Key Points:

- Cumulative Effect: It’s not individual rate cuts, but the total reduction over an easing cycle that significantly impacts the economy. The market is currently pricing in over 2% in short-term rate reductions over the next year.

- Housing Market Resilience: The housing market is expected to remain strong due to consumer financial strength and housing shortages, which may be increased by demographic shifts.

- Corporate Benefits: Lower interest rates help indebted companies increase profits or reduce losses and can stimulate business investment by making borrowing for capital expenditures more affordable.

- Consumer Spending: Reduced borrowing costs may encourage increased consumer spending on major purchases like cars and homes that can potentially boost economic growth.

- Capital Flow Changes: Lower yields on safe investments like T-bills may push investors towards other areas including longer-duration bonds or slightly riskier assets that can affect interest rates and credit spreads.

- Market Implications: While rate cuts can support higher equity valuations, they also signal economic concerns. In fixed income, investors may face a dilemma between locking in current yields and stretching for higher returns.

- Balancing Act: While rate cuts aim to stimulate the economy, they can lead to unintended consequences like asset bubbles and reduced policy effectiveness over time, which highlights the need for balanced economic policy.

In the complex landscape of monetary policy, the U.S. Federal Reserve’s (Fed) decision to cut interest rates reverberates throughout the economy influencing everything from corporate profits to consumer spending. While a single interest rate cut may seem insignificant in isolation, it’s the cumulative effect of multiple cuts over an easing cycle that truly shapes economic outcomes. Its important to explore the multifaceted impact of these rate cuts on the economy, investors, and markets.

The Domino Effect of Rate Cuts

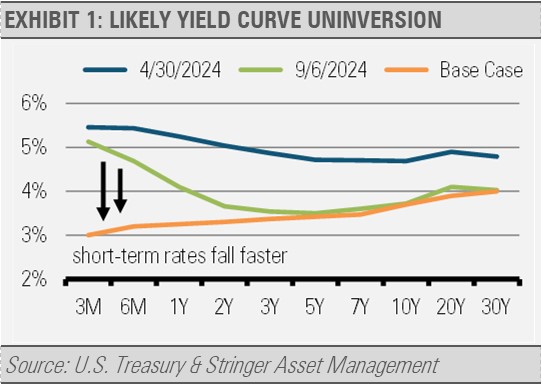

When the Fed initiates an easing cycle, it sets in motion a series of economic dominoes. The market is currently pricing in over 2% in reductions for short-term interest rates over the next year. However, it’s crucial to understand that longer-term interest rates, such as the benchmark 10-year Treasury yield that significantly influences mortgage rates, are set by market forces rather than directly by the Fed. Despite the anticipated rate cuts, we do not expect to see much easing of longer-term rates as they are already below historical averages.

This dynamic creates an interesting scenario for the housing market. With consumer finances generally robust and a persistent shortage of houses, the real estate sector is poised to remain resilient and potentially gain momentum. This could be further fueled by demographic shifts as Baby Boomers sell their properties and more Millennials enter the home-buying market.

Corporate America: A Breath of Fresh Air

For companies carrying debt, interest rate cuts can be a significant boon. Lower interest costs directly impact the bottom line that can allow indebted firms to increase profits or reduce losses. This financial relief may be particularly crucial for companies in capital-intensive industries or those navigating challenging economic conditions.

Moreover, the reduced cost of borrowing can spur business investment. As financing for plant and equipment becomes more affordable, companies may be more inclined to expand operations, upgrade technology, or pursue innovative projects. This increased investment can, in turn, drive economic growth and potentially create new job opportunities.

Consumer Spending and Economic Growth

The ripple effects of rate cuts extend beyond the corporate world to individual consumers. As borrowing costs decrease, consumers may find it more attractive to finance major purchases, such as cars and homes. This potential uptick in consumer spending can provide a significant boost to economic growth as consumer expenditure is a key driver of GDP.

However, it’s important to note that the relationship between interest rates and consumer behavior is not always straightforward. Factors, such as consumer confidence, job security, and overall economic outlook, also play crucial roles in spending decisions.

The Great Migration of Capital

One of the most intriguing aspects of interest rate cuts is how they influence capital flows. As yields on traditionally safe investments like Treasury bills and money market funds decrease, investors may seek higher returns elsewhere. This doesn’t necessarily mean a direct flow into stocks, as many risk-averse investors might prefer to stay within the fixed income universe. The migration of capital into longer-duration bonds or slightly riskier credit instruments can have several effects:

- It can help keep longer-term interest rates down that potentially benefits borrowers across various sectors.

- It can keep credit spreads tight and make it easier for companies to access affordable financing.

- It may indirectly support equity prices by creating a more favorable environment for corporate borrowing and investment.

Market Implications and Investor Considerations

For investors, the implications of rate cuts are multifaceted. While lower rates can support higher equity valuations by making future cash flows more valuable in present terms, they also signal the Fed’s concern about economic conditions. This can create a mixed sentiment in the stock market.

In the fixed income space, investors face a dilemma. The prospect of further rate cuts might encourage some to lock in current yields on longer-term bonds. However, those requiring current income might find themselves stretching for yield, potentially taking on more risk than they initially intended.

The Balancing Act

It’s crucial to remember that while rate cuts are generally implemented to stimulate the economy, they are not without potential downsides. Prolonged periods of low interest rates can lead to asset bubbles, encourage excessive risk-taking, and limit the Fed’s ability to respond to future economic crises.

Furthermore, the effectiveness of rate cuts can diminish over time, especially if rates are already low. This is why many economists and policymakers emphasize the importance of fiscal policy working in tandem with monetary policy to achieve balanced and sustainable economic growth.

Conclusion

The impact of Fed interest rate cuts extends far beyond a simple reduction in borrowing costs. It’s a complex interplay of economic forces that affects corporations, consumers, investors, and markets in a myriad of ways. While rate cuts can provide short-term stimulus and relief, their long-term effects depend on a variety of factors including the overall economic context, global conditions, and the interplay with other policy measures.

As we navigate this period of monetary easing, it’s essential for all economic participants, from individual investors to corporate leaders, to consider both the opportunities and risks presented by this evolving financial landscape. We continue to see an abundance of investment opportunities in high quality equity and fixed income assets that we think can earn an attractive return while helping investors navigate the risks associated with this changing environment.

For more news, information, and strategy, visit the ETF Strategist Channel.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.