Every news item these days seems to be a “hair on fire” event, i.e., the best or the worst ever seen in history! We’ve joked that we’re seeing an unprecedented use of the word “unprecedented.”

Of course, a constant stream of extremes is not reality, but investors are nonetheless faced with the difficult task of sifting true investment information from the harrowing cries of impending doom.

Historically, investors have been better off remaining dispassionate and objective during such hyperbolic periods. A clear-eyed review of history and of fundamental data will likely be investors’ best guides to maintaining portfolio sanity during these…ahem…unprecedented times.

The current bank failures are typical

The whole point to tightening monetary policy is to make banking less profitable and discourage lending and risk-taking. The Fed raises the cost of funding specifically to disintermediate the banking system and make lending to the economy more expensive.

Raising interest rates effectively raises the entire economy’s hurdle rate (i.e., the minimum required rate of return of a financial or capital investment), which makes cash more attractive relative to longer-term investments. That, in turn, curtails both financial and real investment. Because funding becomes more expensive, lending growth slows, and asset valuations decrease, marginal and poorly managed banks tend to fail subsequent to the Fed tightening monetary policy.

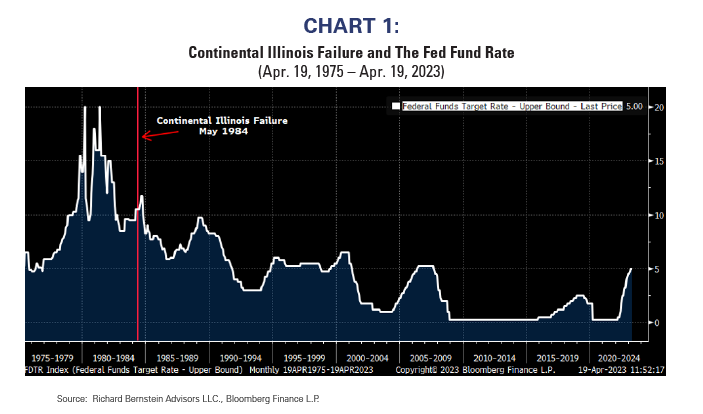

The first major bank failure during my career was Continental Illinois in 1984. Continental Illinois was the 7th largest US bank at the time, and their bailout initiated the phrase “too big to fail.” As financial theory might have suggested, the bank’s failure came after the Fed raised interest rates (See Chart 1)

The recent bank failures were caused by banks skewing their balance sheets’ toward a single industry: technology-related loans. Continental Illinois similarly over-extended by concentrating in energy and secondarily in emerging markets. Also similar to recent failures, Continental Illinois generally had very poor risk management overseeing a poorly diversified portfolio. In addition, the FDIC’s response to the 1984 failure was analogous to the recent government response in that deposits were guaranteed above the FDIC deposit ceiling, which was $100,000 in 1984 versus $250,000 today.

The recent bank failures, therefore, do not seem the least bit unprecedented. Consider the following similarities between Continental Illinois’ failure in 1984 and the recent bank failures:

- Significant single industry/region customer concentration.

- Preceded by Fed tightening.

- Depositors guaranteed above the FDIC ceiling.

Inverted yield curves are typically investors’ warning signal

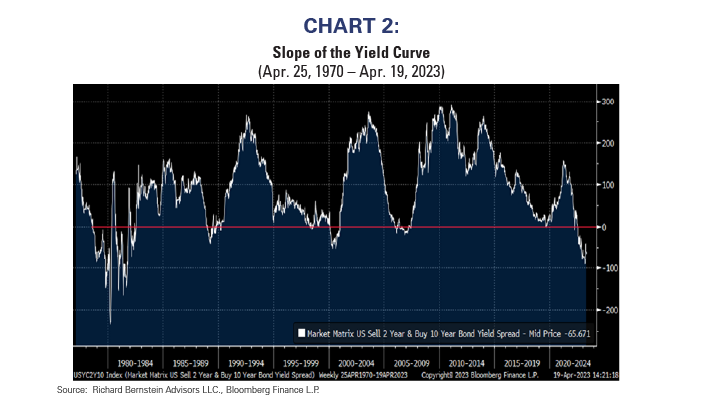

Traditional banking has a relatively simple business model. Banks take deposits and in return pay depositors a short-term interest rate. Banks then use those deposits to make loans and get paid interest rates that track with longer maturity rates along the yield curve. Because yield curves tend to be positively sloped (i.e., long-term interest rates are higher than short-term interest rates), banks’ loan profitability is directly tied to the slope of the curve.

In theory, steeper yield curves provide greater incentive for banks to lend because lending margins are greater, whereas inverted yield curves (i.e., short-term interest rates are higher than long-term interest rates) tend to curtail lending because an increasing proportion of loans are either unprofitable or not profitable enough to account for the risk of the loan.

Some investors describe the slope of the yield curve as an indicator of future nominal economic growth, but it is actually more than simply an indicator. The slope of the curve itself acts as a stimulator or regulator of the economy by providing an incentive for the banking system to increase or decrease lending. Steeper yield curves actually stimulate the economy, whereas inverted ones slow the economy. Yield curves are more than simply indicators; they are policy tools.

As one can see in Chart 2, the yield curve (defined as the spread between the 10-Year T-Note and the 2-Year T-Note) inverted in July 2022. Accordingly, we quickly reduced our regional bank exposure in July, and then broadly moved to a significant underweight in November 2022 as the yield curve reached historic levels of inversion.

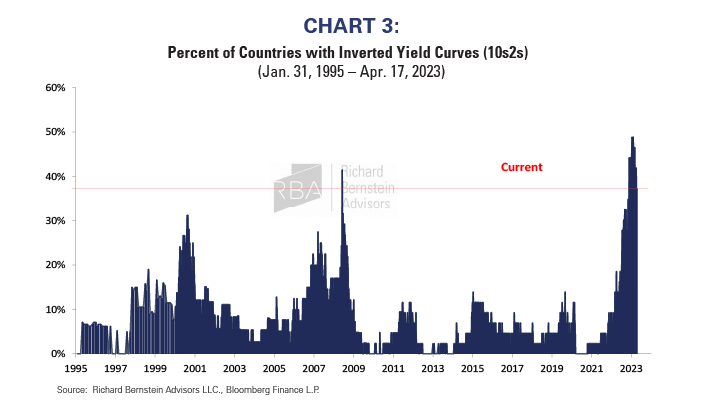

The Fed is not the only central bank currently tightening monetary policy and causing an inverted yield curve. Chart 3 shows the proportion through time of countries that we follow that have inverted yield curves. Recently, the proportion hit an all-time high, indicating that global central banks are trying to hinder credit creation on a global scale.

You can lead a horse to water, but you can’t make it lend

It is well known there are considerable lags between the Federal Reserve setting monetary policy and when that policy changes banks’ lending policies and when lending stimulates or slows the economy. Central banks can only set policy, and can’t actually control bank behavior.

For example, banks’ lending growth tends to be the strongest toward the end of the cycle because the economy is stronger and lending risks are perceived to be less. Banks, sometimes imprudently, continue to take excessive risk despite the Fed tightening monetary policy. At the beginning of cycles, banks perceive risk to be greater than it actually is and are overly hesitant to lend.

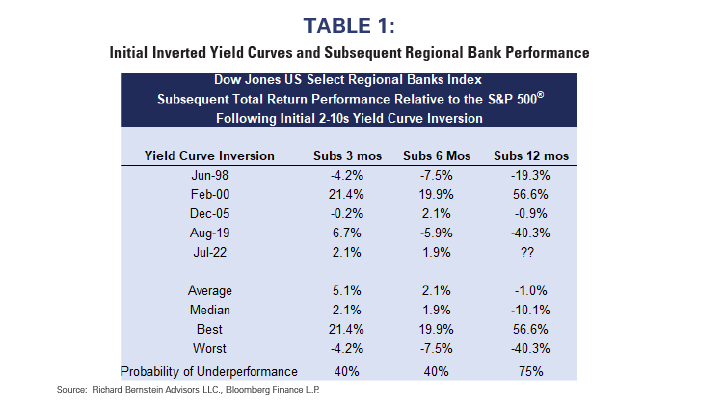

The lags are evident in banks’ stock prices. Table 1 shows the performance of Regional Bank stocks during the 3, 6, and 12 months after the yield curve has historically inverted. The stocks perform relatively well over the subsequent 3 and 6 months because business remains strong. However, by 12 months after inversion, the excessive risk taking begins to affect the bank stocks and they generally underperform.

In fact, Regional Bank stocks tend to underperform 75% of the time during the 12-month periods after the yield curve inverts. Because the yield curve inverted in July 2022, the recent underperformance of the Regional Banks seems to fit the historical norm.

Don’t fret. Investors seem aware of the risks

At RBA, we try to balance economic and profit fundamentals with investor sentiment. The greatest investment opportunities tend to be when profits and liquidity fundamentals are improving yet investors are too scared to take advantage of the assets that benefit from that fundamental improvement. Vice versa, we try to avoid situations in which fundamentals are deteriorating yet investors don’t care.

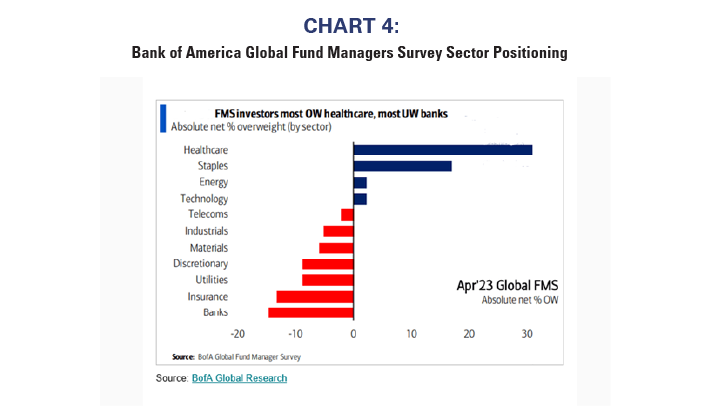

The bank stocks appear to be a combination of these factors. Profits and liquidity fundamentals are still deteriorating, but investors seem aware. Chart 4 shows recent results of the Bank of America Global Fund Managers Survey. According to their survey, fund managers’ portfolios are underweighted bank stocks more than any other group, and they now view a bank credit crunch as the biggest tail risk.

This suggests that the risks are well known. If fundamentals do improve, then it could imply a stronger weight in the sector might be appropriate. For the time being, however, we feel comfortable with our sizable underweight.

Don’t get caught in the constant hyperbole

Henny Penny (a.k.a Chicken Little) is perhaps the most famous hyperbolic news person, but many have claimed in various forms that the end is near. Today’s Henny Pennies decry the end of banking, the end of capitalism, or the end of virtually anything. That’s not reality. This isn’t the first banking crisis in US history and it won’t be the last.

Investors who listen to Henny Penny seem likely to both over-assess the risks within the market and miss future opportunities. Rather than structuring portfolios against any risk that could ever occur, the key to rational investing is following an intellectually sound and well-tested investment process.

For more news, information, and analysis, visit the ETF Strategist Channel.

INDEX DESCRIPTIONS:

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indices. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indices are not actively managed and investors cannot invest directly in the indices.

S&P 500®: S&P 500® Index: The S&P 500® Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad US economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Dow Jones U.S. Select Regional Banks Total Return Index measures regional banks providing a broad range of financial services, including retail banking, loans and money transmissions.