Click here to download the PDF

Equities:

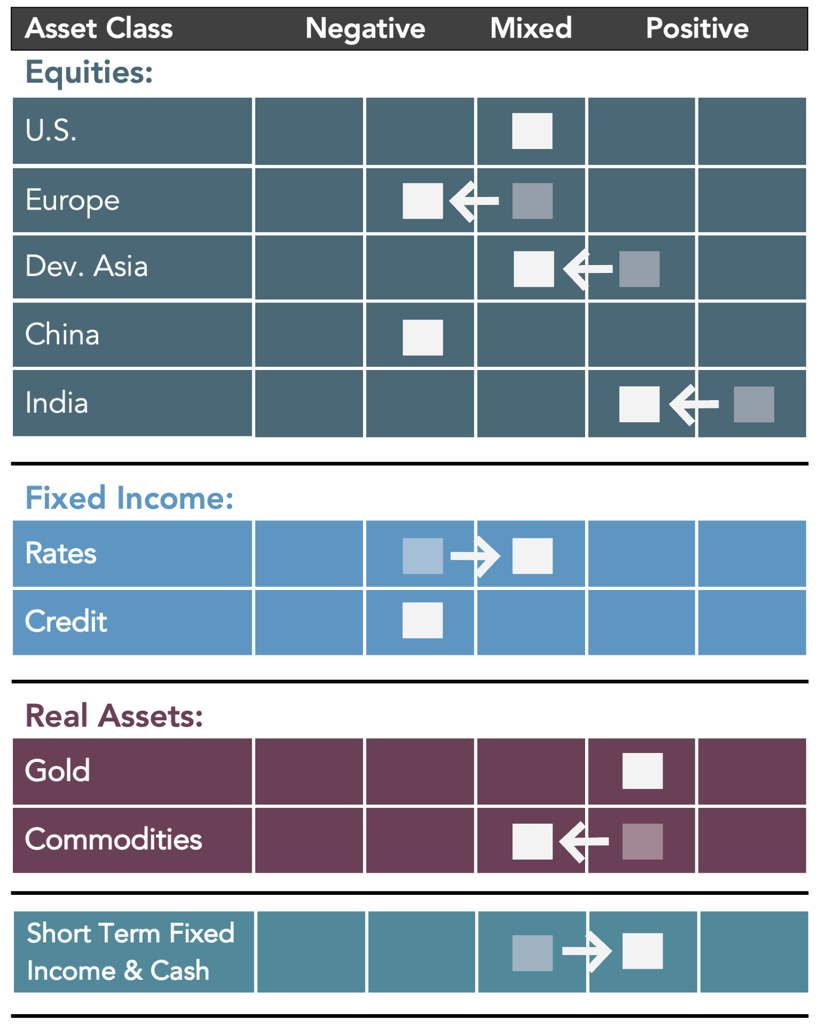

Equities:

▶ U.S. equities continue to hover around their November highs and remain significantly overvalued. A recent widening in high yield credit spreads in the U.S. has somewhat negatively impacted the attractiveness of the U.S. equity market. Beyond retiring the word ‘transitory’ in describing the inflationary pressures in the U.S., Fed Chair Powell also expressed support for a quicker taper of the Fed’s monthly bond purchases than was laid out in November. Correspondingly, market-based measures indicate a higher probability for rate increases as soon as May 2022 as the Fed attempts to normalize monetary policy. Fed tightening is a potential risk to U.S. equities since the surge of liquidity in response to the pandemic likely provided much of the fuel for the stock market’s 20-plus month run. Any significant flattening of yield curve measures alongside further increases in inflation expectations and continued widening in high yield credit spreads could also prove to be potential headwinds for U.S. equities.

▶ European inflationary pressures are at all-time highs, and the ECB has already begun to taper its bond purchases. In addition, the widening of investment-grade credit spreads has decreased the attractiveness of the European equity markets. Momentum measures that previously benefitted European equities have also faded. In addition, the specter of a potential energy shortage in Europe this winter remains a potential risk to European economies, particularly if Russia takes measures to limit fuel supplies to Europe.

▶ Although Japanese equity markets remain relatively more attractive on a valuation basis, the flattening of the yield curve in Japan casts some doubt on growth prospects for the Japanese economy and has therefore reduced the attractiveness of Japanese equities in the short to medium term.

▶ The widening of high yield credit spreads in China, and the U.S. is negatively impacting Chinese equities. In addition, the situation in China remains uncertain due to the continuing pressure among Chinese real estate development firms to service their debt and uncertainty as to how the Chinese government will ultimately respond to this situation. However, the Chinese government recently announced its intention to focus once again on generating economic growth in China, which is a pivot away from recent more restrictive government economic policies. A concerted policy shift by the Chinese government could be positive for Chinese equities.

▶ A widening of the TED Spread in India (the difference between the interest rate that banks charge one another and the interest rate on short-term government debt) has recently negatively impacted the attractiveness of India equities. However, the India equity markets continue to benefit from a positively sloped yield curve measure, relatively benign inflation, and attractive long-term prospects for economic growth.

Fixed Income and Real Assets:

▶ Bonds: Even though the recent decline in interest rates has helped to somewhat boost the outlook for bonds, at current extraordinarily low yields the risk/return trade-off for U.S. Treasury securities is not compelling. In addition, U.S. Treasuries continue to maintain deeply negative real interest rates, meaning that yields are well below inflation expectations.

▶ Credit: The outlook for credit remains mixed. While there has been some widening in high yield and investment grade credit spreads recently, investors’ seemingly insatiable search for yield in today’s low-rate environment could continue to be supportive of corporate bond markets. However, any trouble in the credit markets could lead to a rapid widening of credit spreads which could prove to be a decidedly negative event for corporate bond holders.

▶ Gold: Gold remains attractive, particularly on a long-term basis, and is supported by a continuation of the current negative real interest rate environment (nominal interest rates minus expected inflation). However, further monetary tightening by the world’s major central banks may present a potential headwind to further upside for gold in the near term.

▶ Commodities: Although commodities remain relatively undervalued in our model research and potentially attractive over the longer term, the current environment of widening credit spreads, a stronger U.S. Dollar, the prospect of a Fed tightening highlights increased risks to commodities over the near term.

About 3EDGE

3EDGE Asset Management, LP, is a global, multi-asset investment management firm serving institutional investors, the advisor marketplace, and private clients. 3EDGE strategies act as tactical diversifiers, seeking to generate consistent, long-term investment returns, regardless of market conditions, while seeking to manage downside risks. The primary investment vehicles utilized in portfolio construction are index Exchange Traded Funds (ETFs). The investment research process is driven by the firm’s proprietary global capital markets model.

The model is tested over the widest variety of economic and market conditions and translates decades of research and investment experience into a system of causal rules and algorithms to describe global capital market behavior. 3EDGE offers a full suite of solutions, each with a target rate of return and risk parameters, to seek to meet investors’ different objectives. Of course, investing involves risks and the potential loss of your investment. There is no guarantee that any target return will be achieved.

DISCLOSURES: This commentary and analysis is intended for information purposes only and is as of December 10, 2021. This commentary does not constitute an offer to sell or solicitation of an offer to buy any securities. The opinions expressed in View From the EDGE® are those of Mr. Folts and Mr. Biegeleisen and are subject to change without notice in reaction to shifting market conditions. This commentary is not intended to provide personal investment advice and does not take into account the unique investment objectives and financial situation of the reader. Investors should only seek investment advice from their individual financial adviser. These observations include information from sources 3EDGE believes to be reliable, but the accuracy of such information cannot be guaranteed. Investments including common stocks, fixed income, commodities, ETNs, and ETFs involve the risk of loss that investors should be prepared to bear. Investment in the 3EDGE investment strategies entails substantial risks and there can be no assurance that the strategies’ investment objectives will be achieved. Real Assets (Gold & Commodities) includes precious metals such as gold as well as investments that operate and derive much of their revenue in real assets, e.g., MLPs, metals and mining corporations, etc. Intermediate-Term Fixed Income includes fixed income funds with an average duration of greater than 2 years and less than 10 years. Short-Term Fixed Income and Cash includes cash, cash equivalents, money market funds, and fixed income funds with an average duration of 2 years or less. Past performance is not indicative of future results. Intermediate-Term Fixed Income includes fixed income funds with an average duration of greater than 2 years and less than 10 years.