By Chris Konstantinos, CFA, Director of Investments, Chief Investment Strategist

SUMMARY

- We believe the recent Chinese ‘offshore’ stock sell-off is unlikely to be the catalyst for the end of the US stock rally, in our opinion.

- China appears to be prioritizing social stability and political aims over shareholder protection and corporate profits, in our view.

- We see this episode as emblematic of the ‘New Cold War’ between the US and China.

- In May, we trimmed weightings to Chinese shares in our balanced portfolios and prefer US and European shares.

Chinese stocks under fire…but issues largely isolated to China

In an otherwise relatively uneventful summer for global stocks, it has been a wild couple of weeks for ‘offshore’ Chinese shares – companies domiciled in mainland China but traded on foreign exchanges. Since July 24, Chinese stocks listed on US exchanges wiped out $400 billion in market value. Given that China is the single largest country weighting in broad emerging markets (EM) indexes, this selloff has become a focus for global investors nervous about this downturn triggering broad contagion in world stocks.

What Triggered the Selloff…and What It Means for Global Stocks?

The catalyst for the selloff has been increased Chinese regulatory scrutiny in certain fast-growing sectors, such as for-profit education, internet, and property management. We do not expect this regulatory pressure– and the associated uncertainty it brings – to clear up soon, and thus we expect it to remain a drag on Chinese stocks in the near-term. However, we also believe that the issues currently plaguing Chinese shares are generally China-specific, and do not expect China to be the catalyst for a significant broader sell-off in the US stock market. To this end, we would note that over the past week or so, the S&P 500 made another new all-time high even as Chinese indices were plummeting (see chart, above).

RiverFront’s balanced asset allocation portfolios trimmed their weighting in Chinese and broad EM shares from an overweight positioning to slightly underweight back in May, maintaining no direct exposure at all to China in our two shortest-horizon models. We continue to favor US stocks over international equities, with a selection preference within international for European versus Asian shares, including China.

Past performance is no guarantee of future results. Shown for illustrative purposes. Not indicative of RiverFront portfolio performance. Index definitions are available in the disclosures.

Why China Is Scrutinizing Highly Profitable Companies?

On July 24, Chinese authorities released new regulations for ‘for-profit’ education companies. The new regulations include forcing tutoring and education services companies to convert to non-profit status and disallowing foreign curriculums or foreign teachers from teaching remotely in China. This comes on the heels of an ongoing debate among Chinese citizens surrounding tutoring. Many view expensive tutoring as an unfair advantage that helps wealthy students score well on the ‘gaokao’, the Chinese entrance exam crucial for university admittance. These regulations also allow the state to keep a tighter lid on what foreign ideologies are taught to students.

Chinese authorities have also been targeting powerful technology companies that are viewed as monopolies, national security risks, or threats to the social fairness and stability aims of the Chinese Communist Party (CCP). This often affects these companies’ business models and ability to float shares on foreign exchanges. Last month, Chinese ride-sharing company Didi had its mobile app banned over data security issues, just after the firm’s $4 billion US initial public offering (IPO) on the NYSE. Shortly thereafter, Beijing announced a planned review of overseas listings of all Chinese internet companies with more than a million users. Last November, lending giant Ant Financial was forced to suspend their US IPO and change their business model. Other massive internet companies such as Alibaba and TenCent –companies with a large following among Western investors – have felt the wrath of government scrutiny recently, as the state became increasingly concerned with control.

The Chinese state’s recent crackdown has also extended to powerful businesspeople; Sun Dawu, a Chinese billionaire agricultural mogul, was sentenced this week to 18 years in prison. Some China watchers believe the charges against him were largely motivated by Sun’s friendships and ties with political dissidents.

Communist China Prioritizing Social and Political Aims Over Shareholder Returns

Does this mean that the Chinese government is at ‘war with its own private sector’, as some have suggested? Not exactly…we instead view recent events as a vivid reminder that the overarching aims of communist China have never sat comfortably next to the pursuit of corporate profit. It is clear to us that President Xi and the CCP will continue to prioritize social order over ‘capitalist’ concerns such as return-on-equity or stock prices. These types of moves are designed in part to avoid mass uprising in a nation of 1.3 billion people. China is also increasingly concerned about maintaining state control over homegrown consumer and lending data and access.

We believe that the upshot of this is that high-growth Chinese stocks in sectors that touch or collect data on the Chinese consumer – education, housing, food delivery, lending, and internet commerce among them- are likely to remain on discount. It is not lost on us that ‘offshore’ Chinese public stocks have thus far fared much worse in the sell-off than local-listed China shares (see chart, first page), which suggests to us that the pain being felt in Chinese stock markets is disproportionately borne by international (Western) shareholders in China.

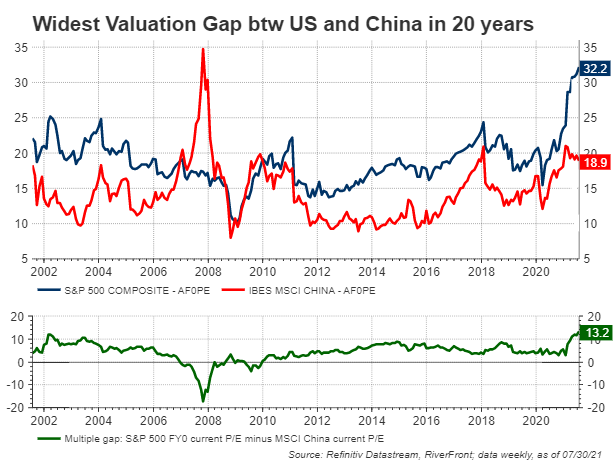

These shareholders going forward may have to continue to assign a consistent ‘uncertainty’ discount to Chinese shares in these areas, regardless of structural growth and profitability prospects. For comparison’s sake, the valuation of the MSCI China stock index – a Chinese index widely-followed in the West, which is roughly a third technology stocks and has behaved similarly in the selloff to pure offshore Chinese indices. MSCI China is currently trading at the cheapest valuation discount – over 13x multiple points – relative to the US bellwether S&P 500 index in 20 years, as judged by trailing year price-to-earnings ratios (see bottom chart, right). However, we think it’s too early to try and ‘bottom-fish’ in these China names, as this uncertainty is unlikely to abate anytime soon.

Past performance is no guarantee of future results. Shown for illustrative purposes. Not indicative of RiverFront portfolio performance. Index definitions are available in the disclosures.

Grievances Between the US and China Deepening

In addition to the events of the last couple of weeks, there is a growing laundry list of grievances between the world’s first and second-largest economies. This is epitomized by the trade war of the last few years, the US’s outspoken stance on human rights abuses in Hong Kong and Xinyang, the US probe into the origins of COVID-19, and President Xi’s aggressive rhetoric towards the West during the CCP’s 100-year anniversary celebration of the party’s founding in July.

For the US’s part, the Biden administration seems to be doubling down on former President Donald Trump’s adversarial stance against Chinese tech companies thought to aid and abet IP theft and cyber espionage. While in office, President Trump released a ‘blacklist’ that prevented US investors for owning stakes in roughly 30 Chinese companies due to national security concerns. In June, President Joe Biden added almost 30 more names to the list, including telecom equipment giant Huawei and other large Chinese telecom companies.

In addition, Securities and Exchange Commission (SEC) Chairman Gary Gensler on Friday said he has asked SEC staff to seek specific disclosures from Chinese firms before signing off on pre-IPO filings, according to the weekend edition of the Wall Street Journal. In an extreme scenario, it’s possible that internal pressure in both the US and China could eventually lead to Chinese companies delisting en masse on US exchanges, though for their part Chinese securities regulators tried to downplay these risks in their address to investors on Wednesday.

Conclusion: The New ‘Cold War’ Enters the Next Phase – We Prefer US and European Stocks to Chinese Ones

All of this appears to us as a continuation of the ‘New Cold War’ between China and large Western economies like the US. We first made mention of this new Cold War in our June 2020 Weekly View entitled China, COVID-19, and the New ‘Cold War’. We believe this will continue to put a ceiling on US-listed China shares for the foreseeable future, as Beijing pivots away from a focus on profit maximization towards social initiatives.

Given China’s volatility and increasing government intervention in their capital markets, we think Chinese equity exposure should be limited for some conservative Sustain and Distribute investor profiles. For long-term Accumulate investors, we continue to favor an active strategy, currently preferring US stocks over international equities. Within international allocations, we have a selection preference for European over Asian shares. Within broad emerging markets, investors are forced to weigh the positives of attractive long-term value and leverage to global reflation with these structural risks, though we would note the economies of other Asian countries such as Korea, India, and Taiwan continue to fare relatively well.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

In a rising interest rate environment, the value of fixed-income securities generally declines.

When referring to being “overweight” or “underweight” relative to a market or asset class, RiverFront is referring to our current portfolios’ weightings compared to the composite benchmarks for each portfolio. Asset class weighting discussion refers to our Advantage portfolios. For more information on our other portfolios, please visit www.riverfrontig.com or contact your Financial Advisor.

Investing in foreign companies poses additional risks since political and economic events unique to a country or region may affect those markets and their issuers. In addition to such general international risks, the portfolio may also be exposed to currency fluctuation risks and emerging markets risks as described further below.

Changes in the value of foreign currencies compared to the U.S. dollar may affect (positively or negatively) the value of the portfolio’s investments. Such currency movements may occur separately from, and/or in response to, events that do not otherwise affect the value of the security in the issuer’s home country. Also, the value of the portfolio may be influenced by currency exchange control regulations. The currencies of emerging market countries may experience significant declines against the U.S. dollar, and devaluation may occur subsequent to investments in these currencies by the portfolio.

Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the U.S. and are considered speculative and subject to heightened risks in addition to the general risks of investing in non-U.S. securities. Also, inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

Index Definitions:

MSCI China Index captures large and mid cap representation across China A shares, H shares, B shares, Red chips, P chips and foreign listings (e.g. ADRs).

The MSCI China A Index captures large and mid-cap representation across China securities listed on the Shanghai and Shenzhen exchanges. The index covers only those securities that are accessible through “Stock Connect”. The index is designed for international investors and is calculated using China A Stock Connect listings based on the offshore RMB exchange rate (CNH).

The Dow Jones China Offshore 50 Index measures the stock performance of companies whose primary operations are in mainland China but whose stocks trade on the exchanges of Hong Kong and the U.S.

Standard & Poor’s (S&P) 500 Index measures the performance of 500 large cap stocks, which together represent about 80% of the total US equities market.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2021 RiverFront Investment Group. All Rights Reserved. ID 1745174