From a purely economic perspective, this election is likely to have little broad economic impact for a number of reasons. First, neither party is likely to have a significant edge in congress. For example, the Republicans have a majority in the Senate, but not enough seats to overcome a filibuster from the Democrats. Therefore, no significant legislative change is likely beyond the extension of the 2017 tax cuts.

While there is a lot of talk on tariffs, the details matter as the other side gets to have a say in any trade war. So, any tariff the U.S. implements is likely to see a retaliatory response from the other side. Also, while tariffs can increase import prices, a strengthening U.S. dollar can offset some of these impacts. And most importantly, while the U.S. trade with other countries is a large nominal dollar amount, it is small relative to the size of the economy.

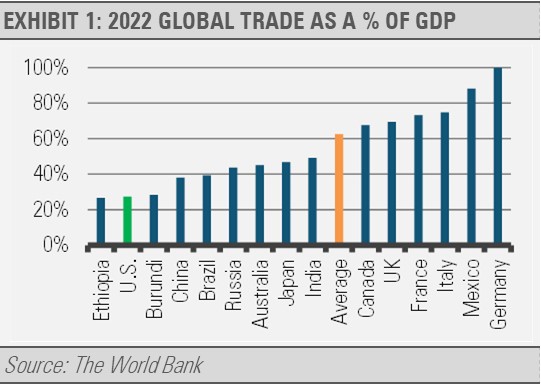

In fact, when ranking countries by global trade as a percentage of economic activity (gross domestic product or GDP), the U.S. ranks near the bottom of the list. As the graph below illustrates, in 2022, the U.S. ranked between Ethiopia and Burundi with less than half the rate of trade per unit of GDP as the world average, 27% vs. 63%.

While the overall impact of tariffs on the domestic economy would likely be limited, lower income households as well as some individual industries and companies could see significant negative impacts. The lack of an administration’s ability to significantly impact the economy and the markets is nothing new. History shows that there is little relationship between which political party holds the White House and either economic growth or stock market performance. This is because the U.S. economy is so vast and primarily driven by the private sector, including households and businesses, that government policy plays a relatively small role in determining economic and financial market outcomes.

The private sector makes up roughly 83% of U.S. economic activity. Over time, the largest drivers of inflation adjusted GDP growth are the growth rate of the labor force and productivity growth. Labor force growth is driven by how many children we have who will eventually enter the workforce as well as immigration. Productivity growth, such as we saw resulting from the information revolution, is driven by private sector innovation. The downward trend we have seen in the rate of GDP growth over the decades has more to do with the slowing of the labor force growth rate as families have fewer children than they did generations ago. This is a global phenomenon we can see across various countries as they move up the development ladder and become more urbanized and less agrarian.

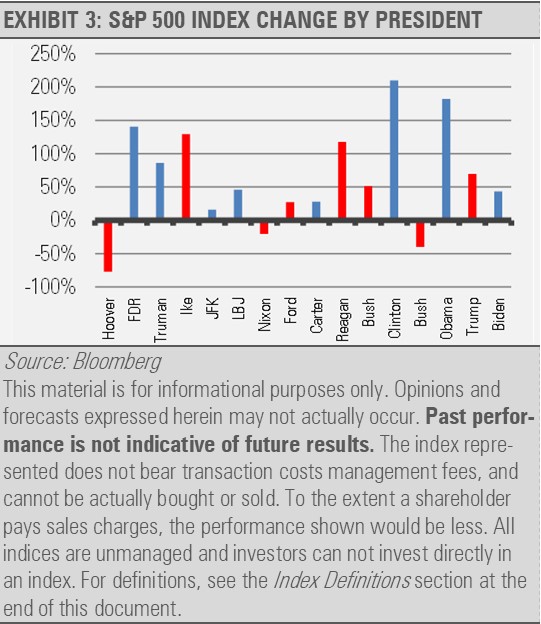

Considering stock market behavior by each administration since Hoover, Democrats seem to have had better stock market performance on average. Two Republican Presidents, Hoover and W. Bush, had the bad luck of beginning their terms after the stock market had huge runs in the1920s and the 1990s, just before the Great Depression and the Lost Decade of the 2000s. Neither of these situations was the Presidents’ fault and, as normal, equity market declines were followed by large equity market rebounds.

With pandemic-era fiscal and monetary stimulus fading, we are largely back to where we started with the “Great Normalization.” A big part of our Normalization theme has to do with the government becoming less involved in economic activity after the stimulus packages and U.S. Federal Reserve policies subside and normalize.

Limiting the federal government interventions into the economy can slow the growth of government spending and allow the country to move to a more stable fiscal path over the years ahead. Fiscal policy will be the greatest challenge for the next administration and several administrations beyond, in our opinion. Politics aside, the federal government will need to embrace a realistic accounting of the situation, and the numbers do not lie. Good financial decisions will have to be made across party lines to get the debt and deficit back in line and heading in the right direction. This is not as impossible as the current political and economic climates may suggest. We have seen it work as political rhetoric has, at least in the recent past, given way to bipartisanship and fiscal responsibility.

One of the best examples of getting the U.S. on firmer footing was President Bush 41 when he went back on his “read my lips” campaign promise and compromised with Democrats to do what was fiscally necessary and raised taxes. President Clinton inherited a healthier tax base as well as the Peace Dividend resulting from the end of the Cold War, and then benefited from increased tax revenue driven by a booming economy that eventually created a surplus and allowed for a cut to the capital gains tax rate. The U.S. federal budget and the deficits will not be resolved in a day and most likely not in the next four years.

Given that the long-term nominal growth rate of the economy is driven primarily by the growth rate of the labor force, the productivity growth of the labor force, and an inflation factor, much of the next decade of growth is already set. Though there will be variability, we think the next decade of growth will be more like the 1990s than the previous business cycle of the 2010s as we believe our economy is set to embark on a new golden age of growth.

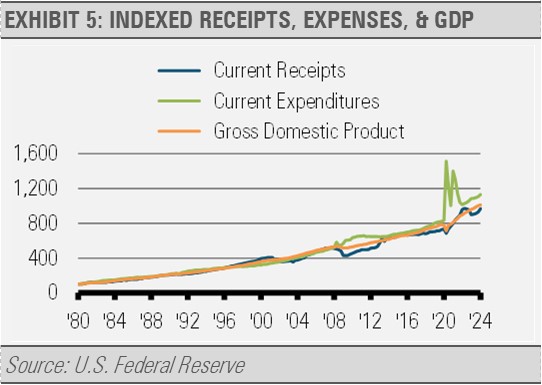

With the private sector driving economic growth and revenue, the government will need to be more disciplined in its expenses so that the growth rate of spending falls below that of revenue. Getting back to sustainability does not require spending to fall, only that the growth rate of spending declines to below the revenue growth rate. This is what we saw during most periods of peacetime economic expansion, especially in the 1990s.

Fiscal discipline is key, and we have seen the government be more fiscally disciplined before. In addition to greater fiscal discipline, innovation can accelerate economic growth just as we saw in the late 1990s with the information technology related boom. Perhaps today’s focus on AI-led innovation can lead to a similar result in the years to come.

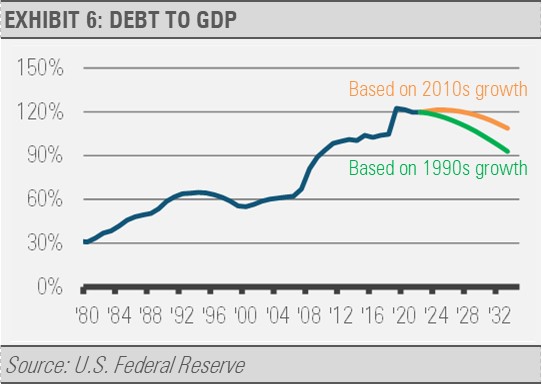

Looking ahead, we can see a path to more sustainable debt levels. For example, the following graph shows the current debt-to-GDP ratio and what two different forward-looking scenarios may look like.

In one scenario, we assume GDP growth will be similar to what occurred during the 1990s, which is our base-case, as well as a scenario where GDP growth is similar to the 2010s. Assuming GDP growth close to the 2010s business cycle average of 4% per year, with government receipts growing at the same rate and spending growth slowing to 2% per year as a result of more fiscal discipline, we forecast that debt to GDP can get back to the pre-COVID levels over the next decade. However, if economic growth is similar to the 1990s as we expect, reigning in spending growth to 2% per year would see a debt-to-GDP level similar to the pre-COVID environment in approximately five-to-seven years.

Meanwhile, the economy has enough economic momentum to carry forward even as the federal government pairs back its support. The roughly 83% of the economy that is not the government and is driven by households and businesses is in great shape overall. For example, household debt service to income levels have plateaued at rates below the long-term average. These healthy debt-to-income levels are supported by increasing household incomes while the average interest rate on an outstanding 30-year fixed rate mortgage is less than 4% and well below rates seen over recent decades. Households will enjoy the benefits of these low interest mortgages for decades to come. The private sector has plenty of capacity to keep the economic engine running while the federal government recalibrates its finances.

INVESTMENT IMPLICATIONS

We continue to favor sectors and industries that have demonstrated consistent earnings growth over time. These investments offer both the potential for downside protection as well as gains due to their more durable business models. On the fixed income side, we are focused on capturing attractive yields with high quality core fixed income. The recent price decline in intermediate-duration fixed income only serves to increase our total return expectation going forward.

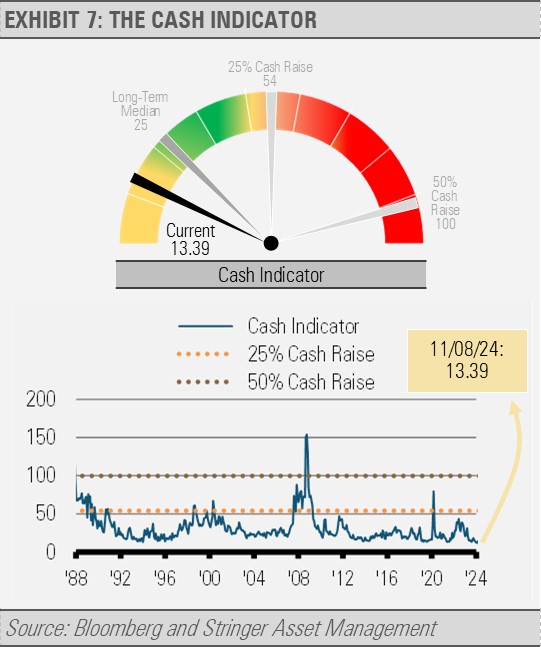

THE CASH INDICATOR

The Cash Indicator has slipped back down as the equity market has rallied. Equity market volatility declined while fixed income credit spreads remain tight. We expect increased volatility in the weeks and months ahead. With the backdrop of continued economic growth, we view equity market drawdowns as opportunities to increase investments in high quality businesses.

For more news, information, and strategy, visit the ETF Strategist Channel.

DISCLOSURES

Any forecasts, figures, opinions or investment techniques and strategies explained are Stringer Asset Management, LLC’s as of the date of publication. They are considered to be accurate at the time of writing, but no warranty of accuracy is given and no liability in respect to error or omission is accepted. They are subject to change without reference or notification. The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment and the material should not be relied upon as containing sufficient information to support an investment decision. It should be noted that the value of investments and the income from them may fluctuate in accordance with market conditions and taxation agreements and investors may not get back the full amount invested.

Past performance and yield may not be a reliable guide to future performance. Current performance may be higher or lower than the performance quoted.

The securities identified and described may not represent all of the securities purchased, sold or recommended for client accounts. The reader should not assume that an investment in the securities identified was or will be profitable.

Data is provided by various sources and prepared by Stringer Asset Management, LLC and has not been verified or audited by an independent accountant.

Index Definitions:

S&P 500 Index – This Index is a capitalization-weighted index of 500 stocks. The Index is designed to measure performance of a broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.