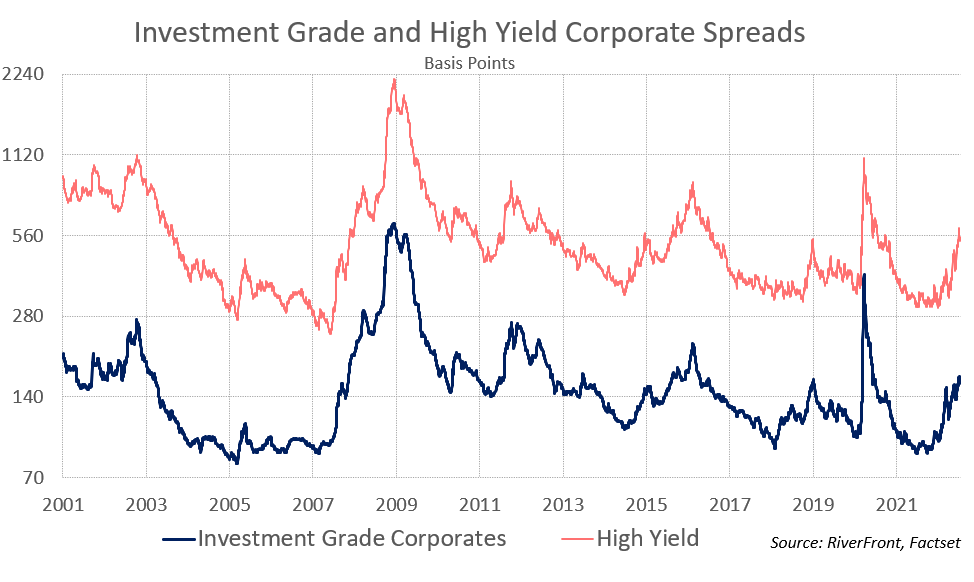

Investment grade corporate bonds began the year yielding a mere 2.36% and as of July 18, 2022 is yielding 4.69%. We believe the increase in yields was mainly driven by the increase in Treasuries and credit spreads, the risk premium to own corporate bonds. Typically, when Treasury yields increase, credit spreads decline if there is not a credit event with the individual company. Many companies took advantage of low interest rates over the last couple of years and thus can put off refinancing at much higher rates for several years. By not having to refinance in the short term most investment grade companies will be less exposed to higher interest rates, which should give them more financial flexibility and stronger credit worthiness, in our view.

At current levels, short maturity corporate bonds provide investors with superior yields without having to extend out maturities, in our opinion. Given that the shorter horizon portfolios are sensitive to large drawdowns during market downturns, we have chosen to use some of the excess cash that the portfolios have been holding to invest in short-term corporates with maturities from 1 to 3 years.

Source: RiverFront, Factset. Chart shown for illustrative purposes only. Past performance is no guarantee of future results. Not indicative of RiverFront portfolio performance. Data as of 7.15.22

High yield Bonds:

High yield bonds much like their investment grade counterparts had a significant change in yields from the beginning of the year until now. At the start of the year, high yield bonds yielded and as of July 18, 2022, they are yielding 8.53%. Yields in the high yield market rose partially due to Treasury yields rising, but to a larger extent due to investors demanding a higher risk premium for lower rated companies, in our view. While the risk premium for high yield bonds may have risen, we do not believe that defaults will rise dramatically if a recession does occur. We believe, much like investment grade companies, high yield companies took advantage of low interest rates in 2020 and 2021 and refinanced debt; meaning that these companies only must worry about their operations for the next couple of years.

Like the strategy employed in the shorter horizon portfolios, our longer horizon portfolios chose to focus on the shorter maturities within the high yield market. Given the Fed’s ability to control the front-end of the yield curve through rate hikes, shorter maturating high yield experienced greater credit spread increases than longer maturities. This market phenomenon allowed the longer horizon portfolios to pick up additional income as short high yield currently yields 8.87% as of July 18, 2022.

Senior Loans:

The one fixed income sector that has been a common element across our portfolios has been senior loans. Senior loans are senior to high yield bonds but are comprised of the same lower rated companies in the high yield universe, meaning that we don’t think we should have to worry about refinancing issues in the near term. Given that we cannot predict when the Fed’s rate hiking cycle will end, we felt that it was appropriate to have a fixed income vehicle in the portfolios that would adjust to rate increases. Senior loans have floating-rate coupons based on the prevailing interest rate environment.

Conclusion:

Opportunities exist in fixed income, and we believe that now is the time to begin adding the asset class back to our portfolios. For the first time in a long time, the balanced portfolios hold Treasuries, investment grade bonds, and high yield. We are combining these assets to increase yield and enhance protection across the strategies, with the longer horizon portfolios taking incremental credit risk in exchange for higher yields.

Important Disclosure Information:

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

All charts shown for illustrative purposes only. Technical analysis is based on the study of historical price movements and past trend patterns. There are no assurances that movements or trends can or will be duplicated in the future.

Index Definitions:

Standard & Poor’s (S&P) 500 Index measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

In a rising interest rate environment, the value of fixed-income securities generally declines.

A basis point is a unit that is equal to 1/100th of 1%, and is used to denote the change in a financial instrument. The basis point is commonly used for calculating changes in interest rates, equity indexes and the yield of a fixed-income security. (bps = 1/100th of 1%)

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero).

Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

Duration is a measure of the sensitivity of the price of a fixed income investment to a change in interest rates. Duration is expressed as a number of years. Rising interest rates mean falling bond prices, while declining interest rates mean rising bond prices.

The federal funds rate is the target interest rate set by the Federal Open Market Committee (FOMC). This is the rate at which commercial banks borrow and lend their excess reserves to each other overnight.

When referring to being “overweight” or “underweight” relative to a market or asset class, RiverFront is referring to our current portfolios’ weightings compared to the composite benchmarks for each portfolio. Asset class weighting discussion refers to our Advantage portfolios.

Investments in international and emerging markets securities include exposure to risks such as currency fluctuations, foreign taxes and regulations, and the potential for illiquid markets and political instability.

High-yield securities (including junk bonds) are subject to greater risk of loss of principal and interest, including default risk, than higher-rated securities.

The Advantage portfolios may be invested in stocks, bonds and exchange-traded products (exchange-traded funds (ETFs) and exchange-traded notes (ETNs)). Advantage is offered through separately managed accounts or on model delivery platforms, depending on the Sponsor Firm.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2022 RiverFront Investment Group. All Rights Reserved. ID 2297753