1. By pausing rate hikes and slowing quantitative tightening, the Federal Reserve has supported equities and other risk assets; valuations have since moved back to fair territory after the January rally. This chart illustrates how the Fed’s policy reactions have corresponded with the direction of equity markets.

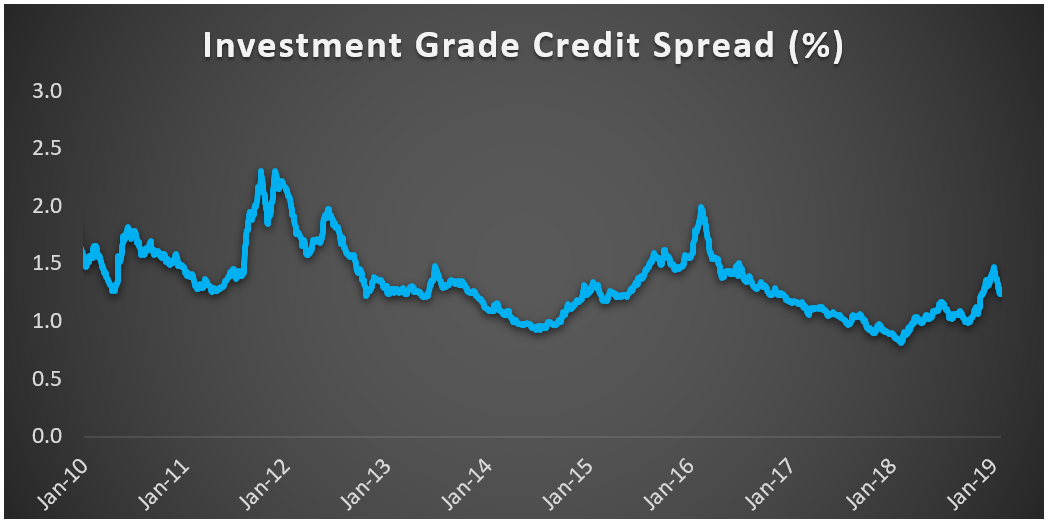

2. The fourth quarter provided an excellent opportunity to add credit exposure as markets became too aggressive in pricing in recession concerns. Supportive technical indicators and higher yields suggest credit has further room to outperform.

2. The fourth quarter provided an excellent opportunity to add credit exposure as markets became too aggressive in pricing in recession concerns. Supportive technical indicators and higher yields suggest credit has further room to outperform.

3. Downward pressure on rates caused by a more dovish Fed and weakening global growth is being offset by continued balance sheet runoff and moderate growth in the U.S. Rates are likely to be rangebound in the near-term.

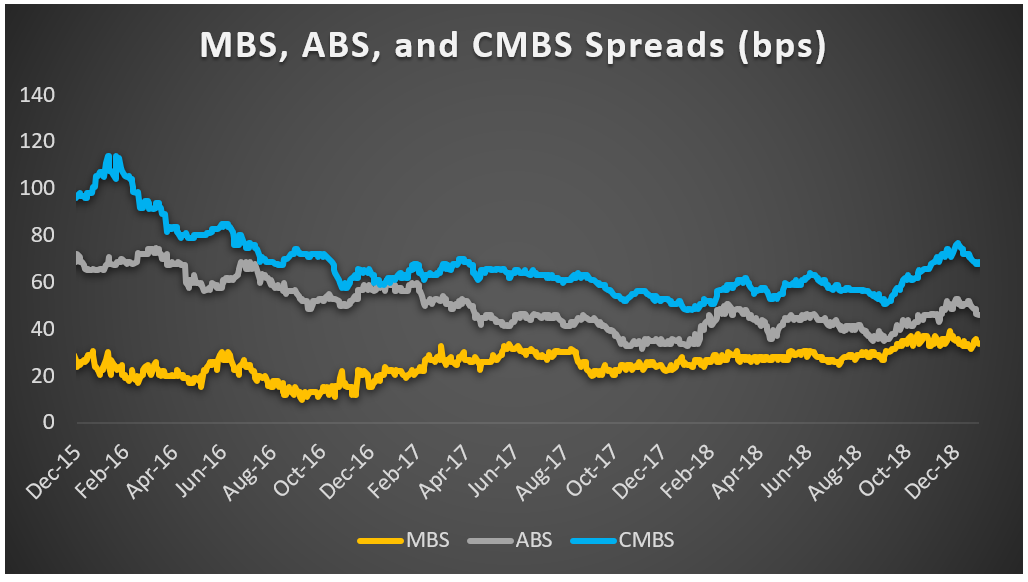

4. A strong housing market coupled with a rangebound outlook for interest rates are supportive of an allocation to mortgage pass-throughs.

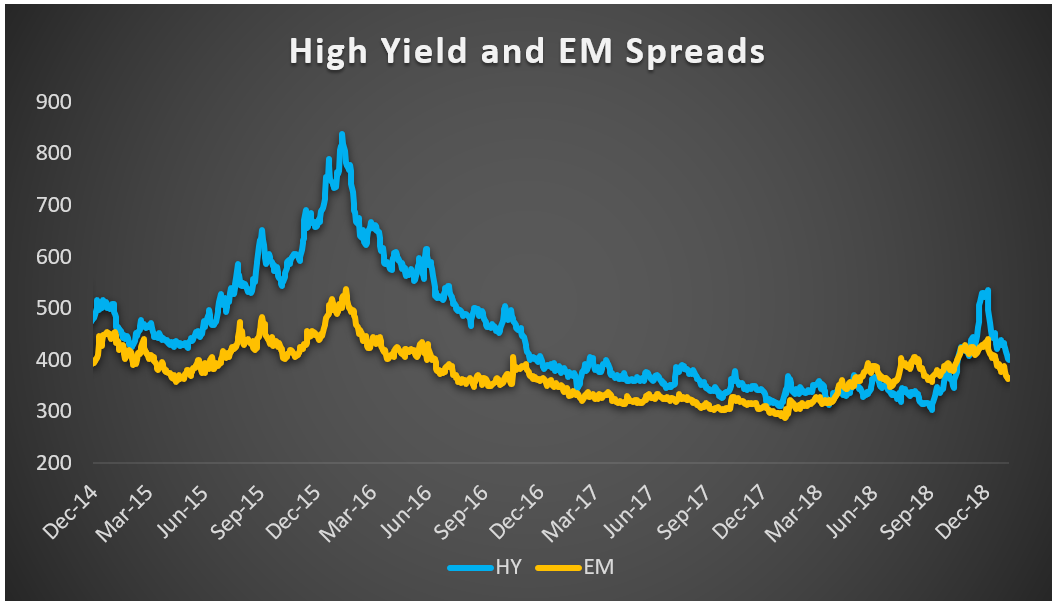

5. Bullish sentiment, yield carry, and valuation data suggest now is the time to hold an allocation to select non-core fixed income sectors, such as emerging markets.

The source for all charts is Bloomberg.

The source for all charts is Bloomberg. To view Sage’s February Equity Outlook, click here.

This article was written by the team at Sage Advisory, a participant in the ETF Strategist Channel.

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our web site at www.sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.