By Nick Porter, Astor Investment Management

Factors have entered the mainstream of investing. Factor investing was once limited to academic finance and institutional investors, but strong returns have driven a proliferation of factor (also known as smart beta) products (1025 ETFs with over $823 Bn AUM), allowing individual investors to access factor investing as never before. Of late, however, factor performance has been uneven, leading some to postulate that factors are played out. We briefly review the rationale behind factor investing and recent performance in this post.

Risk Premium or Inefficient Markets?

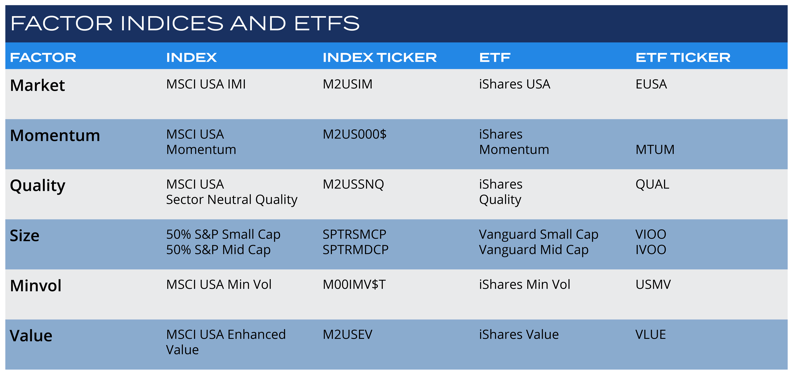

Put simply, fundamental factors seek to achieve above-market returns by exposure to a group of securities with similar characteristics. For example, the value factor looks for companies that are cheap relative to earnings. Factors are appealing because they have been largely validated by academic finance, have sound economic rationale and are easy to invest into via rules-based indexing.

Source: Astor

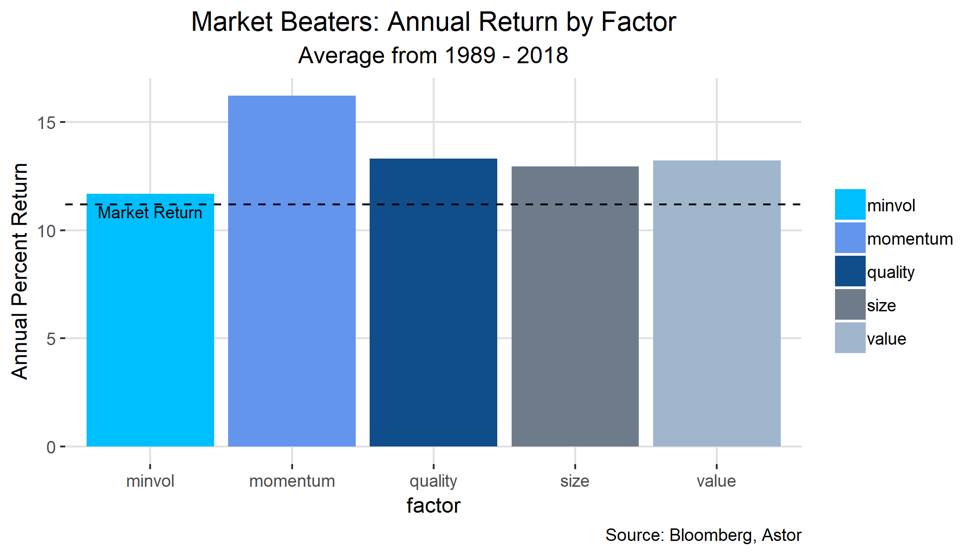

Of course, strong historical returns have helped as well. There is a wide disparity of definitions of factors and their constituents, but viewed broadly, factors have routinely outperformed the market since 1989, as a substantial body of academic research indicates.

This relationship has held up admirably throughout the economic cycle and broadly in line with what you would expect for each factor’s composition – for example, momentum’s outperformance in expansions and underperformance in recessions. The cyclical nature of factors leads many investors to seek diversification with exposure to many sources of risk premia.