By Chris Konstantinos, CFA

Two Decades of Studying Mean Reversion in Markets – What We Have Learned

Our Weekly View is typically a timely look at recent market-moving news, what RiverFront thinks about it, and how it may or may not affect our portfolio positioning. Today is a bit different. We are taking a step back today in order to provide a retrospective of what we’ve learned in our more than two decades of studying the effects of price mean reversion on future returns, both here at RiverFront Investment Group and at a predecessor firm where many of our investment team previously worked together.

Every plan is a good one – until the first shot is fired – Carl Von Clausewitz

The ‘Science’

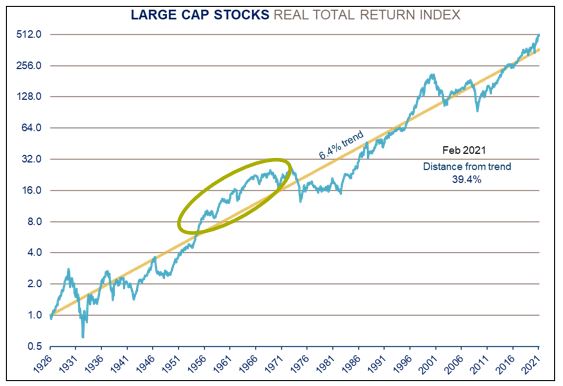

It is often said that asset management is as much an art as a science. We concur – hence our tagline here at RiverFront is ‘The Art and Science of Dynamic Investing.’ We believe that the prime determinant of long-term returns tends to be the price you pay for an asset at the outset of your investment – the mathematical ‘science’ of asset valuation, if you will. We believe the distance above or below a persistent long-term trend line can give investors powerful clues into future returns, especially at extremes. We call this concept Price Matters®. This power of ‘mean reversion’ works in investors’ favor especially when markets are significantly below trend…and against the investor buying into markets trading well above trend. We also believe that this signal explains more of your return the longer your forecast horizon is. A 2020 Goldman Sachs paper suggests that starting valuation has explained roughly 50% of US 10-year forward returns historically, going back to the 1930s.

The ‘Art’

If starting price accounts for roughly half of forward returns, some of the remaining 50% we believe comes from the ‘art’. The ‘art’ for us in part comes in adjusting the science to the regime we find ourselves in, understanding business cycles, and making judgments about current fundamental trends. We also place significant emphasis on investor sentiment and price momentum, explicitly building both into our asset allocation process. In order for a client to be emotionally able to commit to remain in markets long enough for mean reversion to work, we think it requires a flexible asset allocation – not a ‘set and forget’ methodology. While on paper one might end up with a similar long-term return with ‘set and forget’ vs. a dynamic approach, we believe the path the market takes to get those returns plays a big role in whether or not someone actually sticks to the agreed-upon allocation.

The ‘art’ also comes in adjusting for human behavior patterns. This is a simple recognition of the emotional impact of greed…and especially fear. While buying low and selling high make logical sense, in practice humans are emotionally wired to do the opposite in our experience, abandoning their long-term plan in moments of extreme stress. This is a psychological problem with important practical implications; the compounding effect of stock price appreciation and dividend payments can’t work in your favor if you’re not invested.

In order to combat this, we engage in active risk management, which we believe creates ‘emotional alpha.’ We define emotional alpha as the value of helping a client navigate market swings without making decisions purely on emotion. Emotional alpha is what keeps an investor invested and reduces the risk that they give up on their plan at the worst time. For more on the concept of emotional alpha, see here.

This is why we believe in a dynamic asset allocation discipline which recognizes the importance of long-term value but also allows for the possibility of unforeseen events, with defined processes to navigate them – our ‘tactical’ shifts. We think our approach is especially important for clients who have an investment horizon of seven years or less…which describes many of the clients we work with.

Two Decades of Price Matters®: What We’ve Learned

Two of our core values here at RiverFront are ‘humility’ and ‘accountability’. These values have instilled in our investment team a culture of continuous improvement, whereby we constantly evaluate our investment processes and explore whether there is a more effective way to do things. The ultra-low interest rate environment and the surge in money printing across the globe appear to have impacted the efficacy of traditional valuation measures. As a result, we have been regularly reevaluating and adjusting our processes for this environment.

In analyzing the biggest asset allocation decision – stocks vs. bonds – we believe Price Matters® has remained a very useful barometer in this era of ‘financial repression’. It has given us invaluable feedback about the continuing attractiveness of stocks relative to bonds in a decade-plus that has incorporated acute periods of stress, including a global financial crisis, the Euro crisis, the ‘Taper Tantrum’, Brexit, and, most recently, the deadliest global pandemic in a century.

Source: RiverFront Investment Group, calculated based on data from CRSP 1925 US Indices Database ©2021 Center for Research in Security Prices (CRSP®), Booth School of Business, The University of Chicago. Data from Jan 1926 through Feb 2021. Past performance is no guarantee of future results. It is not possible to invest directly in an index.

However, another learning from the last decade is that a historical ‘regime’ – as defined by inflation and interest rates –can have a major impact on the speed and magnitude of mean reversion. The massive pandemic-fueled fiscal spending that is now accompanying the monetary easing is only exacerbating the distortion. Consequently, over the last few years we have chosen to apply a lower weighting to our Price Matters® inputs in our asset allocation modelling for shorter-to-intermediate term time frame investing. We see parallels to the 1950s-1960s, where our Price Matters® work suggested stocks were overvalued…yet they stayed above trend until the early 1970s, providing above-average returns for stocks during this period (see chart, green oval). For more on Lessons from Price Matters, see here.

Mean reversion’s ‘Achilles Heel’ comes if one continues to use a trend that is no longer valid and so we believe it is important that our team is constantly working to validate trends via fundamental analysis. The concept of reversion to a mean hinges on a belief that the trend will continue unabated into the future. This is why we have higher conviction in Price Matters® conclusions in areas such as the United States, where we have a century’s worth of data from which to study the trend. We place less emphasis on mean reversion as a valuation technique in areas such as emerging markets, where data goes back less than 40 years and is marked by significant ‘regime shifts’ in growth. We also have learned that some countries – such as Japan – do not exhibit strong mean reversion historically, rendering this type of valuation work less useful both in absolute terms and with regards to comparing two different regions of the world. For more on this topic, see our 2020 Strategic Review here.

Our conclusion is that Price Matters® and other deep-value based asset allocation methods remain a good framework for thinking through the big picture – especially the stock-vs bond question – but requires augmentation from an ‘ensemble’ of other strategic analysis of regimes, macro drivers and momentum processes to be most effective for time horizon investing in periods shorter than a decade or longer.

Important Disclosure Information

The comments above refer generally to financial markets and not RiverFront portfolios or any related performance. Opinions expressed are current as of the date shown and are subject to change. Past performance is not indicative of future results and diversification does not ensure a profit or protect against loss. All investments carry some level of risk, including loss of principal. An investment cannot be made directly in an index.

Chartered Financial Analyst is a professional designation given by the CFA Institute (formerly AIMR) that measures the competence and integrity of financial analysts. Candidates are required to pass three levels of exams covering areas such as accounting, economics, ethics, money management and security analysis. Four years of investment/financial career experience are required before one can become a CFA charterholder. Enrollees in the program must hold a bachelor’s degree.

Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed.

This report does not provide recipients with information or advice that is sufficient on which to base an investment decision. This report does not take into account the specific investment objectives, financial situation or need of any particular client and may not be suitable for all types of investors. Recipients should consider the contents of this report as a single factor in making an investment decision. Additional fundamental and other analyses would be required to make an investment decision about any individual security identified in this report.

In a rising interest rate environment, the value of fixed-income securities generally declines.

Investing in foreign companies poses additional risks since political and economic events unique to a country or region may affect those markets and their issuers. In addition to such general international risks, the portfolio may also be exposed to currency fluctuation risks and emerging markets risks as described further below.

Changes in the value of foreign currencies compared to the U.S. dollar may affect (positively or negatively) the value of the portfolio’s investments. Such currency movements may occur separately from, and/or in response to, events that do not otherwise affect the value of the security in the issuer’s home country. Also, the value of the portfolio may be influenced by currency exchange control regulations. The currencies of emerging market countries may experience significant declines against the U.S. dollar, and devaluation may occur subsequent to investments in these currencies by the portfolio.

Foreign investments, especially investments in emerging markets, can be riskier and more volatile than investments in the U.S. and are considered speculative and subject to heightened risks in addition to the general risks of investing in non-U.S. securities. Also, inflation and rapid fluctuations in inflation rates have had, and may continue to have, negative effects on the economies and securities markets of certain emerging market countries.

Stocks represent partial ownership of a corporation. If the corporation does well, its value increases, and investors share in the appreciation. However, if it goes bankrupt, or performs poorly, investors can lose their entire initial investment (i.e., the stock price can go to zero). Bonds represent a loan made by an investor to a corporation or government. As such, the investor gets a guaranteed interest rate for a specific period of time and expects to get their original investment back at the end of that time period, along with the interest earned. Investment risk is repayment of the principal (amount invested). In the event of a bankruptcy or other corporate disruption, bonds are senior to stocks. Investors should be aware of these differences prior to investing.

Mean reversion is the tendency of a variable, such as a stock price, to converge on an average value over time.

RiverFront’s Price Matters® discipline compares inflation-adjusted current prices relative to their long-term trend to help identify extremes in valuation. Blue line represents the Large Cap Real Return Index. Yellow line represents the Annualized Real Trend Line of Large Cap Real Total Return Index according to Price Matters®. Shown for illustrative purposes only, not indicative of RiverFront portfolio performance. Information or data shown or used in this material was received from sources believed to be reliable, but accuracy is not guaranteed. The chart above uses a logarithmic scale. Line movements will be dampened/subdued based on the exponential y-axis.

RiverFront Investment Group, LLC (“RiverFront”), is a registered investment adviser with the Securities and Exchange Commission. Registration as an investment adviser does not imply any level of skill or expertise. Any discussion of specific securities is provided for informational purposes only and should not be deemed as investment advice or a recommendation to buy or sell any individual security mentioned. RiverFront is affiliated with Robert W. Baird & Co. Incorporated (“Baird”), member FINRA/SIPC, from its minority ownership interest in RiverFront. RiverFront is owned primarily by its employees through RiverFront Investment Holding Group, LLC, the holding company for RiverFront. Baird Financial Corporation (BFC) is a minority owner of RiverFront Investment Holding Group, LLC and therefore an indirect owner of RiverFront. BFC is the parent company of Robert W. Baird & Co. Incorporated, a registered broker/dealer and investment adviser.

To review other risks and more information about RiverFront, please visit the website at www.riverfrontig.com and the Form ADV, Part 2A. Copyright ©2021 RiverFront Investment Group. All Rights Reserved. ID 1583500