Benchmark Review & Monthly Recap, July 2023 – Clark Capital Management Group

Summer Rally Continued in July; Market Breadth Improved

HIGHLIGHTS:

- Large-cap growth stocks have dominated in 2023, but market breadth has improved in recent months as value and smaller-cap companies have rallied.

- The VIX Index, a measure of stock market volatility, remained subdued in July. After ending June at 13.59, the VIX closed July at 13.63. Subdued volatility and sentiment getting overly bullish could be a near-term headwind for the market.

- Bond yields remained elevated in July. The 10-year U.S. Treasury yield ended July at 3.97% compared to June’s close of 3.81%.

- Yields moving higher was a headwind for bonds as fixed income results were mixed in July.

- The “soft landing” narrative seems to be gaining some steam as economic growth surprised to the upside in the first half of 2023, the job market remained strong, and inflation continued to move lower. However, there are still parts of the economy that are showing some weakness (like manufacturing), and we anticipate a slowdown in the pace of growth moving later into 2023.

EQUITY MARKETS

Equities remained the name of the game in July as stocks rallied across the board. Large-cap Technology companies still dominated year to date, but small and mid-cap companies enjoyed better relative results for the second-straight month. Both value and growth rallied with value enjoying a modest edge in July. International stocks gained with emerging markets among the best equity categories for the month. See Table 1 for equity results for July and year to date.

Table 1

| Index | July 2023 | YTD |

|---|---|---|

| S&P 500 | 3.21% | 20.65% |

| S&P 500 Equal Weight | 3.46% | 10.73% |

| DJIA | 3.44% | 8.55% |

| Russell 3000 | 3.58% | 20.33% |

| NASDAQ Comp. | 4.08% | 37.71% |

| Russell 2000 | 6.12% | 14.70% |

| MSCI ACWI ex U.S. | 4.07% | 13.92% |

| MSCI Emerging Mkts Net | 6.23% | 11.42% |

The broad rally in stocks continued in July, which helped the average stock make additional progress after a weak first several months of 2023. Recall, the equal-weighted S&P 500 Index (which can be thought of as representing what the average stock is doing) was negative through the first five months of the year. That reversed in June and with further gains in July, this measure of stocks is now up double digits (10.73%) year to date.

The same holds true for small-caps, which had been negative through May, but have rallied sharply. Gains in the last two months have pushed this index up by 14.70% year to date. The mega-cap Technology companies continued to enjoy a strong recovery from their 2022 declines and that can clearly be seen in the results of the NASDAQ.

Interestingly, although small-caps, mid-caps, and value stocks have enjoyed recent leadership, it is not as if large-cap growth companies have done poorly. Large-cap growth stocks have also continued to make more gains, but the broader market seems to be catching up with what had been very narrow leadership.

Broad international equities had another solid month in July, while MSCI Emerging Markets had a sharp rebound up 6.23% for the month. International stocks have enjoyed a strong 2023, surpassing the results of the S&P 500 equal-weighted index. U.S. large-cap growth stocks have lapped most other equity categories and remain the clear leader so far in 2023.

Style mattered more in the small-cap universe in July. The Russell 2000 Value Index (a small-cap measure) gained 7.55% in July, while the Russell 2000 Growth Index was up 4.68%. Results for those indices year to date are 10.24% and 18.86%, respectively. July was a better month for small-caps overall, and value in particular, but the year-to-date period has so far belonged to growth and large-cap stocks

Fixed Income

Bond results were rather mixed in July as rates moved higher during the month. The 10-year U.S. Treasury yield has been trending upwards since the late spring (when it got to 3.3% in April) and closed July at 3.97%. This move higher has put bond returns under pressure in recent months, which continued in July with mixed results. As spreads narrowed, corporate bonds, particularly high yield bonds, made gains during the month. U.S. Treasuries were mixed, but longer dated Treasuries struggled as rates rose. See Table 2 for fixed income index returns for July and year to date.

Table 2

| Index | July 2023 | YTD |

|---|---|---|

| Bloomberg U.S. Agg | -0.07% | 2.02% |

| Bloomberg U.S. Credit | 0.31% | 3.45% |

| Bloomberg U.S. High Yld | 1.38% | 6.83% |

| Bloomberg Muni | 0.40% | 3.08% |

| Bloomberg 30-year U.S. TSY | -2.50% | 0.90% |

| Bloomberg U.S. TSY | -0.35% | 1.23% |

We expect the 10-year U.S. Treasury yield to move lower as we go through 2023, but we also anticipate volatility along the way. We acknowledge that the recent move has been higher in yields, but the 10-year U.S. Treasury yield has stayed below the high from October 2022 of 4.25%. Enjoying solid gains for the month, high yield bonds have been the clear winner so far in 2023, which is not that surprising on the heels of such solid stock market gains.

Muni bonds also had a solid July, and year to date results are over 3% for this index; however, the Bloomberg Municipal 5-year Index has gained less than half of that and is only up 1.51% year to date. Shorter maturity U.S. Treasuries made some gains for the month, but longer dated bonds struggled. Bonds have enjoyed a better environment in 2023 compared to a historically challenging period for fixed income in 2022, but the last two months have been more mixed for bonds as stocks have rallied.

We maintain our long-standing position of favoring credit versus pure rate exposure in this interest rate environment. We also believe the role bonds play in a portfolio, to provide stable cash flows and to help offset the volatility of stocks in the long run, has not changed. We also believe that bond yields are attractive, with some of the highest yields we have seen in the last 15 years

Economic Data and Outlook

The first reading of second quarter 2023 GDP growth was reported at a much stronger pace than expected. This advanced reading came in at a 2.4% annualized growth rate, when expectations were calling for 1.8%. (This reading will be revised two times in the months ahead.) Personal consumption was one area that was better than expected, which helped push GDP higher. We still expect economic growth to slow down later in the year and believe that the risk of a mild recession is about as likely as a soft landing.

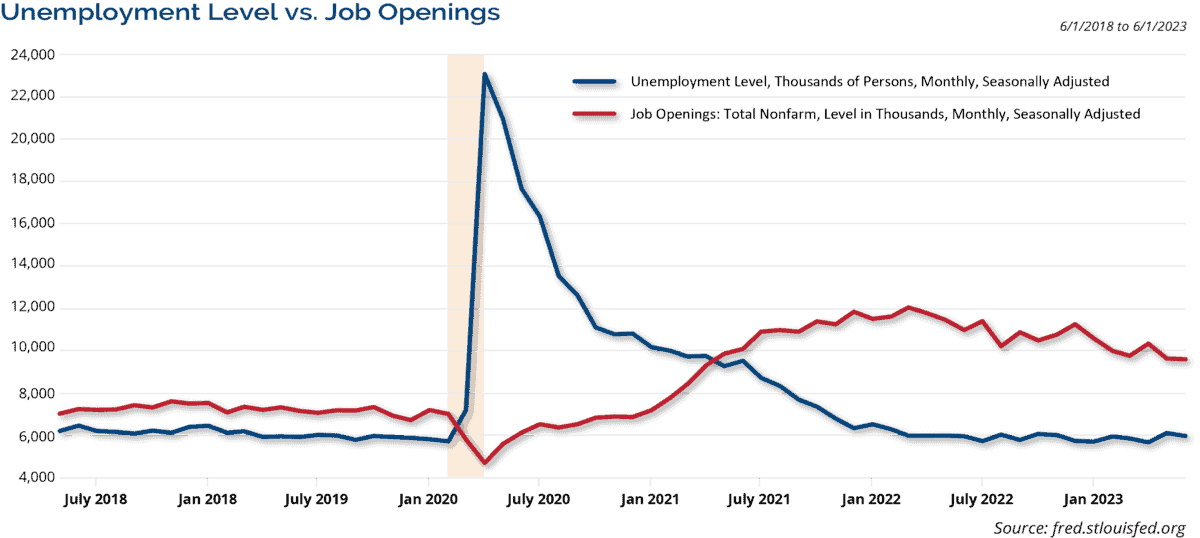

The unemployment rate fell to 3.6% in June as expected from 3.7%, despite non-farm payroll additions being modestly disappointing at 209,000 compared to expectations of 230,000. Job openings remain plentiful, but they have moved lower in recent months. Chart 1 shows that there are still millions more job openings than unemployed people.

Chart 1

The mismatch between job seekers and job openings creates its own issues, but labor market strength seems likely to continue based on this disparity. Businesses might be slowing their hiring activity with concerns about potential weaker economic conditions as job openings have come down. However, the job market remains strong, and it seems unlikely that the economy would slow too drastically with the current job market and consumer strength.

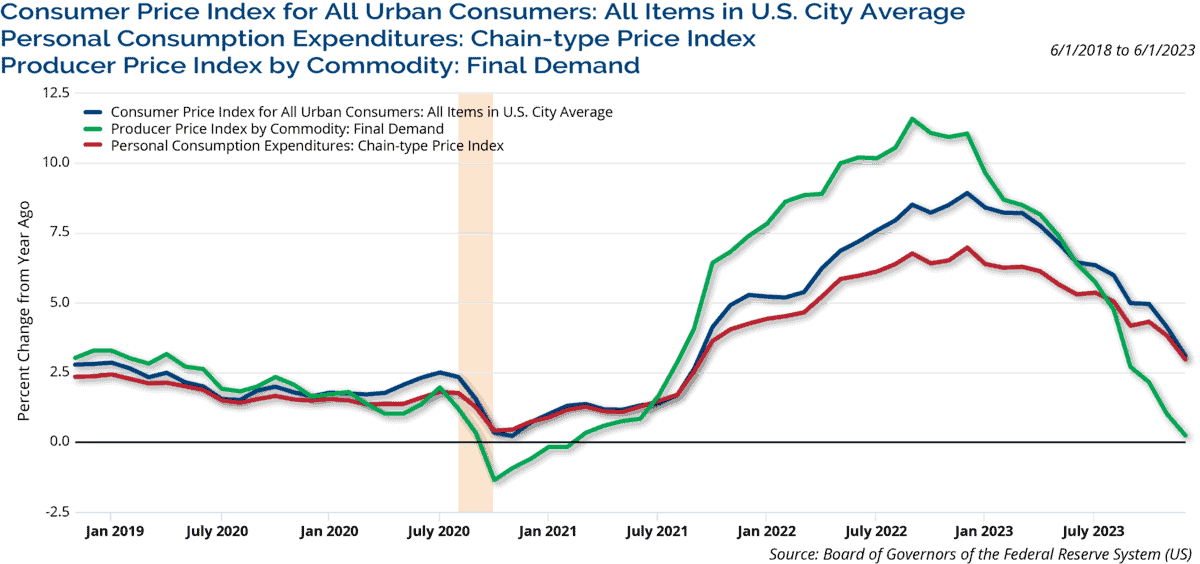

Wages climbed by 4.4% on an annual basis in June, which was just above expectations of 4.2%, but in line with May’s revised number. Too much strength in job market data could be viewed as inflationary by Fed officials and extend this period of restrictive monetary policy. At this point, the Fed’s rate hikes have not had a weakening effect on the job market, but inflation has been moving lower and those readings continued to improve in June. The headline Consumer Price Index (CPI) for June dropped to a 3.0% annual increase, which was better than expectations of 3.1% and an improvement from the prior month’s level of 4.0%. The core CPI was 4.8%, which improved from the prior month of 5.3% and expectations of 5.0%.

The headline Producer Price Index (PPI) continued to fall dramatically and declined to a mere 0.1% annual increase, which was better than expectations of 0.4% and the prior month’s mark of 0.9%. The core PPI was 2.4%, which was also lower than expectations and a decline from May. The Producer Price Index is generally seen as a leading indicator for inflation since these costs occur during the production part of the cycle before products are sold to consumers. Ongoing declines in this index bode well for continued improvements on the inflation front. The Personal Consumption Expenditures (PCE) Index showed a 3.0% annual gain in June from the 3.8% level in May, which was in line with expectations. The Fed’s preferred measure of inflation, the core PCE reading, showed a 4.1% annual rise, which was modestly better than expectations of 4.2% and an improvement from May’s 4.6%. This, however, is still above the Fed’s long-run target of 2%. Overall, it seems clear that the trajectory for inflation is lower and we expect inflation to continue this trend through 2023. Chart 2 shows the percent change from a year ago for these headline inflation readings and this trend lower.

Chart 2

The “soft landing” scenario has been gaining momentum as rate hikes so far have caused limited damage to the job market, GDP strength has been better than expected, and inflation continues to trend lower. However, the aggressive 75 basis point rate hikes from last summer and fall are now just hitting their one-year anniversary and are still likely working their way through the economic system. We think this could be a headwind for the economy later in the year.

Housing data was largely weaker than expected in June. Interest rates have remained elevated in recent months, so some softening in the housing market is not surprising. Building permits, considered a leading indicator for housing, were at an annualized pace of 1.440 million in June. This lagged expectations of 1.5 million and May’s level of 1.496 million. Housing starts fell to an annualized pace of 1.434 million, short of expectations of 1.48 million and well off the revised lower reading of 1.559 million for May.

Existing home sales and new home sales both missed expectations and were lower than May’s levels. Home prices fell in May based on the S&P CoreLogic 20-City Index, but the decline was more modest than expected. Mortgage rates, which have climbed significantly over the last year or so, seem to be flattening out, albeit at an elevated level, which could be slowing some activity. Chart 3 shows the impact that higher mortgage rates have had on building permits. This chart shows an inverse relationship between mortgage costs and people filing permits to build new homes. One of the challenges in the housing market is that people are reluctant to move because they would likely be swapping from a lower interest rate mortgage to a much higher one. That factor seems to be slowing housing activity.

Chart 3

The ISM Manufacturing Index disappointed and showed contraction for the 8th consecutive month in June with a reading of 46.0. The June reading was below expectations of 47.1 and the prior month mark of 46.9. (The July number was below expectations and not much better than June at 46.4 to mark the 9th straight month of declines.) The ISM Non-Manufacturing Index, which covers the much larger service industries in the U.S. economy, recovered from the prior month’s decline. This reading came in at 53.9 in June compared to expectations of 51.2 and the prior month level of 50.3. The service index has slowed in recent months, but it continues to be above 50 and it moved clearly above that mark in June. Recall, the dividing line between expansion and contraction for the ISM indices is 50.

Retail sales (ex. auto and gas) rose by 0.3% as expected in June, but this was shy of the 0.5% growth in May. Buoyed in part by ongoing strength in the job market and further gains in stocks, the preliminary University of Michigan Sentiment reading for July rose to 72.6 compared to expectations of 65.5 and the prior reading of 64.4. The Conference Board’s Leading Index (LEI) continued to decline and fell by -0.7% in June, which was modestly worse than the expected -0.6% decline. For over a year, the leading economic index has been flashing a warning sign of pending economic weakness which has yet to materialize.

After the Fed “skipped” raising rates in June, it once again increased policy rates by 25 basis points in July. We now enter a period of elevated uncertainty. Will the Fed raise rates later in the year or end this rate hike cycle?

Although economic growth picked up in the second half of 2022 and continued through the first half of 2023, we expect growth to slow later in the year. We believe the odds of a mild recession are about 50/50. The job market has remained resilient, which leads us to the conclusion that even if a recession occurs, it would be modest in our opinion.

However, the recent decline in job openings might be an initial sign of more caution by employers in hiring. As always, we believe it is imperative for investors to stay focused on their long-term goals and not let short-term swings in the market derail them from their longer-term objectives.

Investment Implications

Clark Capital’s Top-Down, Quantitative Strategies

Our tactical portfolios remain fully invested in risk-on vehicles and are allocated to high yield and global equity; in addition, they are overweight growth versus value. Credit has performed well even as Treasuries have declined. The benign credit environment has been supportive of risk assets. However, seasonality is now likely to provide a modest headwind as we enter the weakest seasonal period of the year.

Clark Capital’s Bottom-Up, Fundamental Strategies

The S&P 500 Index’s second quarter earnings projections were cut significantly ahead of the reporting season providing support for the market. So far, 83% of U.S. companies reporting have beaten earnings estimates. On a sector basis, much of the earnings strength has been in Consumer Discretionary and Technology, which have outperformed this year.

During July, municipal bonds outperformed most fixed income indices, including the U.S. Aggregate Index and the U.S. Treasury Index. Looking ahead, August is typically seasonally positive for municipal bonds with reinvestment from July’s called and matured bonds normally providing a strong demand tailwind.

ECONOMIC DATA

| Event | Period | Estimate | Actual | Prior | Revised |

|---|---|---|---|---|---|

| ISM Manufacturing | June | 47.1 | 46 | 46.9 | — |

| ISM Services Index | June | 51.2 | 53.9 | 50.3 | — |

| Change in Nonfarm Payrolls | June | 230k | 209k | 339k | 306k |

| Unemployment Rate | June | 3.60% | 3.60% | 3.70% | — |

| Average Hourly Earnings YoY | June | 4.20% | 4.40% | 4.30% | 4.40% |

| JOLTS Job Openings | June | 9600k | 9582k | 9824k | 9616k |

| PPI Final Demand MoM | June | 0.20% | 0.10% | -0.30% | -0.40% |

| PPI Final Demand YoY | June | 0.40% | 0.10% | 1.10% | 0.90% |

| PPI Ex Food and Energy MoM | June | 0.20% | 0.10% | 0.20% | 0.10% |

| PPI Ex Food and Energy YoY | June | 2.60% | 2.40% | 2.80% | 2.60% |

| CPI MoM | June | 0.30% | 0.20% | 0.10% | — |

| CPI YoY | June | 3.10% | 3.00% | 4.00% | — |

| CPI Ex Food and Energy MoM | June | 0.30% | 0.20% | 0.40% | — |

| CPI Ex Food and Energy YoY | June | 5.00% | 4.80% | 5.30% | — |

| Retail Sales Ex Auto and Gas | June | 0.30% | 0.30% | 0.40% | 0.50% |

| Industrial Production MoM | June | 0.00% | -0.50% | -0.20% | -0.50% |

| Building Permits | June | 1500k | 1440k | 1491k | 1496k |

| Housing Starts | June | 1480k | 1434k | 1631k | 1559k |

| New Home Sales | June | 725k | 697k | 763k | 715k |

| Existing Home Sales | June | 4.20m | 4.16m | 4.30m | — |

| Leading Index | June | -0.60% | -0.70% | -0.70% | -0.60% |

| Durable Goods Orders | June P | 1.30% | 4.70% | 1.80% | 2.00% |

| GDP Annualized QoQ | 2Q A | 1.80% | 2.40% | 2.00% | — |

| U. of Mich. Sentiment | July P | 65.5 | 72.6 | 64.4 | — |

| Personal Income | June | 0.50% | 0.30% | 0.40% | 0.50% |

| Personal Spending | June | 0.40% | 0.50% | 0.10% | 0.20% |

| S&P CoreLogic CS 20-City YoY NSA | May | -2.35% | -1.70% | -1.70% | -1.69% |

Source: Bloomberg

Download Market Recap

Past performance is not indicative of future results. The opinions referenced are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Material presented has been derived from sources considered to be reliable and has not been independently verified by us or our personnel. Nothing herein should be construed as a solicitation, recommendation or an offer to buy, sell or hold any securities, other investments or to adopt any investment strategy or strategies. Investors must make their own decisions based on their specific investment objectives and financial circumstances. Investing involves risk, including loss of principal.

Clark Capital Management Group is an investment adviser registered with the U.S. Securities and Exchange Commission. Registration does not imply a certain level of skill or training. More information about Clark Capital Management Group’s advisory services can be found in its Form ADV which is available upon request.

Fixed income securities are subject to certain risks including, but not limited to: interest rate (changes in interest rates may cause a decline in market value or an investment), credit, prepayment, call (some bonds allow the issuer to call a bond for redemption before it matures), and extension (principal repayments may not occur as quickly as anticipated, causing the expected maturity of a security to increase).

Clark Capital utilizes a proprietary investment model to assist with the construction of the strategy and to assist with making investment decisions. Investments selected using this process may perform differently than expected as a result of the factors used in the model, the weight placed on each factor, and changes from the factors’ historical trends. There is no guarantee that Clark Capital’s use of a model will result in effective investment decisions.

Non-investment-grade debt securities (high-yield/junk bonds) may be subject to greater market fluctuations, risk of default or loss of income and principal than higher-rated securities.

Foreign securities are more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards and political and economic risks. These risks are enhanced in emerging market countries.

The value of investments, and the income from them, can go down as well as up and you may get back less than the amount invested.

Equity securities are subject to price fluctuation and possible loss of principal. Stock markets tend to move in cycles, with periods of rising prices and periods of falling prices. Certain investment strategies tend to increase the total risk of an investment (relative to the broader market). Strategies that concentrate their investments in limited sectors are more vulnerable to adverse market, economic, regulatory, political, or other developments affecting those sectors.

JOLTS is a monthly report by the Bureau of Labor Statistics (BLS) of the U.S. Department of Labor counting job vacancies and separations, including the number of workers voluntarily quitting employment.

The Producer Price Index (PPI) program measures the average change over time in the selling prices received by domestic producers for their output. The prices included in the PPI are from the first commercial transaction for many products and some services.

References to market or composite indices, benchmarks or other measures of relative market performance over a specified period of time (each, an “index”) are provided for your information only. Reference to an index does not imply that the portfolio will achieve returns, volatility or other results similar to that index. The composition of the index may not reflect the manner in which a portfolio is constructed in relation to expected or achieved returns, portfolio guidelines, restrictions, sectors, correlations, concentrations, volatility or tracking error targets, all of which are subject to change. Investors cannot invest directly in an index.

The Bloomberg Barclays U.S. Municipal Index covers the USD-denominated long-term tax exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds and prerefunded bonds.

The Bloomberg US Treasury Index measures US dollar-denominated, fixed-rate, nominal debt issued by the US Treasury. Treasury bills are excluded by the maturity constraint, but are part of a separate Short Treasury Index.

The Dow Jones Industrial Average indicates the value of 30 large, publicly owned companies based in the United States.

The NASDAQ Composite is a stock market index of the common stocks and similar securities listed on the NASDAQ stock market.

The S&P 500 measures the performance of the 500 leading companies in leading industries of the U.S. economy, capturing 80% of U.S. equities.

The S&P 500® Equal Weight Index (EWI) is the equal-weight version of the widely-used S&P 500. The index includes the same constituents as the capitalization weighted S&P 500, but each company in the S&P 500 EWI is allocated a fixed weight – or 0.2% of the index total at each quarterly rebalance.

The University of Michigan Consumer Sentiment Index rates the relative level of current and future economic conditions. There are two versions of this data released two weeks apart, preliminary and revised. The preliminary data tends to have a greater impact. The reading is compiled from a survey of around 500 consumers.

The Russell 1000 Growth Index measures the performance of the large-cap growth segment of the U.S. equity universe. It includes those Russell 1000 Index companies with higher price-to-book ratios and higher forecasted growth values.

The Russell 1000 Value Index measures the performance of the large-cap value segment of the U.S. equity universe. It includes those Russell 1000 Index companies with lower price-to-book ratios and lower forecasted growth values.

The Russell 2000 Index is a small-cap stock market index that represents the bottom 2,000 stocks in the Russell 3000.

The Russell 3000 Index measures the performance of the 3,000 largest U.S. companies based on total market capitalization, which represents approximately 98% of the investable U.S. equity market.

The 10 Year Treasury Rate is the yield received for investing in a US government issued treasury security that has a maturity of 10 year. The 10 year treasury yield is included on the longer end of the yield curve. Many analysts will use the 10 year yield as the “risk free” rate when valuing the markets or an individual security.

The Bloomberg Barclays U.S. Corporate High-Yield Index covers the U.S. dollar-denominated, non-investment grade, fixed-rate, taxable corporate bond market. Securities are classified as high-yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below.

The Bloomberg Barclays U.S. Credit Index measures the investment grade, U.S. dollar denominated, fixed-rate taxable corporate and government related bond markets.

The Bloomberg Aggregate Bond Index or “the Agg” is a broad-based fixed-income index used by bond traders and the managers of mutual funds and exchange-traded funds (ETFs) as a benchmark to measure their relative performance.

The 30-Year Treasury is a U.S. Treasury debt obligation that has a maturity of 30 years. The 30-year Treasury used to be the bellwether U.S. bond but now most consider the 10-year Treasury to be the benchmark.

The ISM Non-Manufacturing Index is an index based on surveys of more than 400 non-manufacturing firms’ purchasing and supply executives, within 60 sectors across the nation, by the Institute of Supply Management (ISM). The ISM Non-Manufacturing Index tracks economic data, like the ISM Non-Manufacturing Business Activity Index. A composite diffusion index is created based on the data from these surveys, that monitors economic conditions of the nation.

ISM Manufacturing Index measures manufacturing activity based on a monthly survey, conducted by Institute for Supply Management (ISM), of purchasing managers at more than 300 manufacturing firms.

The MSCI Emerging Markets Index captures large and mid cap representation across 27 Emerging Markets (EM) countries.

The MSCI ACWI ex USA Index captures large and mid cap representation across 22 of 23 Developed Markets (DM) countries (excluding the US) and 27 Emerging Markets (EM) countries*. With 2,359 constituents, the index covers approximately 85% of the global equity opportunity set outside the US

The S&P CoreLogic Case-Shiller 20-City Composite Home Price NSA Index seeks to measures the value of residential real estate in 20 major U.S. metropolitan areas. The U.S. Treasury index is based on the recent auctions of U.S. Treasury bills. Occasionally it is based on the U.S. Treasury’s daily yield curve.

The Consumer Price Index (CPI) measures the change in prices paid by consumers for goods and services. The CPI reflects spending patterns for each of two population groups: all urban consumers and urban wage earners and clerical workers.

In the United States, the Core Personal Consumption Expenditure Price (CPE) Index provides a measure of the prices paid by people for domestic purchases of goods and services, excluding the prices of food and energy.

The VIX Index is a calculation designed to produce a measure of constant, 30-day expected volatility of the U.S. stock market, derived from real-time, mid-quote prices of S&P 500® Index (SPX℠) call and put options. On a global basis, it is one of the most recognized measures of volatility — widely reported by financial media and closely followed by a variety of market participants as a daily market indicator.

The Conference Board’s Leading Indexes are the key elements in an analytic system designed to signal peaks and troughs in the business cycle. The leading, coincident, and lagging economic indexes are essentially composite averages of several individual leading, coincident, or lagging indicators. They are constructed to summarize and reveal common turning point patterns in economic data in a clearer and more convincing manner than any individual component – primarily because they smooth out some of the volatility of individual components.

Gross domestic product (GDP) is the standard measure of the value added created through the production of goods and services in a country during a certain period.

Index returns include the reinvestment of income and dividends. The returns for these unmanaged indexes do not include any transaction costs, management fees or other costs. It is not possible to make an investment directly in any index.

CCM-993