This week, we explore outsourced portfolio construction, make a case for the IPS as a tool for transparency, and offer an IPS template we developed specifically for ETF managers.

A Policy for Growth

We’ve been talking a lot about transparency as one of the key factors in client alignment. In our experience, advisors who embrace transparency in their practices are likely to set policies and procedures that clearly state the value proposition of using ETF portfolios for growing client assets. With that in mind, we would like to offer a template for these guidelines, designed to help advisors build unique and intelligent ETF portfolios. The first step is to create an Investment Policy Statement (IPS).

Self-Driving vs. a Road Mapfor ETF Portfolios

An IPS can be a powerful road map, allowing advisors to deliver successful ETF portfolios to clients. That said, Crystal Kim noted in Baron’s on June 1, 2019 that many advisors choose a simpler self-driving approach:

Some 12% of the 350,000 financial advisors in the U.S. are fully outsourcing portfolio construction to model portfolios from the likes of Blackrock, Goldman Sachs, Charles Schwab, Vanguard, State Street, Merrill Lynch, and Morgan Stanley. That suggests $2.5 trillion in assets…

As asset managers focused on ETFs for decades, we at the ETF Think Tank urge advisors to avoid this approach by asking these 4 key questions:

- Can advisors truly be fiduciaries when accepting “free” models from conflicted sources?

- Will clients continue to see value in advisors that offer models dominated by one issuer’s branded products?

- Can advisors justify a value proposition above robo-advisors with simplistic monochromatic portfolios?

- Is a firm model portable?

If you answered ‘no’ to all 4, we agree. Although we like the concept of using ETF models to streamline an advisory practice, allowing the team to focus on growth, complete outsourcing of portfolio management can be dangerous, especially when it is “free.”

We believe advisors will achieve more sustainable growth with a core/satellite approach, with an internal or outsourced CIO, or simply by properly aligning with a model provider; all of which are methods that can be outlined in an IPS.

Ok, So What is an IPS?

Good luck searching for a definition of an ETF portfolio IPS. There appears to be very little interest in setting a format for ETF portfolios and most investors seem to rely on traditional asset allocations with the largest and cheapest ETFs. Investopedia broadly defines an IPS like this:

An investment policy statement (IPS) is a document drafted between a portfolio manager and a client that outlines general rules for the manager. This statement provides the general investment goals and objectives of a client and describes the strategies that the manager should employ to meet these objectives. Specific information on matters such as asset allocation, risk tolerance and liquidity requirements are included in an investment policy statement.

This definition is great starting point, in that it outlines goals, objectives, risk tolerance and certain constraints. Below we extend and enhance this IPS concept and apply it to ETF portfolios:

ETF IPS OUTLINE

1. Background

2. Definition of Duties

3. Constraints

4. Asset Allocation

5. Benchmark

6. Security Selection

7. Review Process

Background, Definition of Duties & Constraints (items 1-3)

The first three components of an ETF portfolio IPS provide context and establish the primary rules governing the strategy. The background is mainly there to explain why a portfolio is being created. Advisors should document the objective of the portfolios, the history and culture of the advisor and value proposition offered by the strategist. Definition of duties allows for describing the team, roles and outside resources like an OCIO or research subscription. Within this section the frequency of formal meetings should be defined. Finally, constraints, which are both acknowledgement of regulation and/or custodial firm policies like proxy voting. Additionally, this section should deem self-imposed rules like liquidity requirements or types of securities available for consideration. The purpose of the first three sections of the outline is to create parameters that allow for clear portfolio management without rehashing the fundamental concepts. This is, at its core, the structure that matters.

Asset Allocation & Benchmarks (items 4-5)

Although these two concepts are similar, the asset allocation and benchmarks serve very distinct roles in the ETF portfolio IPS. First, the asset allocation section should define the number of strategies or variations based on time horizon or risk tolerance. The asset allocation should also define the dynamics of the portfolio as tactical, strategic or some hybrid variation. This information can then be used to establish benchmarks. We tend to recommend two versions of a benchmark for each strategy; an internal blended benchmark that aligns with the geographic and market cap designation of the portfolio, and a straightforward external benchmark for marketing that aligns simply with the asset breakdown of bonds to equities. An example is provided below:

INTERNAL MODERATE

1. 35% S&P 1500

2. 13% MSCI EAFE

3. 2% MSCI Emerging

4. 20% Barclays Agg Bond

5. 30% Barclays Gov’t 1-3 Year

EXTERNAL MODERATE

1. 55% MSCI World

2. 45% Barclays Gov’t 1-3 Year

Benchmarks are used in the portfolio management process to measure the choices made in asset allocation and security selection. They can also serve as a great indicator of future risk. In the example below, we compare the returns and fundamentals of a hypothetical moderate model to an internal and external benchmark. The 5-year return column is outlined in black to convey the use of two benchmarks as way to illustrate the return contribution from asset allocation versus security selection.

Security Selection Process (Item 6)

Within this section of an IPS, advisors should define a buy discipline and a sell discipline. This is where having a common language for describing and researching ETFs is paramount. In prior ETF Think Tank Weekly Research communications, we noted the importance of naming conventions for understanding and researching ETFs. And here we identify another reason. In The ETF Think Tank Security Master, we use the underlying holdings of an ETF as the basis for this common nomenclature.

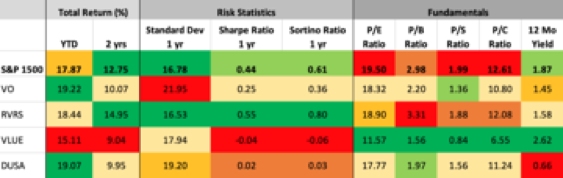

The security selection process should start with outlining a hierarchy of attributes that could initiate a purchase, like exposure, fees, sponsor or concentration. The tools in the etfthinktank.com are designed to help evaluate these types of attributes. Once a position is chosen, a benchmark should be established for each position before purchase. The benchmark for each position is the key to monitoring and triggering the sell discipline that could be performance based, trend based, or fundamental. Below we provide a hypothetical example of US-focused ETFs benchmarked to the S&P 1500.

The Review Process (item 7)

Once all the processes, benchmarks and securities are established as a portfolio, it is important to establish a formal review schedule. We recommend reviewing asset allocation and security selection at least once a month. A more formal investment committee should be established at least annually to review all the aspects of your IPS.

So, I have an IPS, Now What?

Advisors who have established and maintained an IPS for their ETF portfolios should be able to articulate the unique value proposition offered to investment clients. That value should be clear, offered as a fiduciary, portable and provide concise differentiation. The IPS is not an auto pilot but rather a road map defining the value and process advisors deliver to clients. Following this road map can reduce the amount of time advisors spend reviewing similar ideas, help prevent mistakes, and allow time to focus on growth. The ETF IPS can also be the basis for an advisor’s website or in other marketing collateral.

The ETF Think Tank is a community of advisors growing with use of ETFs, and the ETF IPS is a road map that can assist with that growth.

This article was contributed by the team at Toroso Investments, creators of the ETF Think Tank and a participant in the ETF Strategist Channel.

Click here to see disclosures.