We hope all of you are healthy and safe and implore you to follow the guidance of the local, state and federal authorities. We urge you to stay calm despite a 15% drop in the S&P 500 last week while the number of Coronavirus cases continues to climb. Last week, we covered, “Bad Bond Discounts” while this week we look into the discounts in almost everything.

No Crisis Correlation

The markets have been volatile, dislocated and down no matter the asset class. These types of fire sales happen at the beginning of any crisis. We will cover the market impact on many asset classes and geographies. But first let’s look at how the world markets are responding to this virus crisis. The chart below looks at the top virus outbreaks compared to the market impact:

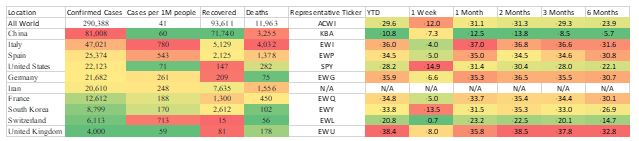

Geographic Comparison of Corona Crisis to Market Returns

As of 3-20-20 source CDC and Morningstar

The key highlight in this chart is the resurgence of the China market as they have managed to get the outbreak under control. This market suffered the same necessary halts to business that we are now also engaging in every major city. China was overwhelmed, accepted reality and did what was crucial. They did it with less infrastructure, more pollution and with minimal economic stimulus, relative to what is proposed in America. The point is, social distancing will work to, “flatten the curve” and save many lives. Government intervention will save the economy. This is an extremely terrible crisis that threatens lives, jobs, businesses and our way of life. As a result of this predicament the world will change, but the final result in a couple of months will be the same; we will return to work, life, love and growth while being smarter, healthier and wiser. This time feels different, but it isn’t. @michael_venuto wanted to share an excerpt from a commentary he wrote in April of 2008:

“This time is different.” I hear this phrase from clients, partners and prospects at least seven times a day. As with any hackneyed phrase, the implications are more diverse then the mundane sentiment inherent in the diction. What they really mean to say is “I have lost confidence” or “why are you not reacting?” or simply “please convince me that the worst is over.” In preparing for this commentary I decided to Google the phrase “this time is different.” I was rewarded with topical, yet typical results. Most of the results refer to the “mortgage crisis”, recession or some other impending doom in our current financial markets. Further down the page I saw a link for an article that touted the technology boom and its sustainability because “this time is different.”

Well, it wasn’t. The tech bubble popped and, as always, emotions subverted logic and valuations reverted to the mean. The most surprising aspect of this little experiment was the fact that “this time is different” has become a financial term. The use of these phrases, analogies and anecdotes by the media fuels the emotional psyche of the market.

Every crisis feels different – they all feel like the end of the world while they are happening. In hindsight they are always less extreme than expected. The end of the world can only happen once, so we choose to bet on a recovery, since consequences of being wrong wouldn’t matter much in an apocalypse.

The second highlight from this, “virus to market” chart above is that the selling is indiscriminate. Meaning the infection rate and the response are not correlating to the specific market performance. South Korea got ahead of this with extreme testing and yet their market is down more than the US. Italy and Spain are dealing with highest cases per million citizens and yet, their markets are only slightly worse than the rest. Markets are rarely rational in times of stress; these markets are responding to an evolving crisis in a media echo chamber with un-trusted government intervention from the local to the executive level. That said, this too will pass.

Risk-Off was Risky

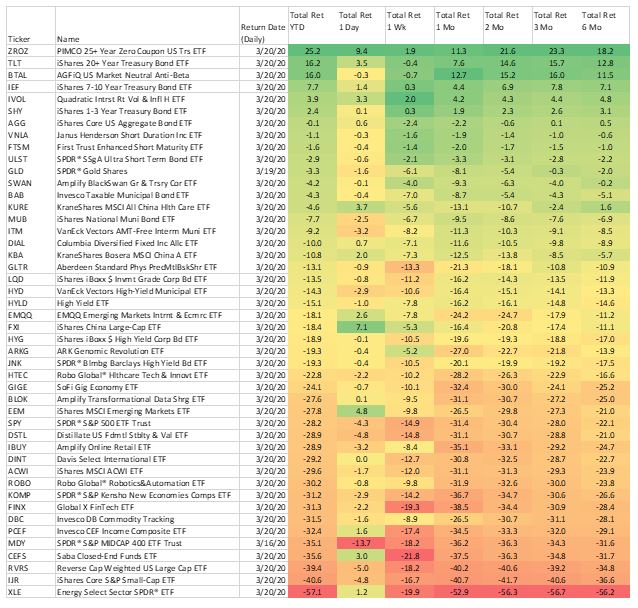

Much of the selling pressure on risk-off assets in the last week were not driven by fundamentals or direct crisis concerns but rather by the need for liquidity. Sell offs resulting from liquidation usually recover quickly, since they don’t require, “buyers”, just the reduction in, “sellers.” We cover the details of the various asset liquidations relevant to many ETF Think Tank members, but first let’s review the performance chart of some commonly held and interesting ETFs:

System Overload

The first area we need to discuss is fixed income. ETFs have taken some blame for shining the light of transparency on the liquidity of fixed income, while as one of our favorite ETF Nerds @Davenadig points out Mutual Funds have been obscuring the true value of the underlying bonds.

Even the long-term treasury sold off last week, which is the most common safe haven asset. All other fixed income assets sold off even more. This is the liquidation cost we discussed above but we should go through them one-by-one and discuss the implications to investment approaches:

- Longer-term fixed income

a. The treasuries went down a little, but more importantly they are no longer going up with inverse correlation to the equity markets. This issue is likely to persist, since the rates can’t really go much lower as they approach negative. - Municipals

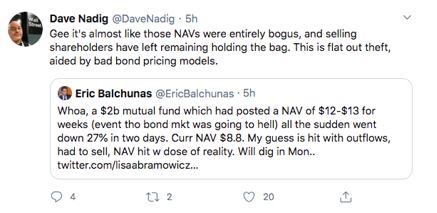

a. All Municipals were down big last week but the Taxable-Munis (BAB) were hit especially hard. The irony is that the Build America Bonds were created to combat the 2008 crisis. The liquidation fire sale left us with desperate price discovery that doesn’t reflect reality. The bond market is generally much less liquid than equities. ETFs act like a cell phone network providing the communication to access these bonds. Just like a cell phone network, the system works very well in times of normal rates of communication. The ETF network normally accesses under 1% of the bond market; in this past week the active and passive market asked for liquidity on over 25% of bonds. The system went to massive discounts and the communication of the net asset value collapsed. This is the same thing that happened to cell phone networks in times of crisis like September 11th or the NYC blackout of 2003. Everybody calling for a bond quote/price got a busy signal and took a discounted guess on the value. These issues, as stated above, usually are repaired quickly. BAB began to price more realistically on Friday.

Another ETF Nerd @NateGeraci pointed out just how extreme the bond liquidations were last week:

- High Yield

a. High Yield experienced a double whammy. They were hurt by the liquidity crisis but more importantly the rout in energy. We are not recommending adding to passive high yield exposure. - Closed End Funds (CEF)

a. The CEF market experienced two forms of liquidation pricing with the underlying bonds trading at discounts and the funds themselves trading at discounts on par with 2008. The liquidity returned on Friday and the recovery began despite negative sentiment in equities. We are extremely bullish on investments opportunistically in the CEF space. These are on sale and we recommend buying selectively. - Short Term Corporates

a. We had another double whammy here with liquidity needs and short-term rates dropping to literally zero. This took a toll on many members with safe haven plays like ULST, FTSM and GSY taking 2% hits. - Gold

a. Gold was down 6% last week in the fire sale. This seems ludicrous in the current environment of stimulus and flights to safety. - Equities

a. Everything went down. This time may not be different, but the successful companies in the changed world will have to embrace different ways of connecting with customers in this era of social distancing. We believe this will bode well for some thematic ETFs that embrace technology, innovation or focus on companies that can help with social distancing.

The ETF Think Tank is Here for You

The ETF Think Tank remains resilient, diligent and we are over-communicating. Advisors called us many times last week and we were here to answer those calls and provide advice and support. The volatility of the markets is depressing and amplified by the very real public health crisis. If we all over-communicate and stay diligent, we will remain strong.