Fixed Income Outlook in 5 Charts

By Komson Silapachai

Stresses from the US regional banking system as well as Credit Suisse have made the outlook for economic growth and Fed policy more complex. The Fed and Treasury have taken steps to limit the fallout of the SVB collapse while leaving room to fight inflation by continuing to raise rates. Interest rate volatility have risen sharply this month as the market price in the uncertainty of Fed policy in the coming months.

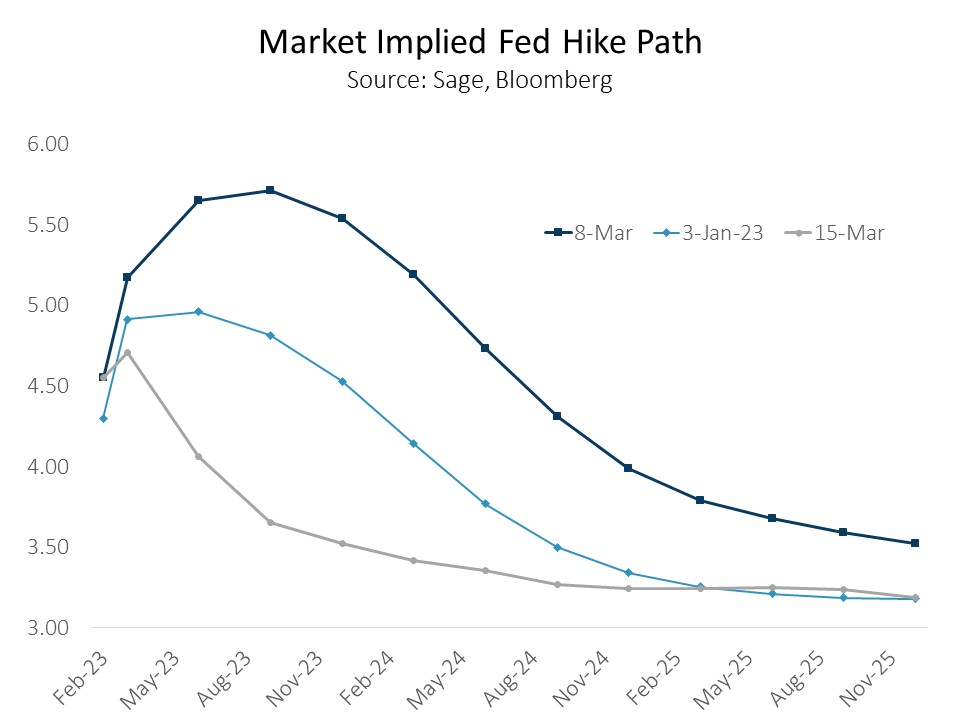

1) Banking Stress Results in Significant Shift in Fed Funds Path. The banking stress in SVB and Credit Suisse have re-priced the expected path of Fed Funds to include rate cuts starting in Q2. Rates have whipsawed this year as the expectation for Fed Funds shot higher in response to strong data, then plummeted in a few trading days due to SVB.

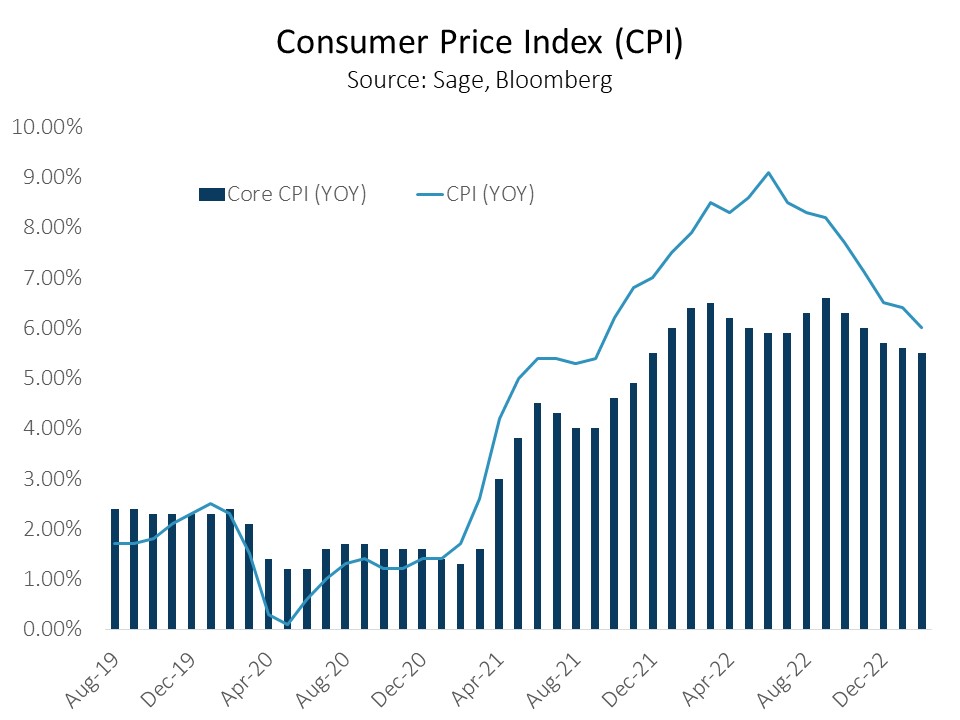

2) Inflation Remains Above Trend. The most recent CPI measure confirms an inflation downtrend, while still being well above the Fed’s target of 2%. Even as energy prices have fallen, inflation remains sticky, particularly in the shelter category.

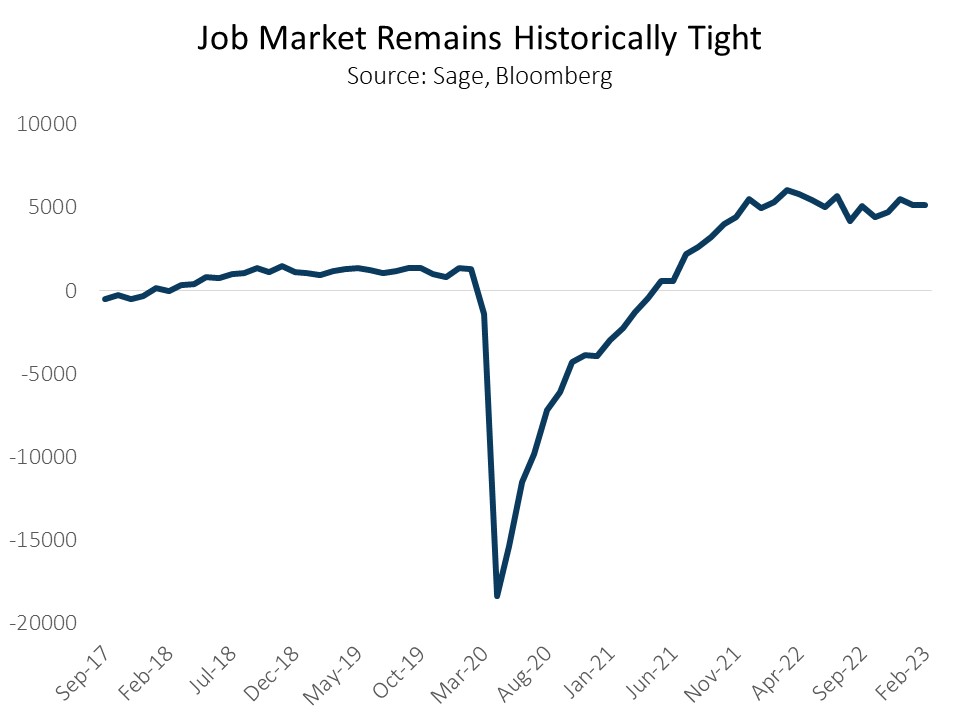

3) Labor Market Still Signaling Full Employment. The US labor market remains secularly tight while wages remain above trend. The Fed will have to weigh labor market tightness and above trend inflation with emerging financial stability concerns as it makes its policy rate decision next week.

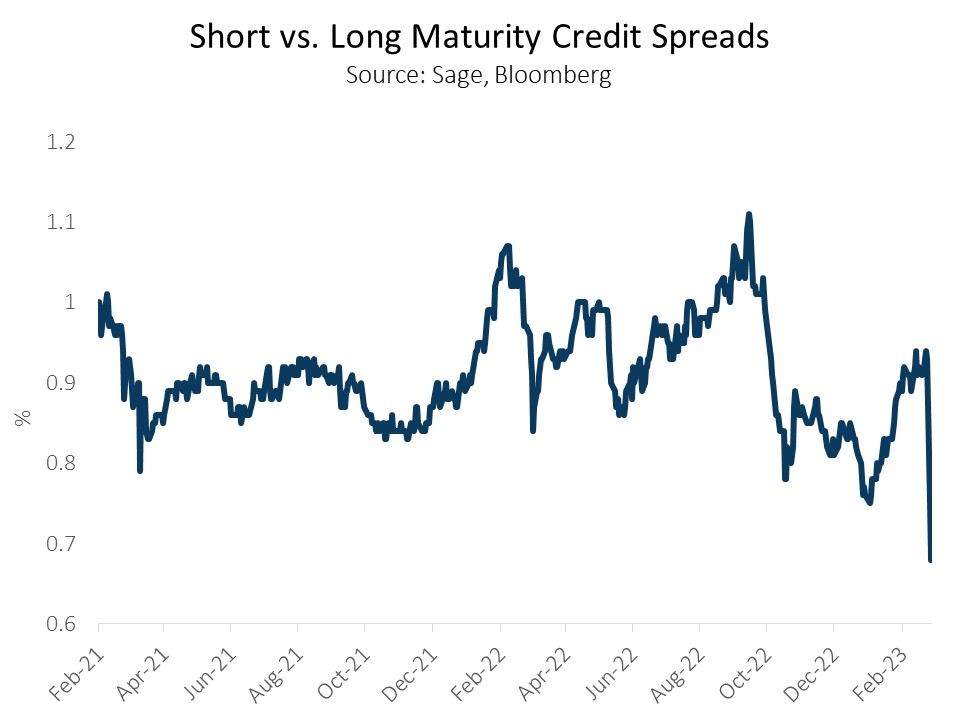

4) Credit Spread Widening, Particularly in Shorter Maturities. Given the stresses in the banking sector, credit spreads have widened. However, they are not signaling a looming credit crisis. The spread curve has flattened with shorter maturity bonds’ spreads widening by more than longer maturities.

5) MBS Could Present Value As Interest Rate Volatility Normalizes. MBS spreads continue to be heavily influenced by interest rate volatility. Spreads tightened significantly from October of 2022 through January of 2023, as volatility came off all time highs. More recently, mortgage spreads have widened as the market’s reassessment of peak rates has pushed volatility higher. While the short-term could be choppy, we believe agency MBS continues to provide significant carry and will benefit from an eventual decline in volatility.

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our web site at www.sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.