Major Indices Post Losses in Q3 2023

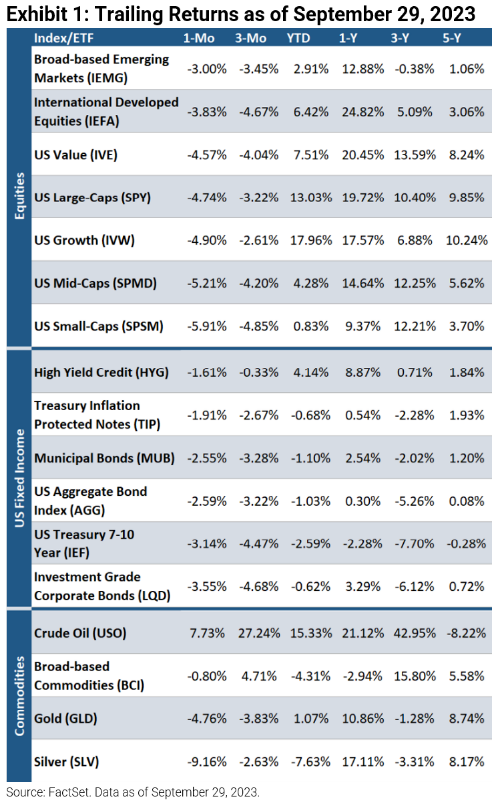

Amid higher for longer messaging from the Federal Reserve, rising longer-term US bond yields, and renewed inflation worries coupled with ascending oil prices, all three major US stock market indices were down in Q3. US small-caps (-4.9%) were among the worst performers, followed by international developed equities (-4.7%) and US mid-caps (-4.2%). Bonds were also down as investment grade corporates fell 4.7%, 7-10 year US Treasuries declined 4.5%, and municipal bonds decreased 3.3%. Commodities produced mixed returns as both crude oil and broad-based commodities were up (+27.2% and +4.7%, respectively) while gold and silver were down (-3.8% and -2.6%, respectively).

The Fed’s Hawkish Pause

The Federal Reserve left interest rates unchanged at the September FOMC meeting, leaving the fed funds rate at the 5.25–5.50% range. Participants have referred to this decision as a hawkish pause as Federal Reserve Jerome Powell expressed uncertainty regarding the US economy. With both annualized core CPI and PCE for August at nearly double the 2% target (4.3% and 3.9%, respectively), he stated the Fed is “prepared to raise rates further if appropriate,” and that rates will be kept at elevated levels until policymakers are confident that “inflation is moving down sustainably.” Updated dot plot projections revealed that 12 out of 19 officials see another 25 bps increase this year, and that 50 bps (two 25 bps cuts) that were expected in 2024 were removed. Moreover, the Fed doubled its GDP forecast for 2023 and increased the 2024 estimate from 1.1% to 1.5%, while lowering both 2023 and 2024 unemployment rate expectations, echoing their hawkish stance. In response, the yield on the 10 year Treasury surpassed 4.6% for the first time since 2007 as the bond market is convinced interest rates will stay higher for longer. As of September end, traders are currently pricing in an 18% chance of a 25 bps rate hike at the next FOMC meeting on November 1st.

Breakouts Imply Something will Break

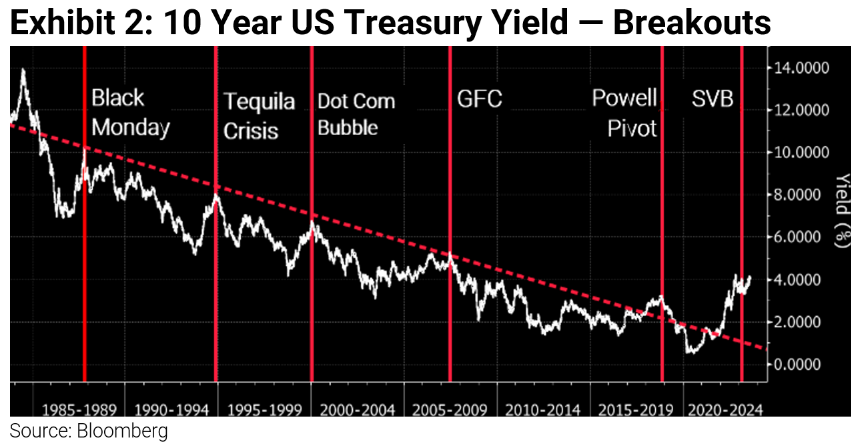

Yield breakouts, when bond yields surge higher than previous resistance levels, have historically coincided with the disruption of financial institutions or an economic downturn. As yields on longer dated bonds continue to rise, does this suggest something will soon break?

Bonds Over Equities?

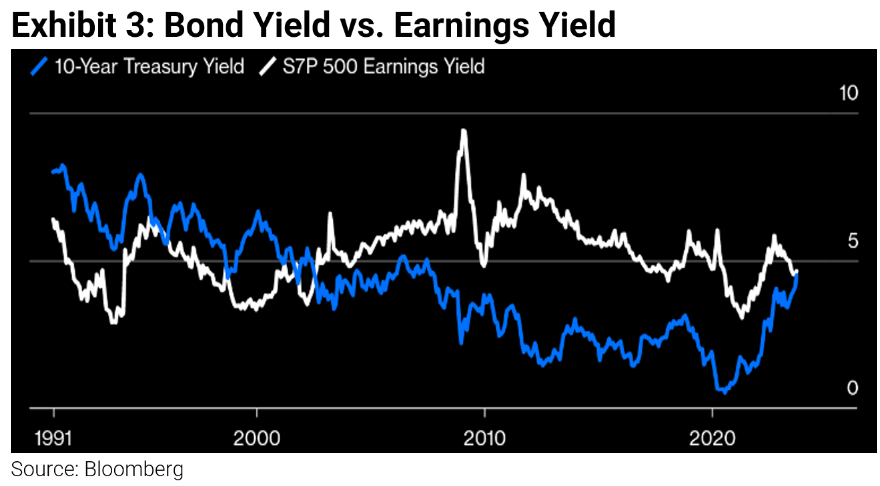

Elevated yields are not supportive for US large-cap index equities as future earnings are discounted at a higher rate. Additionally, Treasury bonds have minimal risk if held to maturity. Given the yield of the 10 year US Treasury bond is almost equal to the S&P 500’s earnings yield, is now a good time to buy bonds?

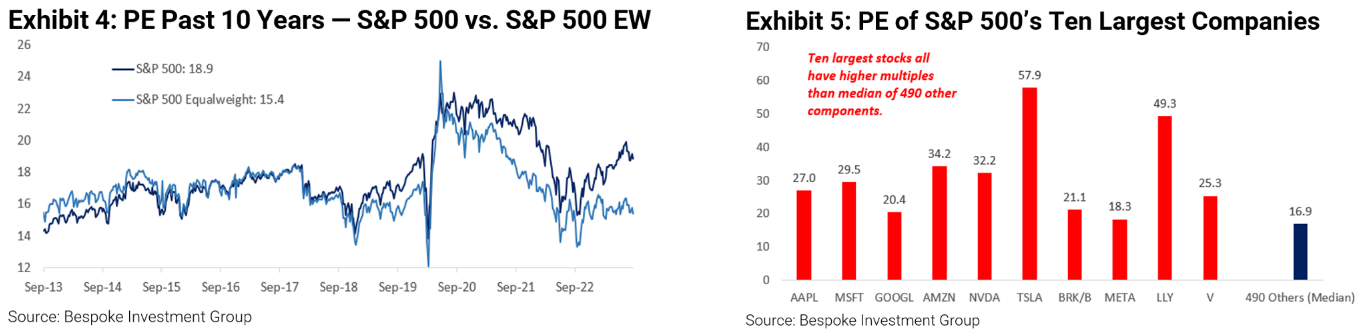

What Makes the S&P 500 So Expensive

The S&P 500’s PE of 19 is expensive relative to history, while the equal weighted S&P 500’s PE of 15 is much cheaper relative to both its market cap weighted counterpart and its own historical range. The difference can be attributed to the larger mega-cap stocks which have rallied significantly this year. Looking at the top ten largest stocks in the index, all of them trade at a higher multiple than the median of the remaining 490 companies (17x earnings), and all but one have a PE above 20.

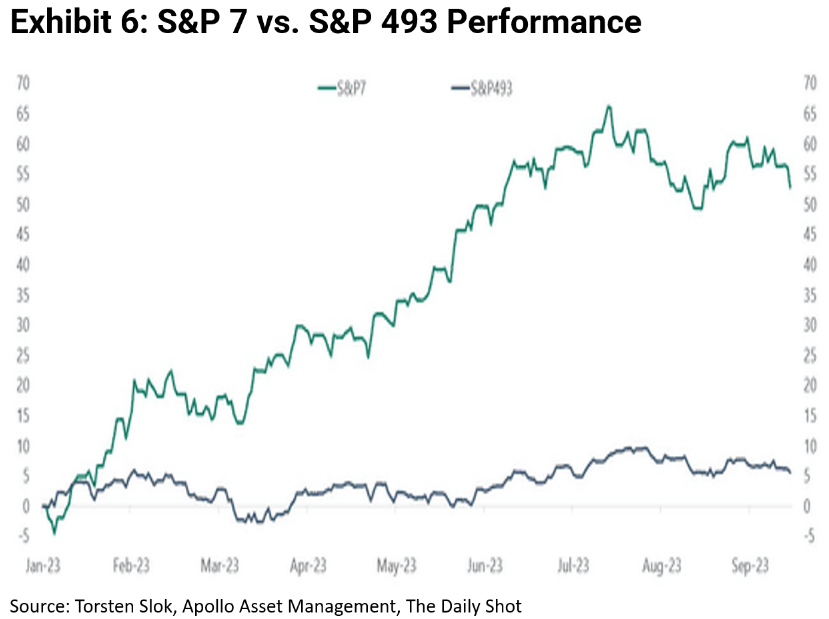

Market’s YTD Gain Driven by Few

It’s crucial to acknowledge a significant portion of the S&P 500’s 13% YTD gain is coming from only a handful of stocks. According to Apollo Asset Management, the 7 largest stocks in the index, otherwise known as the “magnificent seven,” or the S&P 7, are up approximately 50% YTD. These also make up almost 30% of the index alone, posing heightened concentration risk. Meanwhile, the remaining stocks in the index, or S&P 493, is only up 4-5% in 2023. What will happen to the S&P 500 if these seven stocks turn lower? We believe there is a once in a decade opportunity to purchase the broader US marketplace, excluding mega-caps, at an attractive valuation.

It’s Time to Rotate Out of Mega-Cap Expensive Tech Stocks and Into Europe, Japan, Real Assets, Structural Inflation Winners, and the Broader US Large-Cap and Mid-Cap Complex

The extraordinary crowding into the “magnificent seven” US stocks does not make us overly bullish. It’s important to keep in mind that bear markets and recessions have historically corresponded with a change in market leadership. We believe portfolios should be rebalanced away from the US mega-caps as US large-cap equity risk premiums are relatively unattractive.

Diversification is paramount. There are attractive areas of the market with catalysts for upside, i.e., Europe/Japan, US SMID, and structural inflation winners; i.e., the likely market leaders in a post-high real rate, higher inflation world. In the case of Europe and Japan, both have attractive estimate revisions and earnings momentum, are cheaper than the US market, and are further behind the interest rate cycle.

We’ve had the fastest rate hiking cycle in half a century, and core PCE is still nearly double the Fed’s inflation target. As we enter a world of deglobalization, onshoring, reshoring, one should own real assets and stocks in sectors such as industrials, materials, energy, etc. In our view, there’s too much emphasis on trying to figure out the next rate hike. We think what’s more important is building a portfolio that can sustain a world of higher real rates and stubbornly high inflation.

Warranties & Disclaimers

As of the time of this publication, Astoria Portfolio Advisors held positions in IEMG, IVE, SPMD, SPY, SPSM, IVW, IEFA, MUB, TIP, AGG, IEF, HYG, LQD, BCI, GLD, USO, SLV, AAPL, MSFT, GOOGL, NVDA, META, LLY, and V on behalf of its clients. There are no warranties implied. Past performance is not indicative of future results. Information presented herein is for educational purposes only and does not intend to make an offer or solicitation for the sale or purchase of any specific securities, investments, or investment strategies. Investments involve risk and, unless otherwise stated, are not guaranteed. The returns in this report are based on data from frequently used indices and ETFs. This information contained herein has been prepared by Astoria Portfolio Advisors LLC on the basis of publicly available information, internally developed data, and other third-party sources believed to be reliable. Astoria Portfolio Advisors LLC has not sought to independently verify information obtained from public and third-party sources and makes no representations or warranties as to the accuracy, completeness, or reliability of such information. Astoria Portfolio Advisors LLC is a registered investment adviser located in New York. Astoria Portfolio Advisors LLC may only transact business in those states in which it is registered or qualifies for an exemption or exclusion from registration requirements.

For more news, information, and analysis, visit the ETF Strategist Channel.