From tweets to trade wars to impeachment inquiries, 2019 has been anything but steady. The one thing that has weathered the storm? The U.S. equity market, which is up almost 25% YTD. Despite this strong performance, there is an increasing concern among investors that equity prices may be out of line with corporate fundamentals.

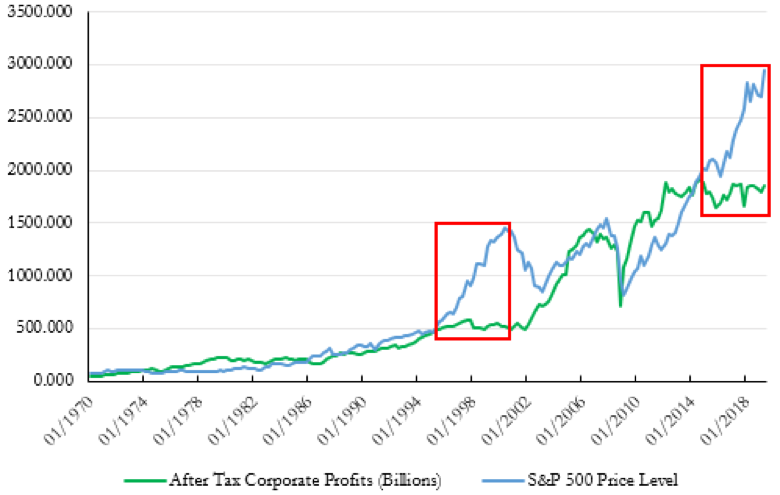

Although the stock market continues reaching record highs, companies are making less than they did five years ago, so this performance is largely driven by P/E expansion (see Figure 1 below). This could be reminiscent of the Tech Bubble, when prices also saw strong acceleration despite stagnant earnings. Before the bubble burst, there were also large divergences between earnings and prices, however a sudden reversal brought equities back down to reality, and earnings soon caught up. A similar scenario is not out of the question today, considering the Shiller P/E, which stood at over 30 in November, is approaching its highest level since March 2000.

Figure 1: S&P 500 Price Level vs. After Tax Corporate Profits (1970- Present)

Source: St. Louis Fed, Yahoo Finance

Running a simple linear model, we see a tight fit between corporate profits and equity prices (see Figure 2 below). There is over 92% correlation between the variables since 1950, with essentially zero probability (P<.0001) that earnings are extraneous to the price of equities. Since every major residual in the model prior to 2015 stems from either the Tech Bubble or the recovery from the Great Recession, there is good reason to believe that the current environment represents a fundamental mispricing in the stock market. For instance, applying the model to the most recently available earnings data would yield a predicted S&P 500 price level of below 2566 with 97.5% probability, quite the far cry from the current levels of over 3100.

Figure 2: Simple Linear Model

Source: St. Louis Fed, Yahoo Finance

A large part of this P/E expansion can be attributed to aggressive corporate buybacks. According to Goldman Sachs’ Research Team, only corporations and households have been net buyers of equities since 2015, with buybacks accounting for a large majority of the demand (see Figure 3 below). If the market loses this key piece of support going forward, either through regulation or from natural causes (e.g. higher prices will require a greater investment from an already flat earnings pool), then one would expect equities to come back down to more reasonable valuations.

Figure 3: Net Equity Demand by Category (Billions)

Going forward, the market’s reliance on buybacks without earnings growth may become less sustainable since the impact of the tax cuts has run its course and the global economy may headed towards further slowdown. Investors are faced with a difficult choice. If they stay fully invested, then they leave themselves open to large losses. On the other hand, if they take defensive positions, they stand to leave substantial money on the table. Tactical strategies, which aim to participate in market expansions and limit losses during prolonged market downturns, may be a worthwhile consideration to solve this dilemma.

Disclosure

Julex Capital Management is an SEC-registered quantitative investment management firm specializing in tactical asset allocation strategies. The firm offers a variety of tactical unconstrained investment solutions aiming to provide downside risk management while maximizing the upside potentials using its unique Adaptive Investment Approach.

The information in this presentation is for the purpose of information exchange. This is not a solicitation or offer to buy or sell any security. You must do your own due diligence and consult a professional investment advisor before making any investment decisions. The risk of loss in investments can be substantial. You should therefore carefully consider whether such trading is suitable for you in light of your financial condition.

The use of a proprietary technique, model or algorithm does not guarantee any specific or profitable results. Past performance is not indicative of future returns. The performance data presented are gross returns, unless otherwise noted.

All information posted is believed to come from reliable sources. We do not warrant the accuracy or completeness of information made available and therefore will not be liable for any losses incurred. No representation or warranty is made to the reasonableness of the assumptions made or that all assumptions used to construct the performance provided have been stated or fully considered.