We anticipated a quiet week in the markets, with limited consequential U.S. economic data, but the Chinese government had other plans. They announced a slew of stimulus measures aimed at revitalizing China’s struggling economy. While these actions may offer some support to the property sector, we remain skeptical about their ability to significantly boost the sluggish consumer demand that has been a persistent drag on growth.

Here are some of the key stimulus measures China introduced in the past week:

- Reserve Requirement Ratio (RRR) Cut: The People’s Bank of China (PBOC) reduced the RRR by 0.5 percentage points, releasing approximately $142 billion into the financial system to boost liquidity and lending capacity.

- Interest Rate Reductions: The PBOC lowered the seven-day reverse repo rate by 20 basis points to 1.5% to reduce borrowing costs. The medium-term lending facility rate was also cut by 30 basis points.

- Property Market Measures: Existing home mortgage rates were reduced by 50 basis points, benefiting about 150 million people. Additionally, the minimum down payment requirement for second homes was lowered from 25% to 15%.

- Capital Market Support: Two new monetary tools were introduced, including a $71 billion swap program to help financial institutions access funds for stock purchases and a re-lending facility offering $42.5 billion in cheap loans to fund share buybacks.

- Potential for Further Easing: The PBOC indicated the possibility of additional easing measures in the coming months if global central banks continue their rate-cut trajectories.

Source: Voice of America (VOA)

Watch the quick video for more on this and keep reading below the video to see other market and economic updates from the week.

Thank you for being here,

Denis Rezendes, Portfolio Manager

The “MSCI EM” Index shown in the video is the MSCI Emerging Markets Index. The MSCI Emerging Markets Index captures large and mid cap representation across 24 Emerging Markets (EM) countries. With 1,328 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country. The countries included are: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Kuwait, Malaysia, Mexico, Peru, Philippines, Poland, Qatar, Saudi Arabia, South Africa, Taiwan, Thailand, Turkey and United Arab Emirates.

Fireside Charts

The Chinese government announced a slew of stimulus measures to prop up the economy over the past week. These announcements sent investors—who had largely abandoned China—rushing back to buy stocks. Looser financial conditions in the U.S. may provide more room for easing in export oriented emerging market countries such as China. Falling mortgage rates in the U.S. are beginning to impact the housing market. Manufacturing and services are telling two different stories about the U.S. economy. S&P 500 earnings growth. AI capital spending.

- Chinese stocks have responded positively to the stimulus measures, but past gains have been short lived:

Source: @JeffreyKleintop

- India recently overtook China as the largest country weight in the MSCI Emerging Market Index:

Source: Gavekal Research

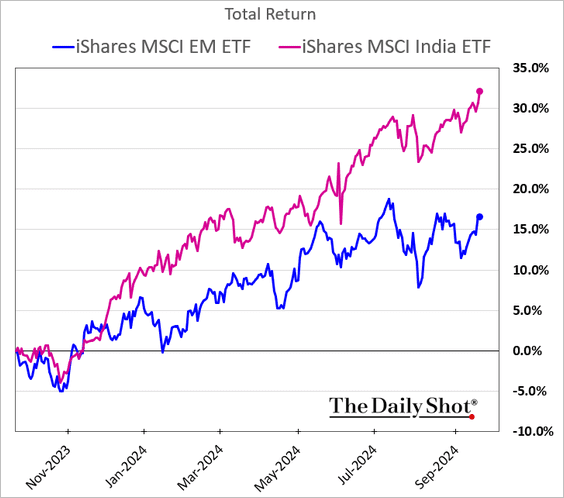

- Indian equities have outpaced those of other countries over the past year:

Source: The Daily Shot 9/23/2024

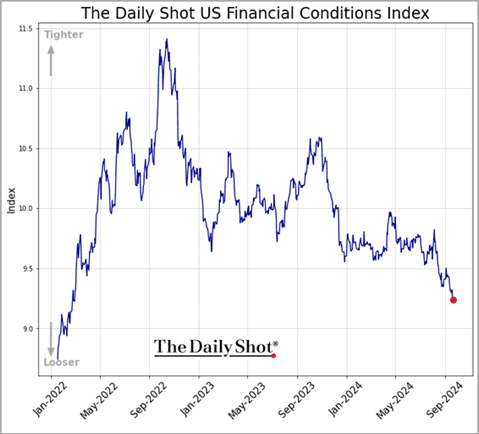

- Falling interest rates further out on the yield curve have had a bigger impact than the recent rate cut on easing financial conditions:

Source: The Daily Shot 9/23/2024

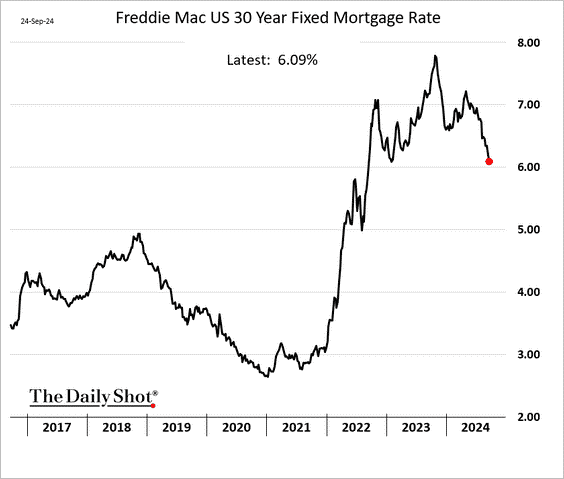

- With rate buydowns and incentives, the rate on some new homes may now be below 5%:

Source: The Daily Shot 9/23/2024

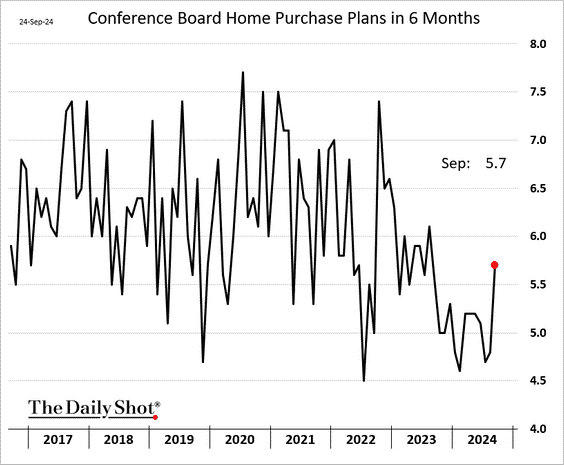

- Plans to purchase a home in the next 6 months jumped in September:

Source: The Daily Shot 9/25/2024

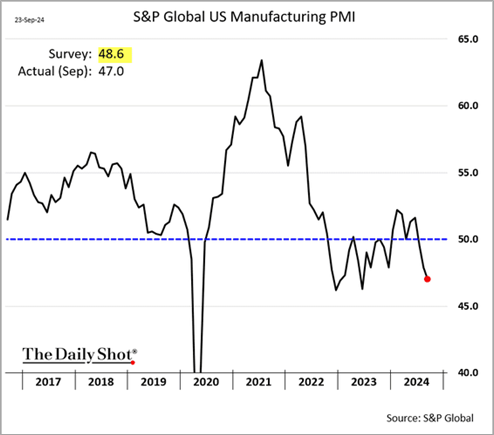

- U.S. Manufacturers are reporting worse business conditions:

Source: The Daily Shot 9/24/2024

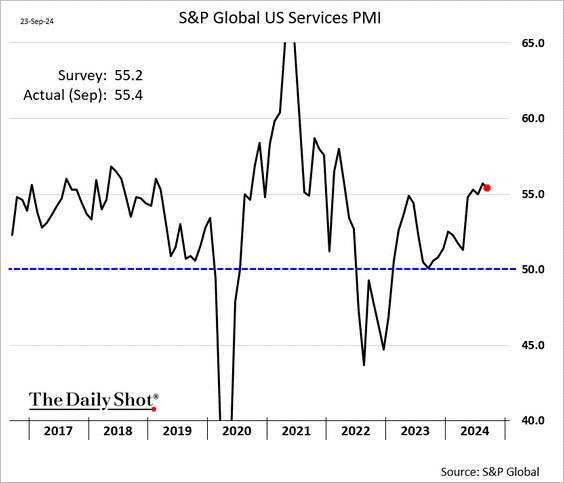

- Thankfully, services are a much larger component of the U.S. economy:

Source: The Daily Shot 9/24/2024

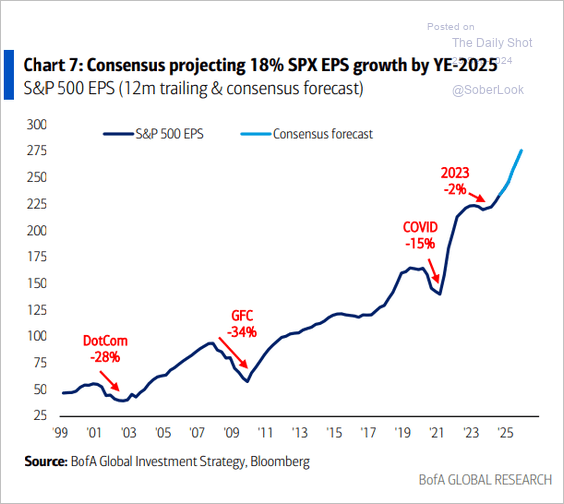

- Analysts believe the S&P 500’s “earnings recession” has come to an end, and are projecting 18% earnings per share (EPS) growth by the end of 2025:

Source: BofA Global Research

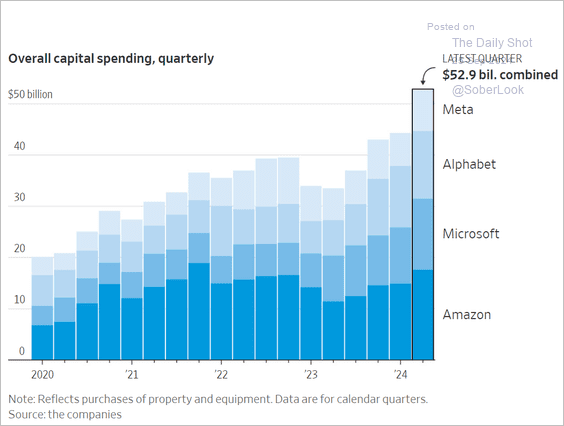

- Capital spending among AI hyperscalers in the U.S. is now running at over $50 billion per quarter:

Source: @WSJ Read full article

By Denis Rezendes, CFA, Partner, Portfolio Manager

For more news, information, and analysis, visit the ETF Strategist Channel.

Disclosure:

Copyright © 2024 Beaumont Capital Management LLC. All rights reserved. All materials appearing in this commentary are protected by copyright as a collective work or compilation under U.S. copyright laws and are the property of Beaumont Capital Management. You may not copy, reproduce, publish, use, create derivative works, transmit, sell or in any way exploit any content, in whole or in part, in this commentary without express permission from Beaumont Capital Management.

Certain information contained herein constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue,” or “believe,” or the negatives thereof or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events, results or actual performance may differ materially from those reflected or contemplated in such forward-looking statements. Nothing contained herein may be relied upon as a guarantee, promise, assurance or a representation as to the future.

This material is provided for informational purposes only and does not in any sense constitute a solicitation or offer for the purchase or sale of a specific security or other investment options, nor does it constitute investment advice for any person. The material may contain forward or backward-looking statements regarding intent, beliefs regarding current or past expectations. The views expressed are also subject to change based on market and other conditions. The information presented in this report is based on data obtained from third party sources. Although it is believed to be accurate, no representation or warranty is made as to its accuracy or completeness.

The charts and infographics contained in this blog are typically based on data obtained from third parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.

As with all investments, there are associated inherent risks including loss of principal. Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Sector and factor investments concentrate in a particular industry or investment attribute, and the investments’ performance could depend heavily on the performance of that industry or attribute and be more volatile than the performance of less concentrated investment options and the market as a whole. Securities of companies with smaller market capitalizations tend to be more volatile and less liquid than larger company stocks. Foreign markets, particularly emerging markets, can be more volatile than U.S. markets due to increased political, regulatory, social or economic uncertainties. Fixed Income investments have exposure to credit, interest rate, market, and inflation risk. Diversification does not ensure a profit or guarantee against a loss.

The federal funds rate is the interest rate at which banks lend money to each other overnight. A treasury yield is the interest rate the U.S. government pays on its debt, and the annual return that investors can expect from holding a U.S. government security.

The Hang Seng Index is a benchmark that reflects the performance of the largest companies listed on the Hong Kong Stock Exchange, providing insights into the health of the Hong Kong economy. The MSCI EM Index measures the equity market performance of emerging markets globally, helping investors gauge investment opportunities and risks in developing economies. The Daily Shot US Financial Conditions Index is a composite indicator that assesses the overall financial conditions in the U.S., incorporating various factors like interest rates and credit spreads to provide insights into market liquidity and risk. The S&P Global US Manufacturing PMI (Purchasing Managers’ Index) measures the economic health of the manufacturing sector by surveying purchasing managers about business conditions, while the S&P Global US Services PMI focuses on the services sector, similarly gauging economic activity based on responses from service sector managers. Earnings per share (EPS) is a financial metric calculated by dividing a company’s net income by its outstanding shares, indicating the profitability of a company on a per-share basis.

Please contact your BCM Regional Consultant for more information or to address any questions that you may have.

Beaumont Capital Management LLC, 125 Newbury St. 4th Floor, Boston, MA 02116 (844-401-7699)