By Doug Sandler, CFA

Summary

- We believe economic data clearly show that 2021 is going to be a banner year for the US economy.

- This will likely lead to greater optimism among consumers who now have the highest saving rate in more than 45 years, in our view.

- Be aware that the strong returns over the last 12-months mean that investors have likely anticipated much of this good news.

If you travelled on Spring Break you probably felt it…That feeling that economic activity seems ready to burst, like the release of water from a hose after a kink has been removed. This pent-up pressure is a result of an economic trifecta, which we define as three strong tailwinds triangulating on the US economy at roughly the same time.

-

- The re-opening of the economy: Vaccine distribution in the US has quickly climbed the learning curve and according to the CDC, we are now vaccinating more than 3 million Americans every day. According to Youyang Gu, who uses machine-based learning for making COVID-19 related projections, the US should return to normal (removal of all COVID-19 related restrictions for the majority of US states) by Summer 2021.

- High savings rates: Savings rates are exceptionally high hovering near 15%, the highest level in over 45 years. We believe that this is due to the tremendous economic uncertainty created by COVID-19. It is our view that as the uncertainty recedes high savings rates create the wherewithal for future discretionary spending.

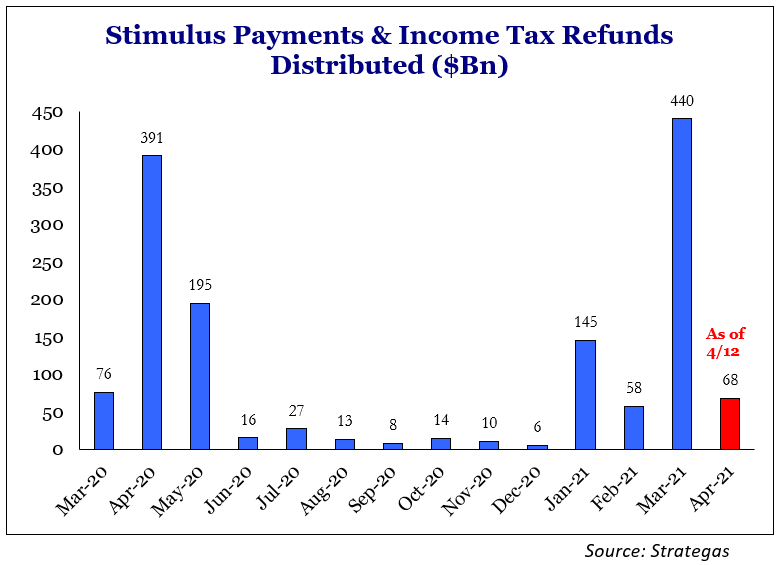

- Influx of government payments: The third tailwind in the trifecta is the fact that a large chunk of the population just received or are about to receive one or more meaningful distributions from the federal government in the form of a stimulus check and/or an income tax refund (Chart 1).

Chart 1: Federal Distributions Likely to Further ‘Prime the Pump’ of Spending.

Disclosures: Past performance is no guarantee of future results. Shown for illustrative purposes.

This economic surge should be good for everyone, but it may be more impactful to the average American (‘Main Street’) than the average investor (‘Wall Street’). We see three main differences between Main Street and Wall Street. Over the last 12-months these differences most benefitted Wall Street, over the next 12-months these same differences may work more in Main Street’s favor.

Street. Over the last 12-months these differences most benefitted Wall Street, over the next 12-months these same differences may work more in Main Street’s favor.

1. Wall Street reflects the future, Main Street reflects the present:

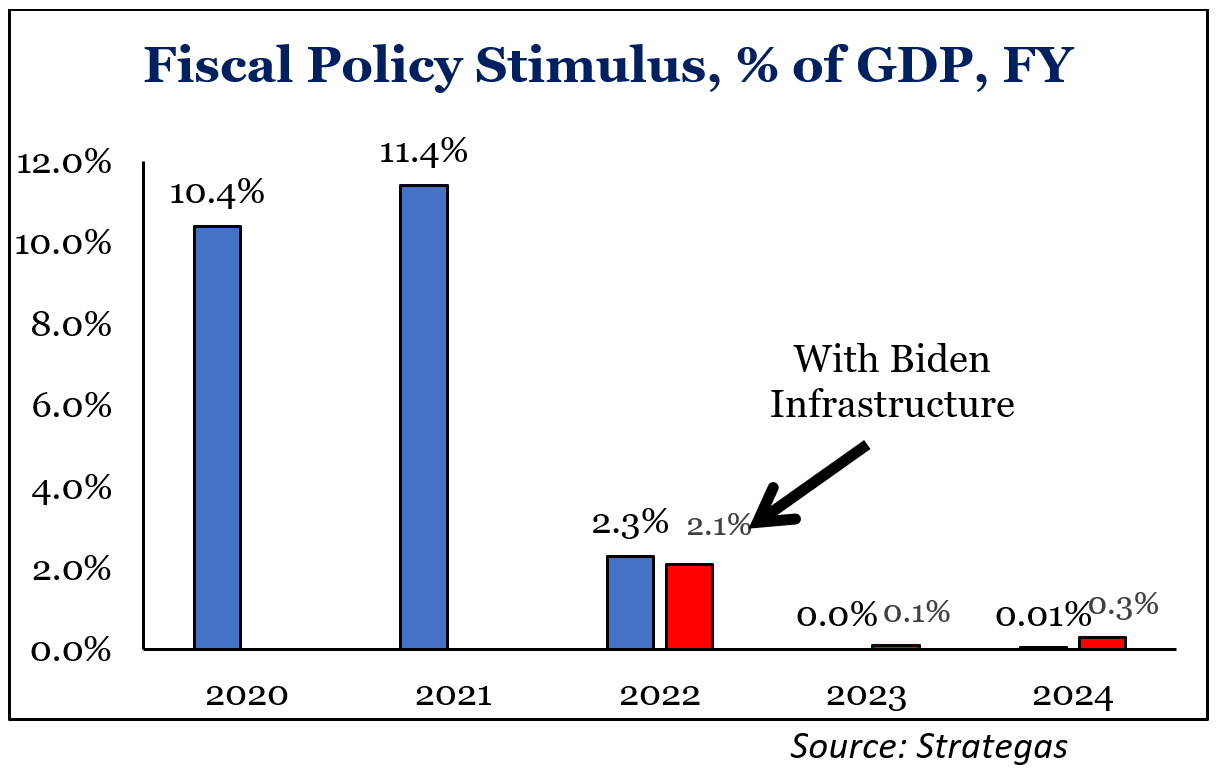

Stock market investors typically looks 6 to 12 months into the future. Therefore, we believe that a significant proportion of the stock market’s strength over the past 12 months can be accredited to it foreseeing the strong economic period we are about to enter. Extraordinary growth, falling unemployment, and rising wages have been anticipated by Wall Street and thus may already be reflected in stock prices to some degree. The market is beginning to look beyond 2021 and will start reflecting what it sees in 2022. Unfortunately, 2022 is unlikely to be as universally positive as 2021. In fact, 2022 is already harboring its share of bogeymen. Higher taxes, fading stimulus (Chart 2), fears of inflation, shifting Fed policy, and mid-term elections are just a few of those concerns on the horizon we are identifying.

Chart 2: Fiscal Stimulus Fades in 2022

Disclosures: Past performance is no guarantee of future results. Shown for illustrative purposes.

2. Wall Street represents a minority of US companies, Main Street represents the majority:

The prospects for large and small companies can differ significantly, especially during difficult times. Since COVID-19 first impacted the economy over a year ago, the business climate has been far more favorable to companies listed on Wall Street. Wall Street is comprised of large public companies, who have stronger technological platforms and better access to capital. These large companies were also more likely to employ the ‘experts’ necessary to take advantage of complex government aid programs. Not surprisingly, the average valuation of public companies has risen significantly as investors recognized these advantages.

According to data from the US Census Bureau and Wilshire Associates, public companies represent less than 1% of all US companies. The National Bureau for Economic Research also notes that publicly traded companies account for roughly one-third of US non-farm employment. Therefore, the other 99%+ of US companies and two-thirds of employment come Main Street. Main Street companies are often smaller (many may be sole proprietors), more poorly capitalized, and less technologically advanced. Thus, Main Street companies have disproportionately been impacted by state-mandated shutdowns and less able to shift to ‘work from home’. However, as the economy begins to surge from pent-up demand, we believe that the competitive advantages of Wall Street companies will become less compelling, particularly in light of their higher stock prices.

3. Wall Street focuses on earnings and stock prices, Main Street focuses on wages and home prices:

Main Street will appreciate tightening labor markets since they contribute to rising wages. Main Street should also love the fact that the housing market is extremely strong, benefitting from a rise in home ownership and ultra-low interest rates. Wall Street, on the other hand, does not necessarily like rising wages since they negatively impact profit margins and earnings. The potential for higher corporate taxes and a stricter regulatory environment also threatens to pressure earnings in the future. We believe these pressures may be strong enough to offset some of the benefits of a strengthening economy.

Conclusion:

Our view is that both Wall Street and Main Street will be smiling throughout 2021. For this reason, we are modestly overweight stocks in our balanced Advantage portfolios. However, over the next 12-months, Main Street’s smile may be slightly wider than Wall Street’s, which we think will be a good thing for America.

Going forward, we think investors may want to prepare for lower returns over the next 5-7 years and potentially higher volatility as the stock market may at some point start to look beyond the strong economic period we are entering.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

In a rising interest rate environment, the value of fixed-income securities generally declines.

When referring to being “overweight” or “underweight” relative to a market or asset class, RiverFront is referring to our current portfolios’ weightings compared to the composite benchmarks for each portfolio. Asset class weighting discussion refers to our Advantage portfolios. For more information on our other portfolios, please visit www.riverfrontig.com or contact your Financial Advisor.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2021 RiverFront Investment Group. All Rights Reserved. ID 1610891