The saga of the coronavirus disease or COVID-19 has evolved into a global concern in the last couple of weeks. The virus, while now apparently on the decline in China, has spread to more than 60 countries, with the US experiencing its first virus fatality over the weekend. The global nature of COVID-19 is causing consumers and companies to change behaviors, as reflected in China’s record low in recent manufacturing surveys. These changes are causing investors to start worrying about a recession in 2020. As a result, the S&P 500 dropped 15% from its all-time high just 8 trading days ago, experiencing its worst single week since 2008. A global ‘flight to safety’ has driven the 10-Year Treasury yield to nearly 1% and oil prices under $50.

RIVERFRONT’S PLAYBOOK FOR THE UNEXPECTED: TRUST THE PROCESS

The fear of the unknown can be gripping. This fear often leads to panicked selling as investors start to discount a worst-case scenario. While we have no unique insight on how or when this particular panic will end, we think the ‘worst case scenario’ often proves to be too punitive. For this reason, we think it’s important to take a deep breath and trust a well-constructed process to remove emotionality from decision making.

- Strategic Process: We build portfolios targeting investment horizons that range from 3 years to 10+ years, stress-testing them through past recessions and similar historical shocks. As a result, our shorter-horizon portfolios incorporate a conservative strategic asset allocation.

- Tactical Process: Historical review suggests that the recent sell-off may eventually present a buying opportunity, as we believe COVID-19 is unlikely to be a sustained economic issue. Thus for longer horizon investors, we suggest not selling into the current decline, and so far we have chosen to remain at current risk levels in our longer-horizon portfolios.

- Risk Process: To further protect principal from market volatility, our tactical risk management process is most acutely focused on the shorter-horizon portfolios, where we recently reduced risk and raised cash. For our longer-horizon portfolios, although we have not taken action, we are monitoring events closely. Additionally, since equities often quickly recover, reinvestment plans need to be decided at the time of sale and implemented when appropriate.

MAINTAINING PERSPECTIVE: HISTORY SUGGESTS SHOCKS ARE TRANSITORY

At RiverFront, our overall view remains that a non-financial ‘black swan’ event – such as a terrorist attack or a global epidemic like COVID-19 – is likely to have a negative near-term impact on the affected region’s economy, but that effect usually rights itself within a quarter or two. Similar double-digit stock sell-offs occurred after the SARS outbreak in 2003 and the 9/11 attacks in 2001. Global stocks ultimately recovered their losses in both cases. This is because risks cannot be viewed in isolation and tend to be met with countermeasures by policymakers.

CAN POLICYMAKERS MITIGATE A GLOBAL RECESSION?

While there remains skepticism about the limits of central bank accommodation, we believe that lower interest rates do have a positive effect on economic output through the transmission mechanism of housing, lending, and consumer and business confidence. As an example, the yield on 10-Year Treasuries has dropped roughly 80 basis points (bps = 1/100th of 1%) and West Texas Intermediate (WTI) Crude Oil has dropped nearly $14 since the beginning of the year. The combined effect has the potential to lower mortgage payments for those choosing to refinance and give consumers a needed income boost through lower gasoline prices.

Fed funds futures markets are already pricing in a high likelihood that the Federal Reserve lowers interest rates in March and again later in the year, and international central banks like the European Central Bank, Bank of Japan and People’s Bank of China are following suit with stimulus of their own. To this end, Fed Chair Jerome Powell helped spark a mini-rally after he mentioned the Fed will “use its tools and act as appropriate to support the economy.” We anticipate a coordinated response by the world’s central banks, which we think could help restore fragile investor confidence. Investors shouldn’t forget that policymakers also have a toolkit beyond just interest rates, and that definitive communication around a commitment to reflation can have significant impact on business confidence and financial conditions.

RISK MANAGEMENT: NEXT TECHNICIAL LEVELS OF SUPPORT

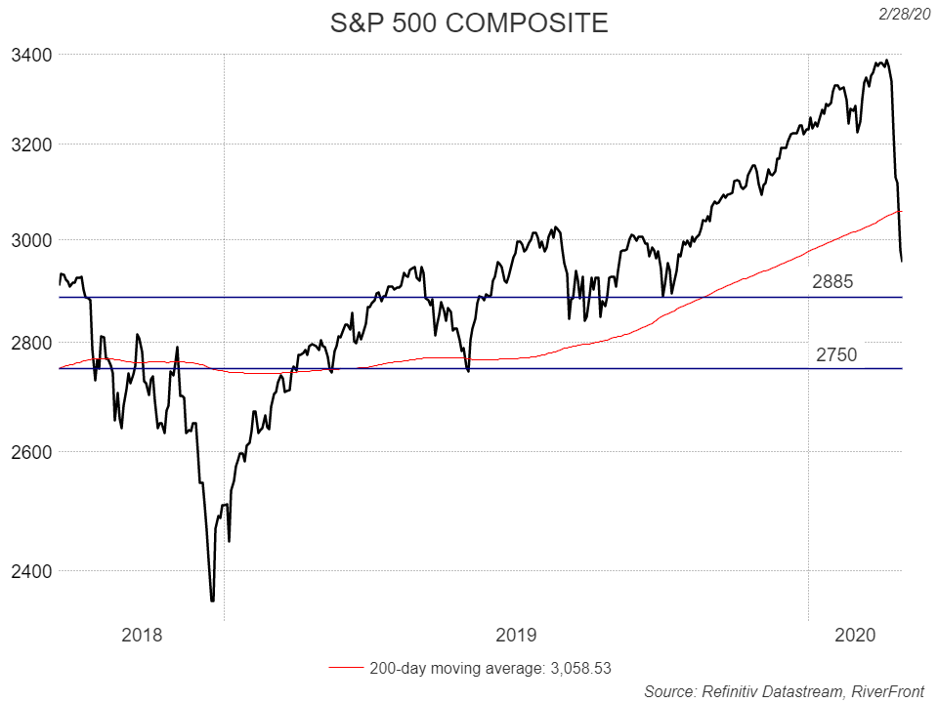

As our chart below shows, the speed of the sell-off over the past week is of a different, more pernicious nature than anything we’ve experienced recently. Our first set of trailing risk management stops, a discipline we consistently monitor in good times or bad, were violated last week. In swift fashion, the S&P 500 violated what we would view as important support level at 3045 (200-day moving average) and is seeking to find support at 3000, an important psychological level. This may mean the market may not be quick to right itself in the near-term. We believe the next meaningful support exists around the 2845 level and, below that, at 2750. These may be viewed as important risk management alerts, in our opinion.

Past performance is no guarantee of future results. Not indicative of RiverFront performance. Shown for illustrative purposes only. It is not possible to invest directly in an index.

APPENDIX: WHAT WE KNOW ABOUT COVID-19 SO FAR

COVID-19 is a unique challenge for investors, with so much still unknown both about the disease and its ultimate effects on the global economy. However, as the epidemic enters its 2nd month and the worldwide infection rate nears 100,000, some characteristics are becoming clearer. Ironically, the more we learn about the virus, the less ‘existential’ its risks appear.

It does not appear nearly as dangerous as many past global epidemic concerns, such as SARS or Ebola. A quote from the Wall Street Journal last Thursday: “SARS killed about 10% of the people it infected, while about 2.9% of the people confirmed to be infected with this new coronavirus have died, according to World Health Organization data.” It’s also reasonable to believe that the ultimate mortality rate of COVID-19 will be lower than the current rate, simply because its asymptomatic nature (many carriers will never show symptoms) means that scientists are probably understating the total infection rate currently.

It does not appear to be mutating. COVID-19 has remained genetically stable so far, according to the US CDC.

There are no known vaccines or treatments approved yet, but several are in development. Technological progress in the last few years means that the genetic code of COVID-19 has been sequenced and decoded much faster than prior epidemics, leading to accelerated vaccine development (source Wall Street Journal, 2/25/20). In addition, existing anti-viral drugs that were effective on Ebola are also being tested.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Past results are no guarantee of future results and no representation is made that a client will or is likely to achieve positive returns, avoid losses, or experience returns similar to those shown or experienced in the past.

Information or data shown or used in this material is for illustrative purposes only and was received from sources believed to be reliable, but accuracy is not guaranteed.

In a rising interest rate environment, the value of fixed-income securities generally declines.

Technical analysis is based on the study of historical price movements and past trend patterns. There are no assurances that movements or trends can or will be duplicated in the future.

Investing in foreign companies poses additional risks since political and economic events unique to a country or region may affect those markets and their issuers. In addition to such general international risks, the portfolio may also be exposed to currency fluctuation risks and emerging markets risks as described further below.

Changes in the value of foreign currencies compared to the U.S. dollar may affect (positively or negatively) the value of the portfolio’s investments. Such currency movements may occur separately from, and/or in response to, events that do not otherwise affect the value of the security in the issuer’s home country. Also, the value of the portfolio may be influenced by currency exchange control regulations. The currencies of emerging market countries may experience significant declines against the U.S. dollar, and devaluation may occur subsequent to investments in these currencies by the portfolio.

Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the U.S. and are considered speculative and subject to heightened risks in addition to the general risks of investing in non-U.S. securities. Also, inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

Standard & Poor’s (S&P) 500 Index measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

It is not possible to invest directly in an index.

Riverfront Investment Group, LLC (“Riverfront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. Riverfront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in Riverfront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated (“Baird”), a registered broker/dealer and investment adviser. Opinions expressed are current as of the date shown and are subject to change.

RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated (“Baird”), a registered broker/dealer and investment adviser.

Copyright ©2020 RiverFront Investment Group. All Rights Reserved. 1106321