By BCM Investment Team

Smart Portfolios For Challenging Times

Overview

What started as a summer of optimism in markets ended with a fall of fear. Tough talk[1] from the Federal Reserve and August’s inflation print brought equity and fixed income markets broadly towards new lows to close out the quarter.

This remains an extraordinarily challenging and unpredictable investment environment due to exogenous events (Covid/China supply-chain bottlenecks, Ukraine War/Europe Energy crisis) and the unprecedented government fiscal and interest-rate interventions in the economy.

The probabilistic machine learning models that are the foundation of the Decathlon system suggest that equities are “oversold” and offer favorable risk-reward, likewise for bonds. Aside from our statistical and behavioral-based quantitative systems, there is plenty of qualitative evidence that investors are very fearful and already girded for substantial further market declines. We believe downturns are less likely to occur when investors are braced for them. Therefore, both quantitatively[2] and qualitatively, our assessment is that it’s a timely entry point, that the actual risk is less than the perceived risk, and that being somewhat contrarian will pay off.

Furthermore, after the 3% upward shift[3] in the yield curve this year and the worst drawdowns on record for fixed income and traditional balanced strategies, the forward returns of a 60/40 type portfolio are likely higher than they have been in many years. While the recent performance of balanced portfolios has been frustrating for all investors, we expect balanced strategies to provide attractive absolute returns in most market scenarios with less volatility and mental stress than recently experienced.

Our biggest concern going forward is ongoing mismanagement of interest rates by the Federal Reserve. The rapid interest rate increases this year has destroyed substantial wealth in every asset class world-wide that is publicly traded. Certainly, investors of every stripe have already experienced a “hard landing” that has significantly reduced their wealth and likely will reduce their near-term economic activity. Likewise, many industries, such as housing and semiconductor memory, are already reporting year-over-year declines in business activity of 20%.[4]

Damage in markets is widespread and worse than it appears on the surface, EAFE Equities are 20% below their pre-pandemic highs and US Small Cap companies are flat and now trade at a historically low forward P/E of just 10.8, an earnings yield of nearly 10%[5].

It’s our belief that history will not look favorably upon the current Federal Reserve and their management of the economy through all phases of the pandemic. The latest mistake is navigating by looking out the rear window, making decisions based on stale historical information, and not paying attention to the real-time deterioration and value destruction in full view due to the extreme rate hikes. The Federal Reserve members publicly proclaim that “monetary policy acts with long and variable lags”, yet they lack the patience to wait for the impact of their actions.

While ultimately the direction of the economy will determine the direction of the market, we believe it is extremely unlikely to occur in a straight line. We’ll continue to look for opportunities to tactically add value which may be of increased importance while neither general equity nor fixed income exposure has yet to pay off for investors.

A Deeper Dive

Inflation hasn’t cooled off fast enough

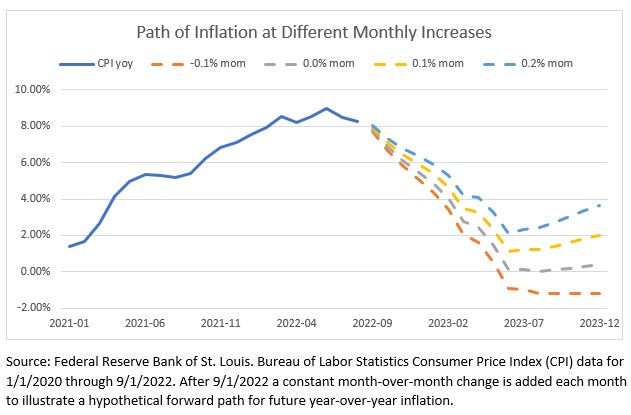

August’s Consumer Price Index (CPI) report took the market by surprise, showing +0.1% month-over-month rise in prices compared to expectations for a small decrease from Bloomberg’s economist survey. Perhaps more concerningly, core inflation, which excludes the benefit of lower oil prices, increased 0.6%–nearly double July’s increase and a 7.4% annualized rate. This has economists and market participants worried that core CPI will act as a floor for future inflation and necessitate a more severe recession than previously anticipated. Despite the doom and gloom over inflation, we maintain the opinion that the U.S. economy is past peak inflation. The level of prices remains relatively unchanged since June and many[6] market signals are pointing towards lower inflation. The illustration below shows the potential path of headline inflation if month over month changes remain relatively muted. Headline inflation will not fall quickly without a decrease in prices, but a continuation of recent trends will bring year over year inflation down to acceptable levels in due time.

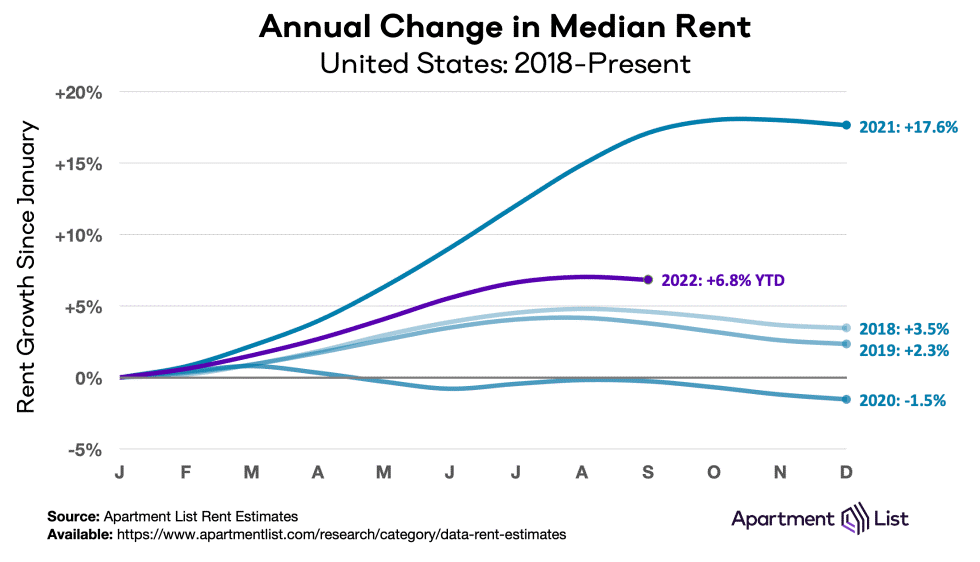

Realizing this path of lower inflation will be largely dependent on slower increases in the cost of shelter and labor. The cost of shelter, which rose 0.7% in August[1], is the largest component of core CPI and was responsible for more than half of August’s core CPI growth. This may be a lagging indicator of true inflation, as housing turnover is required for most housing prices to re-set and housing turnover is at historic lows. In addition, a number of sources show that both rent and home prices have stagnated.

While wages are an indirect input to CPI, wage growth is the key driver of the demand side of the inflation equation, and for most of the year wage growth has been extremely strong. In recent months that too has flattened as workers continue to re-join the labor force. This resulted in an increase in unemployment in August despite 315,000[1] more workers employed in the month. If wage growth and shelter costs continue to abate it’s hard to be overly concerned about another inflationary surge in the near-term.

Will the Federal Reserve “break the economy?”

“We have got to get inflation behind us. I wish there were a painless way to do that. There isn’t” – Jerome Powell.

With the benefit of hindsight, the Federal Reserve is behind the ball on inflation. Recent tough rhetoric is either an attempt to save face or an attempt to use the forward-looking nature of markets to pull forward tighter financial conditions before having to directly implement them[2].

We aren’t apt to read into the Fed’s psychology and determine if they are indeed bluffing or are determined to make good on their words, but with the federal funds rate at 3-3.25%, one-year treasury yields at 3.98%,[3] and an increasingly inverted yield curve it seems like the market does believe them. If markets are already discounting the Fed following through with their plan, any changes could be a positive surprise.

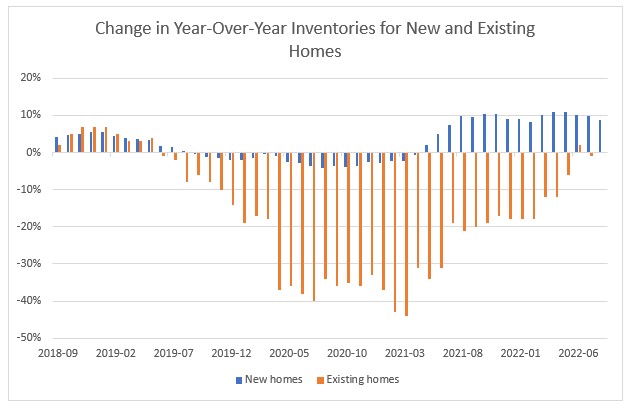

Fundamentally it is clear that higher interest rates are having the intended effects. Housing is the most interest rate sensitive sector in the economy and activity has dried up. With mortgages at 7%, compared to 3% earlier this year, the effective cost of the same priced house is roughly 60% higher. [4]Sellers currently appear unwilling to trade in their low fixed rate mortgages, while buyers have had affordability cramped. As a result, new homes built by homebuilders may be the only meaningful source of supply in the short-term.

Source: Bloomberg. National Association of Realtors. Data from 8/31/2017 to 8/31/2022.

Eventually it all comes down to earnings

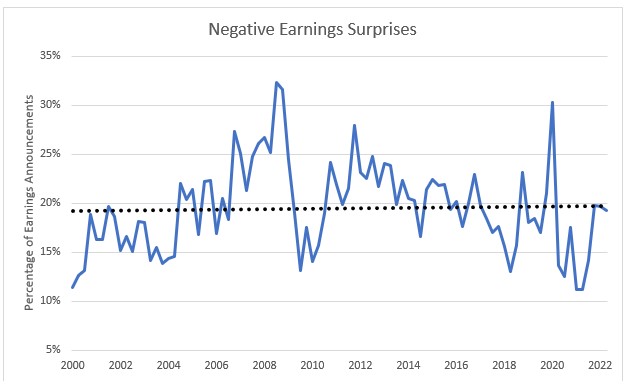

Eventually macroeconomic speculation trickles down to the market directly via corporate earnings. In the second quarter we saw some continued margin pressure, likely a result of both inflation and comparing against high volumes of 2021. However, the market was well calibrated for these earnings and negative surprises typically seen around recessions were mostly absent. These relatively strong earnings bolstered the markets at the beginning of the second quarter and will be an important catalyst looking ahead to the coming months.

Source: Bloomberg Earnings Surprise Index. Data from 3/1/2000 to 6/30/2022.

Last quarter we discussed the excess inventories at retailers that spooked the market—–this quarter it was Federal Express. It may be unwise to ignore one of the major carriers offering weak guidance and volumes when forecasting a potential recession, but the FedEx guidance could also represent a continued shift of consumer habits both from goods to services and digital to physical. Counter to FedEx’s weak guidance, commentary from banks and credit card companies thus far implies the consumer has yet to noticeably weaken.

Energy sector shows first signs of its customary volatility

Even this year’s lone bright spot in equity markets, Energy, has been under pressure due to fears of falling demand. The S&P 500 Energy sector fell over 25%[5] from highs in just over a month at the beginning of July despite ending the quarter as one of the best performing sectors. Spot oil prices are now lower than before Russia’s invasion of Ukraine, despite no material changes in policy towards Russian oil. One of the most humbling examples of how difficult investing can be is that by far the best performing sector since the pre-pandemic high is Energy and the worst is Communications[6], almost an exact inverse of the fundamental effects that occurred while we were locked down.

Concluding Thoughts

Preparing for the worst may make the “worst” unlikely

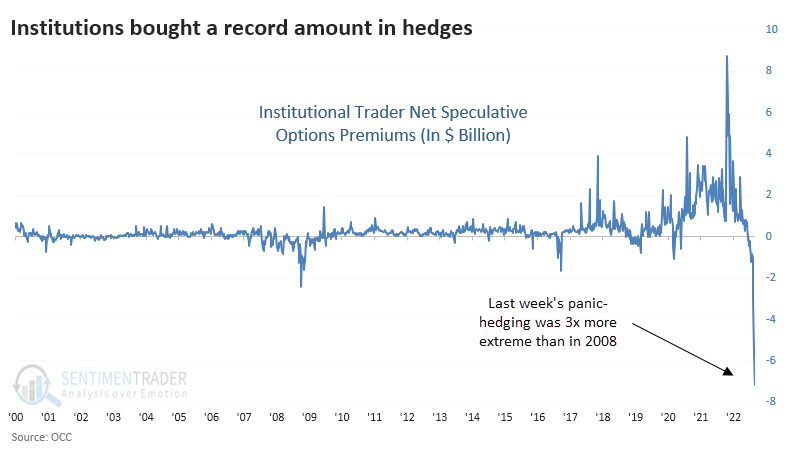

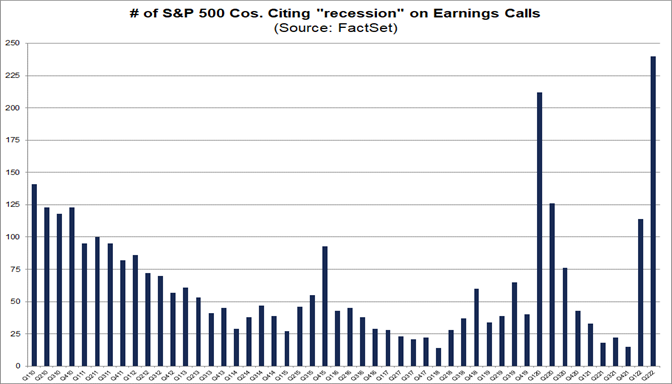

Investors appear to be positioned defensively and corporations have already prepared for the worst. Despite the damage that has already occurred, money market and bank deposit balances have never been higher in history[7], nor has demand for hedging via puts. Many corporations having already undertaken increased fiscal discipline as they anticipate tougher times ahead.

Source: SentimentTrader.

Source: FactSet Research.

As we mentioned last quarter, bad debt is the true culprit of deep recessions. Although interest rates are making future debt more expensive, the vast majority of current debt is fixed to low rates and will not encumber individuals or most corporations for quite some time. The combined effects are a market and economy prepared for the worst. On one hand this can be a self-fulfilling prophecy as weaker investment and hiring slows economic growth, but on the other this makes the most dangerous scenario of a major unexpected decline in economic activity less likely. We continue to believe this backdrop of financial health can mitigate the damage within the economy, while investors bearish positioning may provide an attractive longer-term entry point for many assets.

[1] https://www.bloomberg.com/news/articles/2022-08-26/powell-says-history-warns-against-prematurely-loosening-policy

[2] Compared to both their 200-day and 50-day moving averages, the pool of ETFs we track is at a relatively extreme level. This level was last seen at the market’s bottom in June and has historically yielded very strong forward returns on average. Since June 2000, the average 1-month forward return for the S&P 500 at levels this far below the 50-day moving average has been over 4%.

[3] Federal Reserve Bank of St. Louis, Federal Funds Rate from 1/1/2022 through 9/30/2022

[4] Micron Technology Inc., Fourth Quarter 2022 Earnings release

[5] The EAFE Index ETF (EFA is down 10.4% since 2/1/2020). S&P 600 P/E of 10.8 from Yardeni Research Inc. 9/30/2022.

[6] In addition to rents and wages mentioned below, home prices fell in August, government spending has been negative year-over-year for 5 quarters and various supplier price indices, most recently and notably the ISM prices paid index, are well off their highs.

[7] US Bureau of Labor Statistics, August Consumer Price Index release.

[8]US Bureau of Labor Statistics, August unemployment release

[9] An example of the market implementing Federal Reserve policy for them is in March/April of 2020 when the Federal Reserve indicated that it could buy fixed income ETFs that were trading below NAV. This announcement brough many fixed income ETFs back in line with the NAV and the Federal Reserve never needed to follow through with actual large-scale purchases of fixed income ETFs.

[10] Federal Reserve Bank of St. Louis, 9/30/22

[11] 1/30 for amortization = 3.3% + 3% mortgage = 6.3% prior, now that same math is 10.3%, a payment roughly 60% higher

[12] Koyfin. Data from June 6th to July 15th, 2022.

[13] Koyfin. Since 2/1/2020, the Energy sector (XLE) has risen 57.3%, while the Communications sector (XLC) has fallen -10.2%.

[14] Federal Reserve Bank of St. Louis. Money market funds hold $5.032 Trillion while Bank deposits are $17.953 Trillion. Those are up from $4.727 Trillion and $13.320 Trillion pre-pandemic.

Disclosures

Copyright © 2022 Beaumont Capital Management LLC. All rights reserved. All materials appearing in this commentary are protected by copyright as a collective work or compilation under U.S. copyright laws and are the property of Beaumont Capital Management. You may not copy, reproduce, publish, use, create derivative works, transmit, sell or in any way exploit any content, in whole or in part, in this commentary without express permission from Beaumont Capital Management.

This material is provided for informational purposes only and does not in any sense constitute a solicitation or offer for the purchase or sale of a specific security or other investment options, nor does it constitute investment advice for any person. The material may contain forward or backward-looking statements regarding intent, beliefs regarding current or past expectations. The views expressed are also subject to change based on market and other conditions. The information presented in this report is based on data obtained from third party sources. Although it is believed to be accurate, no representation or warranty is made as to its accuracy or completeness.

The charts and infographics contained in this blog are typically based on data obtained from third parties and are believed to be accurate. The commentary included is the opinion of the author and subject to change at any time. Any reference to specific securities or investments are for illustrative purposes only and are not intended as investment advice nor are they a recommendation to take any action. Individual securities mentioned may be held in client accounts. Past performance is no guarantee of future results.

As with all investments, there are associated inherent risks including loss of principal. Stock markets, especially foreign markets, are volatile and can decline significantly in response to adverse issuer, political, regulatory, market, or economic developments. Sector and factor investments concentrate in a particular industry or investment attribute, and the investments’ performance could depend heavily on the performance of that industry or attribute and be more volatile than the performance of less concentrated investment options and the market as a whole. Securities of companies with smaller market capitalizations tend to be more volatile and less liquid than larger company stocks. Foreign markets, particularly emerging markets, can be more volatile than U.S. markets due to increased political, regulatory, social or economic uncertainties. Fixed Income investments have exposure to credit, interest rate, market, and inflation risk. Diversification does not ensure a profit or guarantee against a loss.

The MSCI ACWI Index is designed to represent performance of the full opportunity set of large- and mid-cap stocks across 23 developed and 24 emerging markets. The ICE BofA US Broad Market Index tracks the performance of US dollar denominated investment grade debt publicly issued in the US domestic market, including US Treasury, quasi-government, corporate, securitized and collateralized securities.

For Investment Professional use with clients, not for independent distribution.

Please contact your BCM Regional Consultant for more information or to address any questions that you may have.

Beaumont Capital Management LLC

125 Newbury St. 4th Floor, Boston, MA 02116 (844-401-7699)