Election risk, recession risk, and more loom over second-half markets, creating the potential for heightened volatility. For those looking to dampen these potential effects within equities, the Fidelity Low Volatility Factor ETF (FDLO) may be one to consider.

Investors must contend with many risk factors in the second half, including that of elevated volatility. The Cboe Volatility Index (VIX) measures the implied volatility of the S&P 500, or expectations for volatility over the next 30 days. It’s often seen as a measure of market stress or an investor fear gauge.

The VIX logged its single-largest intraday spread (172%) in early August. This sharp move came on the heels of Japan’s central bank raising rates, rising recession concerns in the U.S., and ongoing geopolitical risks. The rapid unwind of the yen carry trade reverberated across global markets on Aug. 5, 2024. The VIX climbed as high as 65.73 at one point before declining to close at 68.57. Although the VIX has retreated back to levels in the mid-to-high teens shortly after the spike, this illustrates how quickly volatility can snowball in financial markets. It’s the third-highest level reached by the VIX, following a reading of 85 in October 2008 (great financial crisis) and 85 again in March 2020 (COVID-19 pandemic).

With many risk variables in play in the second half, low-volatility strategies may appeal to investors. Such strategies need not come at the cost of returns.

Low Volatility Investing With Fidelity’s FDLO

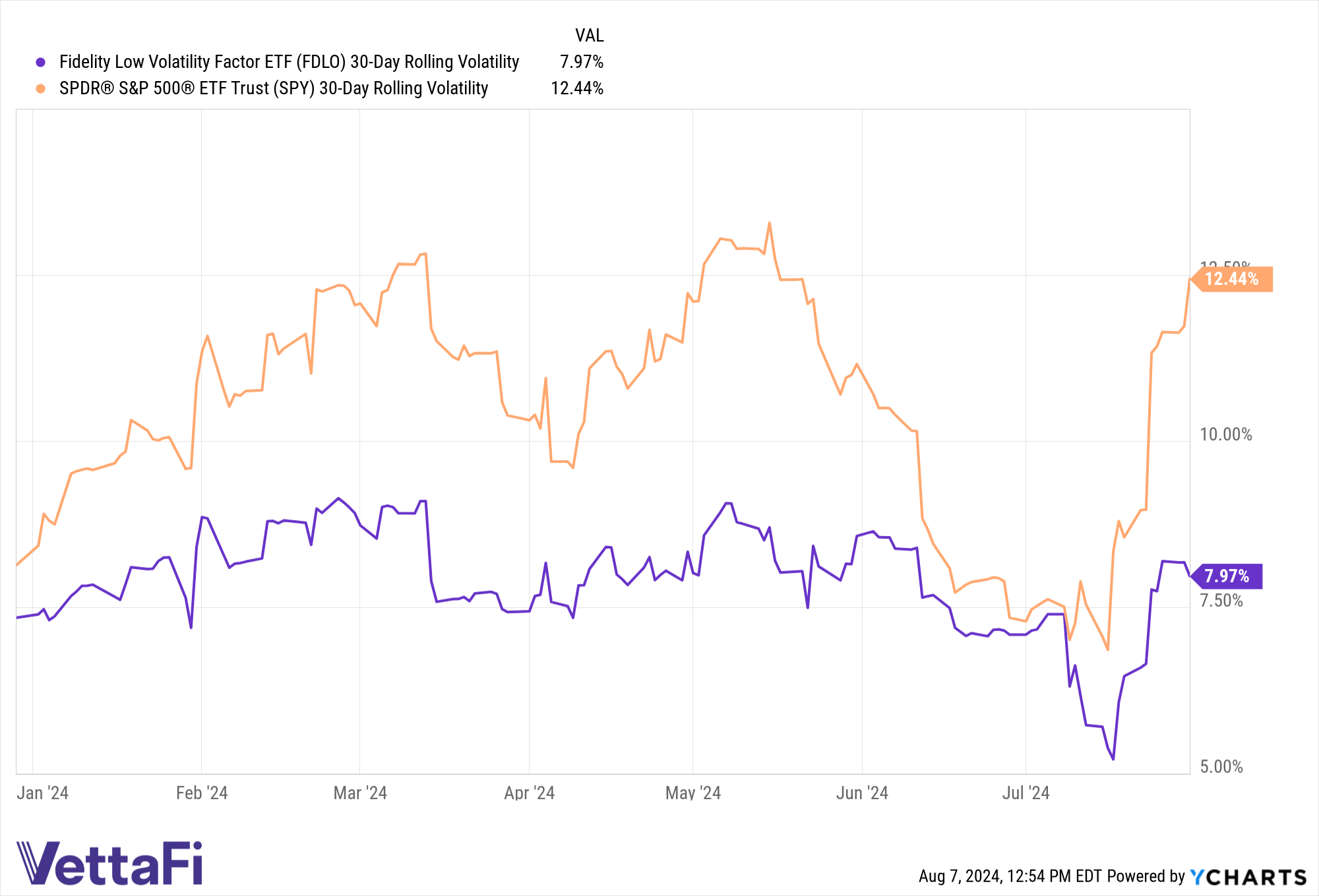

In the last year, FDLO generated total returns of 14.79% compared to the S&P 500 Index’s 18.77% as of 8/06/24 according to Y-charts data. Over the last three years, FDLO generated total returns of 18.55% compared to SPX’s 21.24% as of 8/06/24. Notably, the fund generates returns with reduced volatility compared to the broader market.

Y-charts calculates the 30-day rolling volatility by multiplying the standard deviation of the last 30 percentage changes in total return by the square-root of 252 (trading days each year). The SPDR S&P 500 ETF Trust (SPY) is used as a representative of broad equity volatility.

See also: “3 Key Considerations That Set Fidelity’s Factor ETFs Apart”

FDLO seeks to track the performance of the Fidelity U.S. Low Volatility Factor Index. The index begins with a starting universe comprising the 1,000 largest stocks by market cap. All securities in the universe receive scores based on their five-year standard deviation of price returns, five-year beta, and five-year standard deviation of earnings per share (EPS).

Scores favor those companies with lower standard deviation of returns, EPS, and lower beta. This creates a portfolio of companies with relatively more stable returns and earnings, as well as resilience to market declines.

The top-scoring stocks within each sector are selected for the index, adjusted for market-cap. This adjustment aims to eliminate potential unintended exposure to small cap stocks. Once the securities are selected, sector weights of the index are matched to the sector weights of the starting universe to eliminate unintended sector biases. Finally, within each sector, each stock is overweighted by the same amount (“equal active” weighting), which seeks reduce concentration risks in individual names.

FDLO carries an expense ratio of 0.15%.

For more news, information, and strategy, visit the ETF Investing Channel.

Fidelity Investments® is an independent company unaffiliated with VettaFi LLC (“VettaFi”). These articles do not form any kind of legal partnership, agency affiliation, or similar relationship between VettaFi and Fidelity Investments, nor is such a relationship created or implied by the articles herein. VettaFi LLC is the author and owner of these articles.

1163585.1.0