By DeFred Folts III, Managing Partner, Chief Investment Strategist, and Eric Biegeleisen, CFA, Managing Director, Research Portfolio Manager

Equities:

▶ U.S. Equities: The U.S. equity market outlook is a bit more neutral currently given the tug of war between the positive impact of the global economic rebound and concerns about whether robust economic growth will prove to be inflationary, thereby prompting the Federal Reserve to withdraw its extraordinary monetary policy support sooner than anticipated. At the same time, equity markets in general, including the U.S., are continuing to benefit from accommodative central bank policies, narrowing credit spreads, and steepening yield curves.

▶ India Equities: Our model research currently finds the India equity market to be attractive. Current struggles with the pandemic and the upcoming elections should encourage highly accommodative monetary and fiscal policies for an extended period and leave room for economic improvement once vaccinations ramp up. Additional factors that enhance the prospects for the Indian equity market include the potential for future economic growth as indicated by a steepening yield curve measure, a benign interest rate environment, and favorable long-term

demographic trends.

▶ Japanese equities remain attractive and should continue to benefit from narrowing high yield spreads, steepening yield curve measures, and positive investor psychology. In addition, the global economic recovery from the coronavirus pandemic should benefit many of Japan’s largest corporations since they tend to export their products all over the world, including into the U.S.

▶ European Equities: European companies should also continue to benefit from the sustained and extraordinary monetary and fiscal stimulus required to support the region because of a slower recovery from the coronavirus pandemic and inconsistent progress on vaccinations. In addition, a continued rotation from growth equities to the stocks of more cyclical companies that benefit more from the ongoing global economic recovery should continue to be positive for Europe. Early signs of increasing inflation in the Eurozone will need to be monitored.

▶ China Equities: The model outlook for Chinese equities is currently neutral. While Chinese companies benefit from accommodative monetary policies as reflected in the favorable price momentum we’ve witnessed recently, the recent uptick in U.S. inflation, elevated U.S. Treasury yields, and strengthening of the Chinese Yuan neutralizes the overall outlook in the short-term.

Fixed Income:

▶ The bond market has been relatively stable recently, even in the face of economic data indicating signs of inflationary pressures throughout the economy as the U.S. emerges from the pandemic. U.S. Treasuries represent an unattractive risk-return trade-off at current yields as they continue to yield less than the market’s expected inflation rate across nearly all maturities.

▶ Caused in part by investors searching for yield, expectations for economic recovery, and the Fed’s continued tacit support of the credit markets (corporate bonds), credit spreads – the difference between high-yield and investment-grade bond yields – have continued to narrow and junk bond issuance remains strong. However, with record amounts of corporate debt outstanding and with historically low yields for high-yield bonds, there is a heightened risk that any accident in the financial markets could cause credit spreads to widen abruptly.

Real Assets:

▶ Gold has now recovered most of the declines that it suffered earlier in 2021 and continues to be supported by negative real interest rates (nominal rates minus inflation expectations). Gold could also benefit from future inflation prospects, particularly if the Fed maintains its stance on inflation being transient and sticking to its stated timeline on interest rate policy and bond-buying programs.

▶ Commodities remain attractive due to the longstanding relative undervaluation of real assets and the prospect of a robust global economic recovery in the second half of 2021, as well as the prospects for a weaker U.S. dollar. Other factors positively impacting real assets include; appreciation of the Chinese Yuan, narrowing credit spreads, steepening global yield curves, and positive investor psychology.

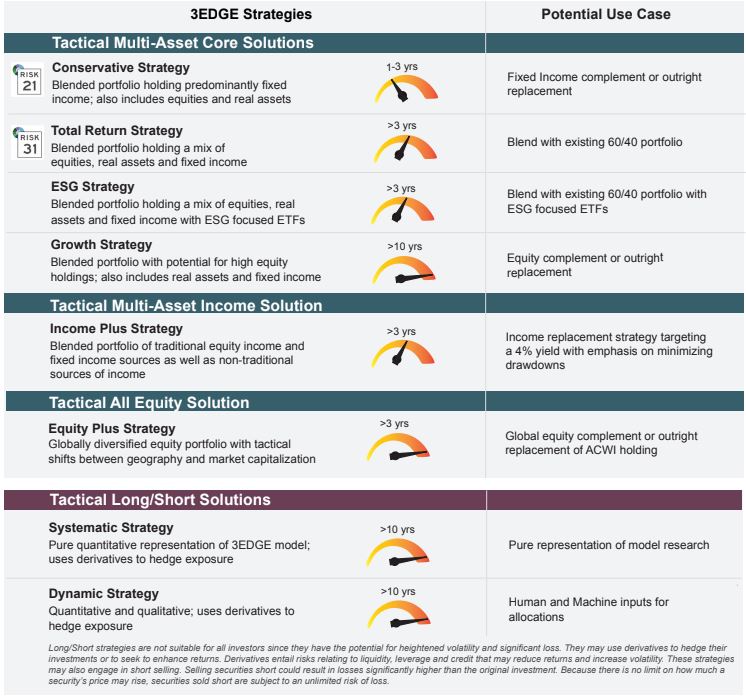

3EDGE Solutions Designed to Smooth the Ride

Seeking to manage volatility and downside risk while providing the potential to be additive to investment returns

About 3EDGE

3EDGE Asset Management, LP, is a global, multi-asset investment management firm serving institutional investors and private clients. 3EDGE strategies act as tactical diversifiers, seeking to generate consistent, long-term investment returns, regardless of market conditions, while managing downside risks.

The primary investment vehicles utilized in portfolio construction are index Exchange Traded Funds (ETFs). The investment research process is driven by the firm’s proprietary global capital markets model. The model is stress-tested over 150 years of market history and translates decades of research and investment experience into a system of causal rules and algorithms to describe global capital market behavior. 3EDGE offers a full suite of solutions, each with a target rate of return and risk parameters, to meet investors’ different objectives.

DISCLOSURES: This commentary and analysis is intended for information purposes only and is as of April 2, 2021. This commentary does not constitute an offer to sell or solicitation of an offer to buy any securities. The opinions expressed in View From the EDGE® are those of Mr. Folts and Mr. Biegeleisen and are subject to change without notice in reaction to shifting market conditions. This commentary is not intended to provide personal investment advice and does not take into account the unique investment objectives and financial situation of the reader. Investors should only seek investment advice from their individual financial adviser. These observations include information from sources 3EDGE believes to be reliable, but the accuracy of such information cannot be guaranteed. Investments including common stocks, fixed income, commodities, ETNs and ETFs involve the risk of loss that investors should be prepared to bear. Investment in the 3EDGE investment strategies entails substantial risks and there can be no assurance that the strategies’ investment objectives will be achieved. Real Assets (Gold & Commodities) includes precious metals such as gold as well as investments that operate and derive much of their revenue in real assets, e.g., MLPs, metals and mining corporations, etc. Intermediate-Term Fixed Income includes fixed income funds with an average duration of greater than 2 years and less than 10 years. Short-Term Fixed Income and Cash includes cash, cash equivalents, money market funds, and fixed income funds with an average duration of 2 years or less. Past performance may not be indicative of future results.

The Risk Number®, a proprietary scaled index developed by Riskalyze to quantify the risk of a portfolio, is calculated based on downside risk on a scale from 1- 99. The greater the potential loss, the greater the number. The Risk Number® includes analysis and proprietary information of Riskalyze. As of 3/31/21. Further information available at Riskalyze.com.

View from the EDGE is a registered trademark of 3EDGE Asset Management, LP