By Dan Weiskopf, Portfolio Manager for Toroso Investments

The claims that ETF fixed income provides efficient market access are being tested during this period of disruption while equity ETFs are trading mostly seamlessly. There are multiple reasons for this. Perhaps the main reason is due to the fact that not all bonds trade every day, so pricing services are relied upon to provide quotes. Therefore, fixed income ETFs are arguably a secondary source of price discovery. The primary source would be large, direct institutional buyers. However, given the nature of the thousands of bond cusip numbers available, and the fact that most bonds are owned and not traded, this price discovery is simply not as active as in equities. This means that pricing may be impaired right now and investors should be looking closely. Clearly, risk of credit impairment exists, but how to price that risk is still in question. In certain cases, prices are now back to 2009 levels despite the positive trends in lower interest rates. Most importantly, investors will look to confidence in credit as an indication of overall market stability.

Quick Background:

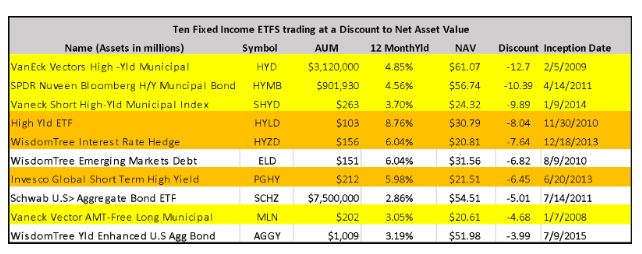

There are 419 fixed income ETFs with assets under management (AUM) of about $827 billion. According to Bloomberg, over this past year, fixed income has seen AUM inflows of $164 billion and almost $36 billion YTD. Last year’s flows in fixed income almost eclipsed equity flows. However, what should be more interesting to investors is the opportunity to further capitalize on the trend in lower interest rates by taking risks on current discounts in the ETF market and the baskets of bonds they currently represent. Credit is on sale!

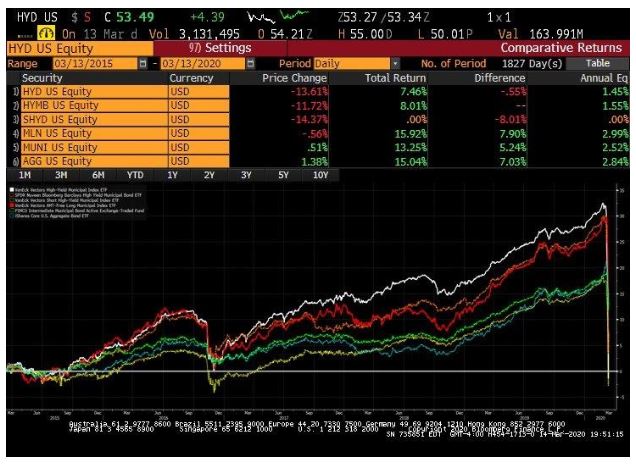

To identify some quick opportunities, I screened for discounts of greater than 3% and ETFs with more than $100 million in AUM. Frankly, I was surprised to find so many opportunities. I can share the full list upon request if you email me. I have highlighted the municipal bond categories in yellow and high yield in gold. Examples of extreme potential mispricing can be found in HYD, HYMB, SHYD, HYLD, HYMB. As the chart below illustrates, the disruption in the fixed income market for municipal bonds and high yield has been especially pressing.

High Yield ETF: HYLD, HYZD, PGHY

All three ETFs highlighted in gold are relatively small in terms of AUM. This may impact the way the ETF trades, and could be part of the reason the discounts exist. However, the fact that High Yield Fund (HYLD) is actively managed, unlike the other two ETFs, is noteworthy. HYLD’s duration is also about 2 years, which includes 20% in bank loans. The managers have already put out a COVID-19 statement, found here: https://hyldetf.com/

Municipal Bond ETFs: (HYD, HYMB, SHYD, VLN)

Our ETF Professor, Dan Weiskopf, wrote about HYD for ETF.com in 2012 and 2014. His 2014 interview with the Van Eck municipal bond portfolio manager Jim Colby is, in certain ways, foretelling on why this could be an opportunity for investors. Jim is the portfolio manager of passive indexes, which means his role is in credit research, and he filters through thousands of securities offered by dealers. For example, HYD owns over 2,200 securities. Investors looking at the fixed income ETF space would benefit from reading the interview. https://www.etf.com/sections/features/21138-structure-matters-colby-on-muni-bond-etfs.html?nopaging=1

Investors should also note that this high yield fund is targeted at long duration, and therefore its price may be part of the issue for the discount to the Net Asset Value. The details for this fund, as well as the other municipal bond funds Jim Colby manages, can be found here. https://www.vaneck.com/etf/income/hyd/portfolio-analytics/

Are Bond ETFs Broken?

Are Bond ETFs Broken?

Dave Nadig covered this question in depth below:

https://www.etftrends.com/bond-etfs-had-a-wild-day-but-did-they-break-i-think-not/

All in all, we agree with his conclusion. The ETFs are trading orderly and reflecting the liquidity concerns with the actual bonds in the portfolios. Transparency and liquidity are some of the key client alignment growth factors for ETFs. However, when ETFs shine the light of transparency on less liquid assets, investors may not like what they see. In summary, the ETFs are more liquid than the underlying bonds, so small disconnections are expected in times of extreme stress. We don’t believe something is broken, but as stated by Reggie Browne, we need to learn from this and improve.

The market is on sale; where are the coupon clippers?