So, here is the big question: Why aren’t more long-term investors financially independent?

The short answer is… because of the substantial losses that comes from the inevitable Bear markets. In other words, traditional investing cannot adapt to difficult market environments. As a result, high volatility and bear markets eliminate years of personal savings and accumulated gains forever.

Making money means nothing unless you can keep it. Markets can be cruel. They can give, and give some more, and then take it away. These periods that wipe out years of savings and growth have one thing in common… They occur in market indexes, and portfolios, that have a high concentration in an asset class that has experienced a major advance.

It appears that we may be entering one of those periods that rob many Americans of their future financial independence. Today, the major market indexes, like the S&P 500, have the highest concentration of risk since 2000. Implementing “efficient diversification” has never been more important than it is right now.

Now we will discuss the state of the markets and why portfolios must adapt their diversification to avoid the potential risks ahead.

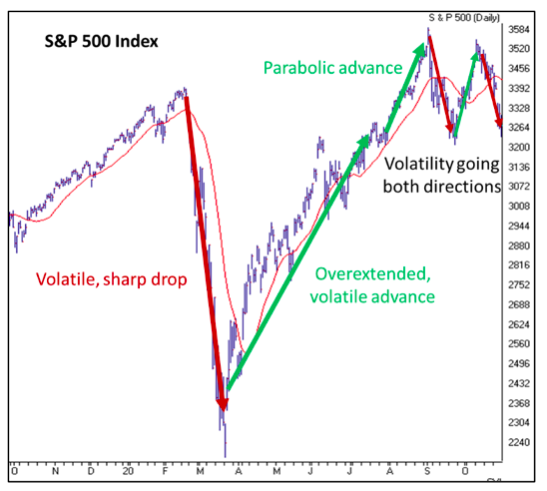

You have probably heard it before—markets do not like uncertainty, but keep in mind that the future is almost always uncertain. The volatility that has been experienced the last few weeks stems from a volatile market environment that began in late March.

Source: AIQ Trading Expert Pro

We are sure the news will be filled with nothing but the election over the coming days, so let’s turn our attention to something that we have been discussing for a while and something that others are just starting to pick up on: Technology and its impact on the markets.

Technology’s impact on the Market

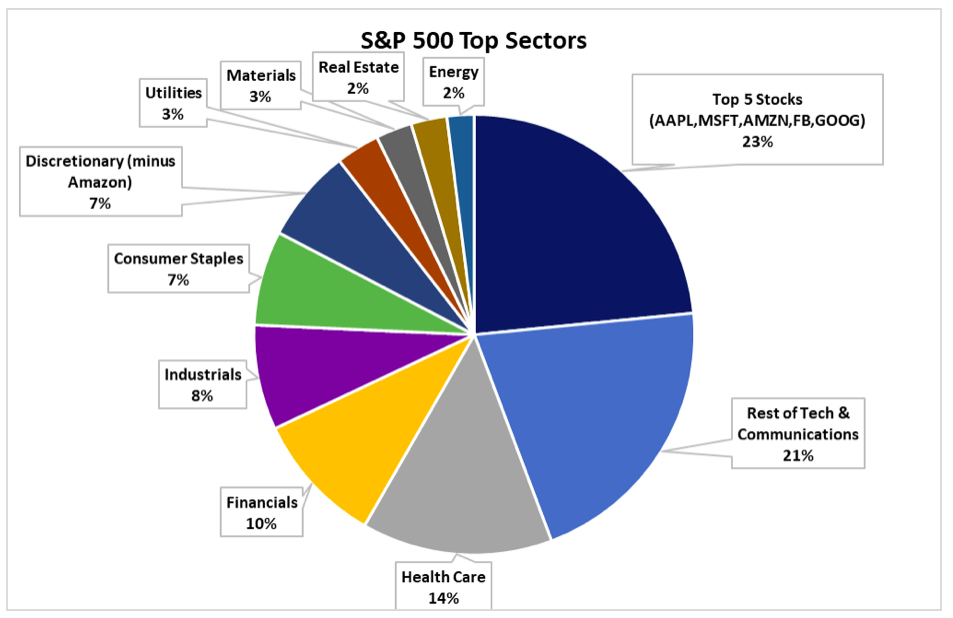

The S&P 500, which represents the 500 largest US stocks and is generally used to measure the health of the US stock market, is a market capitalization weighted index. This means that the larger a stock is, the more of an impact it has on the movement of the S&P 500.

For instance, did you know that the 5 largest stocks in the S&P 500 (Apple, Microsoft, Amazon, Facebook, and Google) make up 23% of the index’s movement. In other words, 5 technology-related stocks have the same impact on the market as the Consumer Staples, Utilities, Energy, Industrials, Basic Materials, and Real Estate sectors COMBINED. That is 5 technology-related stocks having the same impact as 210 other stocks. So, as technology goes, the markets go.

From the chart above, you can see that the top 5 largest S&P 500 stocks would make up the largest sector and are all technology-related. The next largest sector would be the rest of Technology & Communications. Altogether, technology-related stocks make up north of 40% of the S&P 500.

So, with all the drops and advances that have occurred in the markets this year, the question becomes “how healthy is the stock market?” We have talked about how Technology-related stocks have substantially outpaced virtually all other market segments. Since Technology is such a large component of the S&P 500, it has carried the broad markets higher.

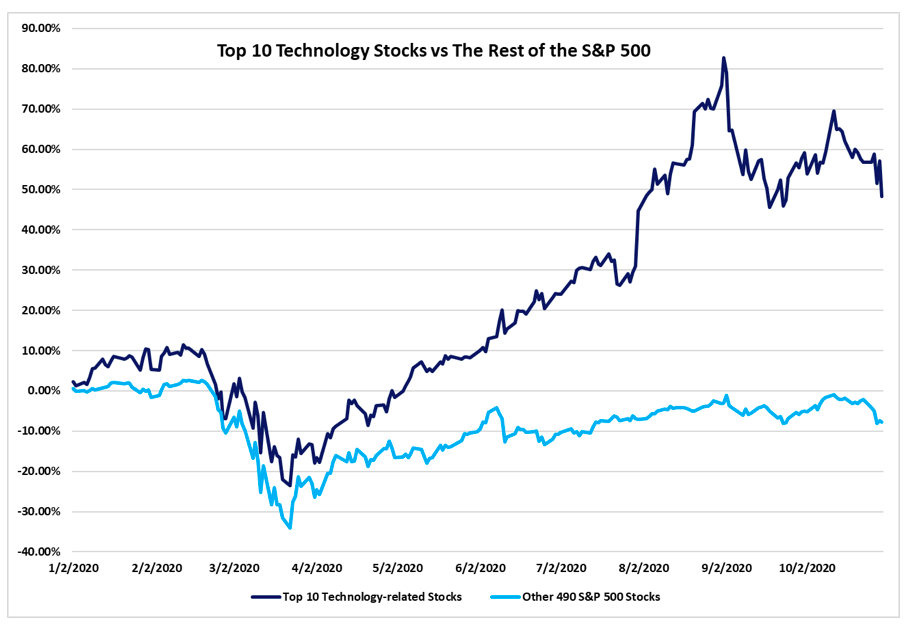

To support this claim, our team at Canterbury ran a study that compares the largest technology stocks and their performance versus the rest of the market. To do this, two indexes were created:

- The 10 largest technology-related stocks. The parameters for “technology-related” were the 10 largest stocks with at least a .600 (semi-strong/strong correlation) to the Nasdaq 100 index over the last 6 months. The Nasdaq is broadly considered a technology-based index. This index was also cap-weighted, meaning Apple is the largest stock, Microsoft is second, Amazon is third, etc. The components were: Apple, Microsoft, Amazon, Facebook, Google, Nvidia, PayPal, Adobe, Salesforce, and Netflix.

- The second index contained every other S&P 500 stock and was also market capitalization weighted. In this case, the index contained 490 stocks, of which the largest were Berkshire, Johnson & Johnson, Proctor & Gamble, Visa, JP Morgan, United Healthcare, and Home Depot.

Source: CIM. Amibroker was used to create these indexes

Year-to-date the top Technology-related stocks are up +48% while the index of the other 490 stocks is down -8%. The top 10 tech stocks make up 27% of the S&P 500. In fact, since the beginning of 2018, the 10 largest Tech stocks are up +152%, while a value index (which represents S&P 500 stocks that are not technology-related) is down -3.3%. Throughout that time, both have experienced extremely high volatility.

To lead into our next point, notice how the volatility, or erratic movements in the top technology-related stocks has substantially increased over the last 2 months. Heading into September, it almost felt like no matter what technology stock was invested in, it was going to make money, and many inexperienced day-trading Robinhood investors probably felt like geniuses. After a parabolic rise, those top tech stocks have fallen -20% off their peaks. The other 490 S&P 500 stocks have also been volatile, but much less relative to the tech counterparts.

Tech Bubble of 2000

No two markets are exactly the same, but the investor psychology that impacts the market’s behavior can be very similar. The market movements we are seeing today have similar characteristics to a market we saw back in 2000. Back in 2000, technology-related stocks also made up 40% of the S&P 500. Technology stocks also performed extremely well, substantially outpacing every other sector by a wide margin.

S&P 500 components heading into the Tech Crash:

Source: Historical S&P Sector Weightings, SeekingAlpha

In the chart below, which occurs in the 10 months leading up to the market’s peak in March 2000, prior to the Tech crash, you can see that Technology was also substantially outpacing the broad market (S&P 500) and Value stocks (which are mostly non-tech related)

Source: AIQ Trading Expert Pro

What followed this chart was Technology stocks crashing by -80% over the next two years, and the overall market falling by nearly -50%. It took until 2007 for the market to get back to breakeven before heading into the financial crisis, which yet again took the market all the way back to prior lows. All told, it took over 13 years for the market to get back to the same level as it was in 2000.

Are we seeing another bubble in technology? Absolutely. Seven years prior to 2000, technology went up 900%. In the last 7 years, technology has gone up 800%. As to when that bubble will pop, time will certainly tell, but what we know right now is that technology is showing many of the same dangerous characteristics as it was back in 2000.

Portfolio Management

When it comes to long-term investing, we all have the same goal. We want our portfolios to make us financially independent.

The truth is that most long-term investors will not accumulate an investment portfolio big enough to meet their life-long needs. This is true even though they may have saved enough money and have been invested for a long time.

It is important to understand the benefits that efficient diversification can have on the risk from difficult markets. The subject of “diversification,” was first explored by Nobel Prize winner, Harry Markowitz. Dr. Markowitz wrote a paper titled “Portfolio Selection” (1952) and a book, Portfolio Selection: Efficient Diversification (1959). His work discussed the impact that diversification can have on both, reducing risk and increasing long-term return.

Dr Markowitz’s point was that “diversification” alone was not enough to have a meaningful impact on reducing market risk.

The following is a quote from Dr Markowitz:

“To reduce risk it is necessary to avoid a portfolio whose securities are all highly correlated with each other. One hundred securities whose returns rise and fall in near unison afford little protection than the uncertain return of a single security.”

A “good portfolio” is more than just a list of stocks and bonds. The portfolio should be diversified in a way to protect against “a wide range of contingencies.”

In other words, a 15-stock portfolio, that contains 7 technology stocks may have periods of very high returns. On the other hand, a concentrated portfolio will eventually suffer a substantial loss when most are impacted by the same negative event.

Bottom Line

Market indexes were not designed to be efficient portfolios; they were mainly created to measure market capitalization. In some cases, market indexes can be well-balanced among its sectors and be a reasonably efficient portfolio. There are other times when one sector will take over, making an index highly inefficient, which ultimately results in a substantial decline. As of today, the market’s extreme overweighting in technology makes it highly vulnerable. When the tech bubble pops, the market will suffer substantially.

Similarly, many static or strategic portfolios will also suffer and experience substantial declines because of their inability to adapt—they will reflect what the broad markets experience.

A bear market occurs over a long time and takes even more time to recover, which is not to be confused with what we have seen this year. When a bear market comes, it will take time to form, and more time to recover. Portfolios which are unable to adapt will then take years and years just to get back to a point of breakeven, leaving many investors short of their goal of financial independence.

This is why portfolios need to be able to adapt. Markets will always encounter difficult periods. Adaptive portfolio management was designed just for that reason. When, not if, technology bursts and causes increased volatility in the markets, Adaptive Portfolio Management has a system mitigate risk in the portfolio.

Adaptive portfolio management is not about substantially overweighting the hottest areas of the market, but instead creating a diversified, efficient portfolio of securities that are showing low correlated, low risk characteristics. An efficient portfolio will not have 40%+ invested in technology. As each security’s characteristics begin to change, the portfolio will continue to adjust to maintain an efficient portfolio through any market environment- bull or bear.