By Ryan O’Malley, Sage Advisory

As the dust begins to settle following the extreme volatility seen in the second quarter of 2020, the corporate bond market has revealed opportunities. At Sage, we favor the communications, energy, and high-yield sectors as we believe they offer solid credit fundamental trends along with strong relative value.

Communications

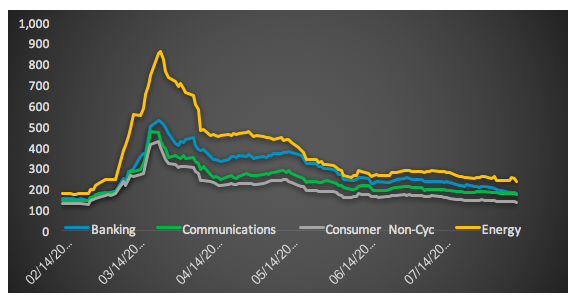

The fourth cheapest sector in the Bloomberg Barclays US Corporate Bond Index with an option-adjusted spread (OAS) of 154 bps, the communications sector has a number of liquid issuers with improving balance sheets and strong cash flow generation, such as CBS/Viacom and AT&T. These issuers have also benefitted from the increased demand for at-home entertainment and data as many consumers have eschewed brick-and-mortar retail and movie theaters for more at-home friendly options.

Corporate Bond Sector Spreads

Source: Bloomberg Barclays Indices

Energy

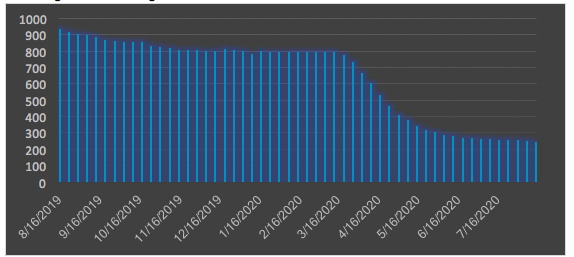

Energy is still the cheapest sector in the Bloomberg index after suffering an extreme dislocation during volatility in April. As the price of WTI oil has recovered nearly 100% from April lows to $42.16 currently, better capitalized companies are taking advantage of robust demand for investment grade paper and tendering for short-maturity, high-coupon bonds to decrease interest expense and improve their balance sheets. At the same time, global macro fundamentals have buoyed the outlook for commodities while supply has decreased dramatically, creating a more sustainable market for drillers that have the financial resources to take advantage of these favorable financing conditions. The following graph illustrates the slowdown in drilling activity, which has supported oil prices.

Baker Hughes U.S. Total Rig Count Index

Source: Bloomberg

High Yield

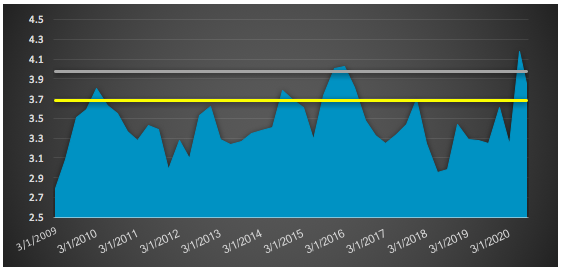

Sage continues to see value in the high-yield sector of the corporate bond market. The ratio of OAS offered by high yield compared to the overall corporate market is nearly 3.8x. This is close to the post-crisis high of 4.1x seen in June 2020. This is nearly two standard deviations higher than the median ratio since 2009, implying that we are still a range that is cheaper than nearly 95% of observations since the Great Financial Crisis.

Option-Adjusted Spread Ratio of High-Yield vs. Investment Grade Corporate Bonds

(Lines Represent One and Two Standard Deviations)

Source: Bloomberg

This article was contributed by the team at Sage Advisory, a participant in the ETF Strategist Channel.

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our web site at www.sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.