Our Cash Indicator methodology acts as a plan in case of an emergency. This is analogous to the multiple safety systems in a modern automobile, which includes an airbag. Importantly, each of these systems work together to potentially help smooth the ride.

We manage risk tactically over the short-term by investing across a broad array of themes and asset classes including cash. We can either invest opportunistically or defensively depending on the environment.

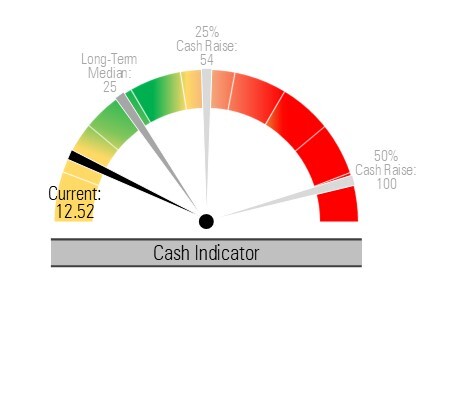

Cash Indicator: Markets are functioning properly, but we expect continued volatility.

Our proprietary Cash Indicator (CI) provides insight into the health of the market by monitoring the level of fear using equity and fixed income indicators. This warning system is designed to signal us to either a 25% or 50% cash position to potentially protect principle and provide liquidity to reinvest at lower and more attractive valuations.

The CI has dipped back to extremely low levels suggesting a high degree of complacency in the financial markets. We expect financial market volatility to increase in the coming months as markets eventually normalize.

Strategic View: Fixed income valuations remain attractive, as do equities except the few that have rallied recently.

Equity Valuations: The recent market rally has pushed valuations broadly higher and extremely high for the narrow group of equities that led last year’s rally. On a risk-reward basis, other areas of the global equity market look quite attractive with the exception of Europe and especially China.

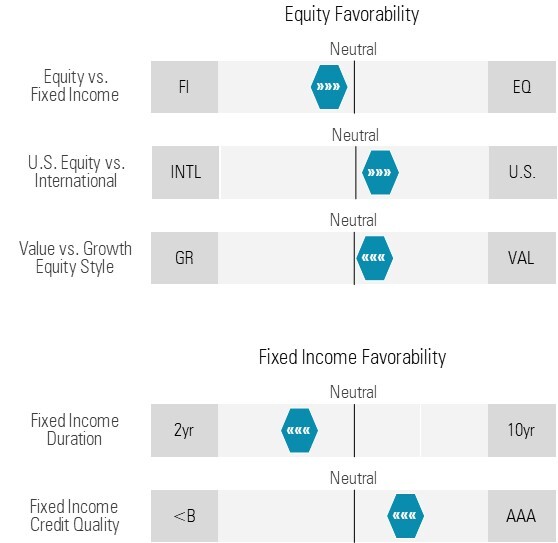

Equity Favorability: While still favoring the U.S., we have reduced our overweight to domestic equities due to the extreme valuation gap between the capitalization-weighted U.S. equity market and defensive U.S. equities along with dividend payers and high quality foreign equities.

Fixed Income Valuations: At current interest rates, high quality fixed income looks very attractive, while high yield is less attractive on a risk-reward basis.

Fixed Income Favorability: We have combined intermediate-term with short-term holdings to lock in higher interest rates. If short-term interest rates fall in the coming months as we expect, the income generated by intermediate holdings will remain stable even as these bond prices appreciate. In addition, the commercial mortgage back space offers compelling yields outside of office space and retail.

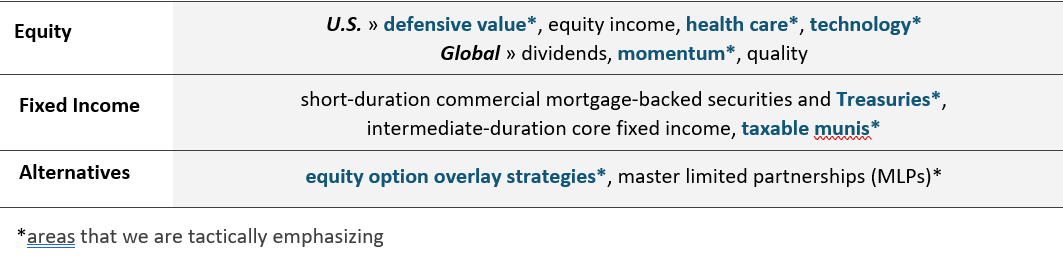

Tactical View: We favor defensive equity, dividend payers, fixed income, and alternative investments.

We expect the Federal Reserve (Fed) to begin cutting short-term interest rates this year. Slowing economic growth, falling inflation, and Fed rate cuts should combine to cause interest rates to fall. Investors can prepare for falling interest rates by locking in current income for longer utilizing high quality intermediate-term fixed income investments. As interest rates eventually decline, these holdings should benefit from both consistent income as well as price appreciation. In addition, the valuation gap between U.S. and international equities has reached extreme levels, which makes foreign equities in stable economies a relative bargain. We think that investors can take advantage of this opportunity by investing in high quality foreign companies and markets that exhibit positive momentum.

Global Broad Outlook: We remain cautious about the European market, but cautiously optimistic about most others.

For more news, information, and analysis, visit the ETF Strategist Channel.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not be taken as an advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.