For most of the last fifty years, fixed income investing has been characterized by owning some combination of Municipals, Corporates, Treasuries and Agency Mortgage-Backed Securities. Of course, investors have occasionally added Preferreds and a few other products to their portfolios, but the core holdings have largely stayed consistent. This strategy aligned well with periods of secular disinflation and slow nominal growth.

However, the effects of deglobalization, expanding budget deficits, structural labor shortages and insufficient commodity and infrastructure investment could result in secularly higher rates and volatility, which may necessitate an alternative approach to fixed income asset selection: One that is more tactical, liquid and able to adapt to earnings and liquidity cycles while finding relative value.

For example, investors looking to rebalance fixed-income portfolios heading into the new year are faced with a serious issue. If they follow accepted norms and buy an index-focused fund, 25-35% of those will likely be held in investment grade (IG) corporate bonds. But IG bonds have become one of the worst relative value instruments in fixed income, with future returns skewed significantly to the downside because IG spreads are among the tightest (most expensive or overvalued) levels in history.

Although products to manage such a landscape have been available for decades, their accessibility to the individual investor has been limited. That is no longer the case. The proliferation of fixed income ETFs means the entirety of the world’s fixed income options is no longer just for hedge funds and high fee money managers. Retail investors can now invest in almost any corner of the fixed income world at a low cost and with tremendous liquidity. One such sector that we have been capitalizing on for years are Collateralized Loan Obligations (CLOs). While CLOs may not suit every economic environment, they have recently become a valuable tool for RBA in navigating the post-COVID higher rate landscape and present a compelling investment opportunity in an accelerating profit cycle. If these backdrops change, however, the liquidity of CLO ETFs allows RBA to adapt accordingly.

CLOs have been around since 1992, but have generally only been available to banks, hedge funds and large institutional buyers. Like traditional corporate debt, CLOs are sensitive to the earnings cycle and are grouped by default risk ratings. Like bank loans, they are floating rate instruments with attractive coupons. And like high yield (HY) corporates, they offer superior yields to the broad corporate market.

High grade and high yield corporate spreads are as expensive as ever, but the accelerating earnings cycle and low historical default risk suggest CLOs offer an opportunity to capture the characteristics of high-quality corporates without the overly rich valuation and duration risk.

In the below pages we will outline the CLO structure and why RBA is comfortable with the risks associated with owning CLOs vs other sectors of the fixed income market like IG and HY corporates.

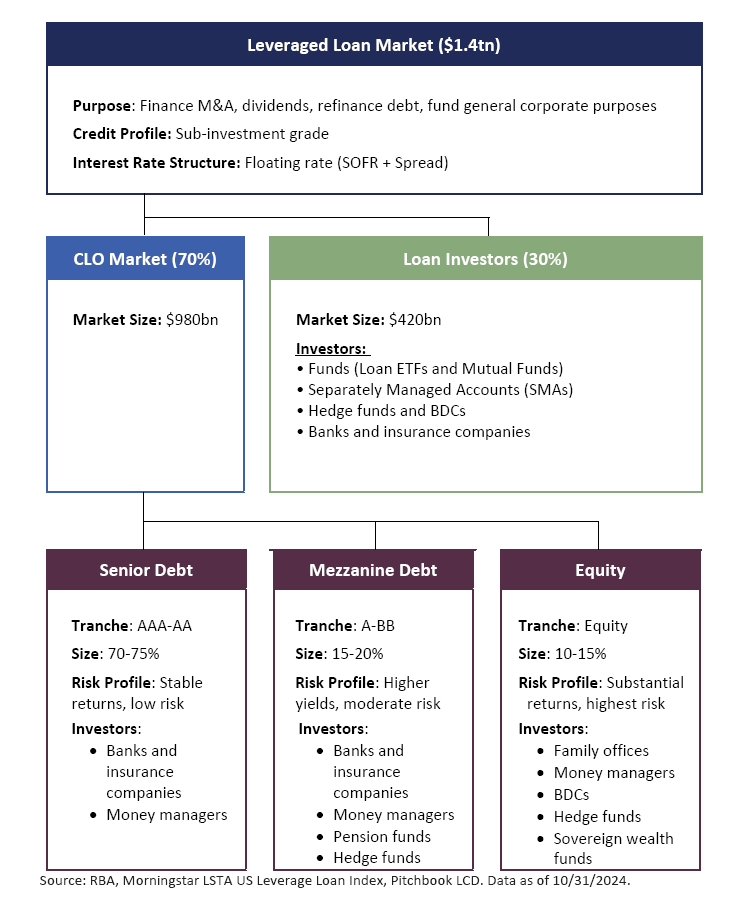

What is a Collateralized Loan Obligation (CLO)?

- At its core, a Collateralized Loan Obligation (CLO) is simply a pool of corporate loans whose cash flows are divided amongst a group of investors. This is known as the “collateral pool.”

- These corporate loans are mostly floating rate and sub-investment grade and are the same loans one might find in a bank loan ETF or mutual fund.

- The difference between owning a CLO and owning a bank loan ETF is that the CLO has layers of protections called tranches, whereas the bank loan investor is the first loss (equity) holder.

- The loan market is roughly the same size as the high yield market ($1.2tn) and CLOs own about 70% of all syndicated bank debt.

- The below graphic shows the general structure of the loan and CLO market along with the issuers and buyers of these instruments:

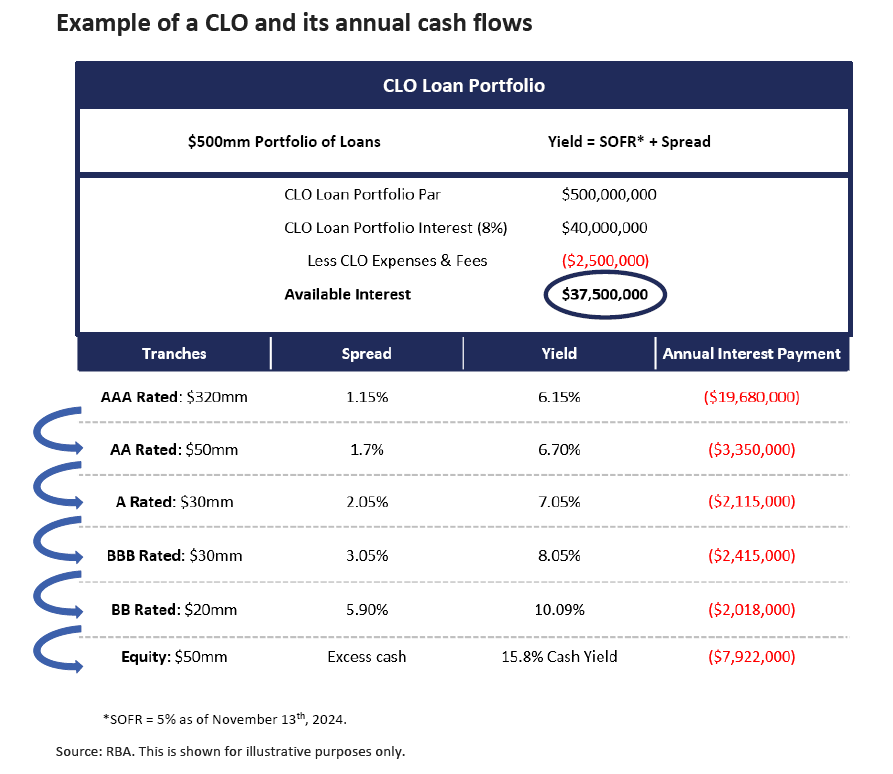

How is a CLO constructed?

- A CLO manager raises capital by issuing CLO securities (tranches).

- Using this capital, the CLO manager buys a pool of corporate loans.

- These loans generate cash flows that are then distributed back to the investors.

- The priority of payments is determined by which tranche the investor purchases, the AAA tranches is paid before the AA tranche, which is paid before the A tranche, etc. The equity tranche receives any excess interest.

- The underlying loans as well as the tranches are floating rate securities.

Example of a CLO and its annual cash flows

This sounds like a CDO… how is it different and what are the risks?

- The Collateralized Debt Obligations (CDOs) that contributed to the Financial Crisis were low quality, highly correlated subprime housing debt sensitive to one sector of the economy, housing. CLOs are diversified pools of corporate debt and are thus sensitive to corporate health. This is not to absolve the collateral pool of a CLO of risk. But for one to be worried about the correlation of default risk in a CLO, one must also have equal to greater worry about the high yield and bank loan market.

- CLOs are typically structured with covenants and protections that CDOs never enjoyed, including overcollateralization, interest coverage, reinvestment, collateral quality, par coverage and minimum weighted average coupon tests (defined in Appendix).

- CDO risks were misrepresented due to lax underwriting standards and poor structuring. CLOs are under much more scrutiny and CLO managers now generally hold the equity tranche of their deals, incentivizing proper management.

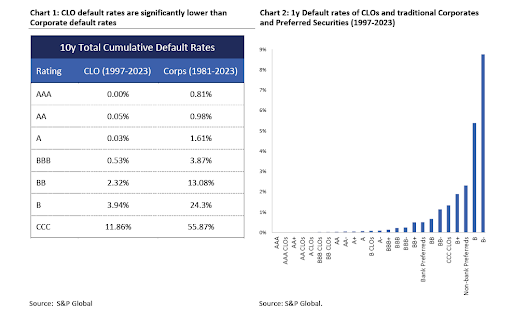

- Because of their higher quality and structure, the default risks of a CLO are extraordinarily small, especially when compared to corporate bonds.

- On a rolling 10y cumulative default loss basis (Chart 1), BBB CLOs have less default risk than AAA Corporate bonds and on a 1-year default basis (Chart 2), CLOs are among the least risky fixed income instruments.

RBA owned AAA CLOs during the profit recession of 2022 and BBB CLOs since early 2024. With improving corporate earnings and low default rates, why do BBB CLOs offer such an attractive yield?

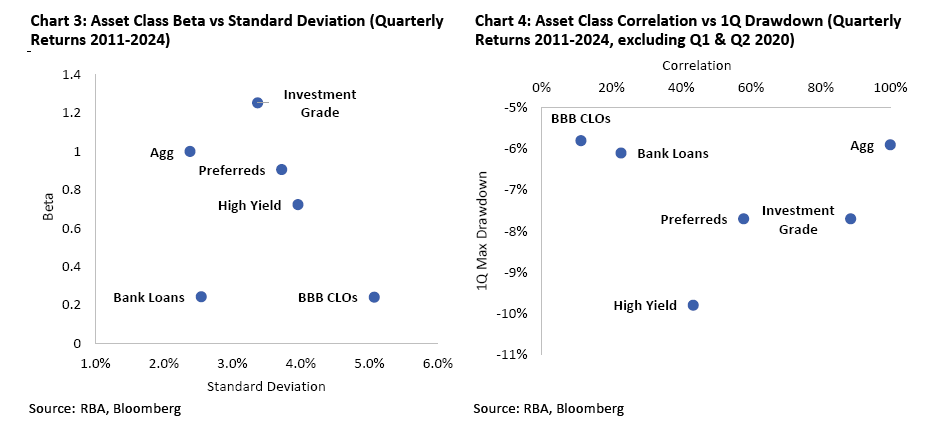

- Due to their high return volatility (1.5x that of the IG corporate market), investors will naturally demand a higher spread (lower valuations) for BBB CLOs despite the low default risk.

- However, it is important to note that notwithstanding a higher standard deviation, BBB CLOs also have low beta and low correlations to the broad bond indices, and outside of what turned out to be a two-quarter roundtrip of a large drawdown in 2020, have lower drawdown risk than other corporate debt and the Bloomberg Aggregate Index.

- Given their structure, investors demand a complexity premium to owning CLOs.

- The underlying tranches of a BBB-rated CLO are relatively illiquid compared to traditional corporate debt, which creates an illiquidity premium. However, the ETF structure allows retail investors to benefit from this illiquidity premium while still enjoying the added liquidity of the ETF itself.

- CLOs are floating rate, so their risk-free reference rate today (SOFR: 5.05% as of November 12th, 2024) is higher than a 10-year fixed rate bond’s risk-free reference rate (10-year Treasuries: 4.42% as of November 12th, 2024).

By Michael Contopoulos, Director of Fixed Income

For more news, information, and strategy, visit the ETF Strategist Channel.

Appendix:

1. Overcollateralization (OC) Tests

- Purpose: Ensure there is enough collateral to cover the liabilities of the CLO at each level of debt.

- Mechanism: The OC test compares the value of the collateral pool to the outstanding balance of each tranche. If the test fails (i.e., collateral value falls below a certain threshold), cash flows are diverted from the equity tranche and junior tranches to pay down senior debt, which helps restore coverage.

2. Interest Coverage (IC) Tests

- Purpose: Ensure there is sufficient interest income from the collateral to cover the interest obligations for each debt tranche.

- Mechanism: The IC test compares the income generated by the collateral to the interest due on each tranche. If the test is not met, cash flows that would have gone to lower tranches (including equity) are redirected to pay down senior debt, securing coverage and protecting senior investors.

3. Reinvestment Tests

- Purpose: Limit the reinvestment of principal proceeds to maintain portfolio quality.

- Mechanism: During the reinvestment period, the collateral manager can reinvest principal proceeds if the CLO meets certain conditions, including quality and diversification tests. If any test fails, reinvestment is restricted, and excess cash flow may be used to pay down the senior tranches.

4. Collateral Quality Tests

- Purpose: Maintain the credit quality of the loan portfolio.

- Examples:

- Weighted Average Rating Factor (WARF) Test: Limits the average credit risk by measuring the weighted average rating of loans in the CLO.

- Weighted Average Spread (WAS) Test: Ensures the portfolio earns sufficient interest to cover the CLO’s debt payments.

- Diversity and Concentration Limits: Prevent excessive exposure to single industries or issuers to maintain portfolio diversity.

5. Par Coverage Tests

- Purpose: Ensure that the principal value of the portfolio exceeds the par amount of the outstanding debt.

- Mechanism: This test evaluates whether the principal balance of the loans in the CLO exceeds the target value. If the test fails, excess cash flow may be redirected to pay down senior debt to reduce risk.

6. Minimum Weighted Average Coupon (WAC) Test

- Purpose: Maintain a minimum average coupon rate across the portfolio.

- Mechanism: Ensures the CLO portfolio earns a sufficient level of interest to meet its obligations. Failing this test can restrict cash flow to junior tranches.

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. RBA information may include statements concerning financial market trends and/or individual stocks, and are based on current market conditions, which will fluctuate and may be superseded by subsequent market events or for other reasons. Historic market trends are not reliable indicators of actual future market behavior or future performance of any particular investment which may differ materially, and should not be relied upon as such. The investment strategy and broad themes discussed herein may be inappropriate for investors depending on their specific investment objectives and financial situation. Information contained in the material has been obtained from sources believed to be reliable, but not guaranteed. You should note that the materials are provided “as is” without any express or implied warranties. Past performance is not a guarantee of future results. All investments involve a degree of risk, including the risk of loss. No part of RBA’s materials may be reproduced in any form, or referred to in any other publication, without express written permission from RBA. Links to appearances and articles by employees of Richard Bernstein Advisors, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial adviser and in light of his or her own circumstances, including the investor’s investment horizon, appetite for risk, and ability to withstand a potential loss of some or all of an investment’s value. Graphs, charts, and tables are provided for illustrative purposes only. Investing is subject to market risks. Investors acknowledge and accept the potential loss of some or all of an investment’s value. Views represented are subject to change at the sole discretion of Richard Bernstein Advisors LLC. Richard Bernstein Advisors LLC does not undertake to advise you of any changes in the views expressed herein.