Capitol Hill and Wall Street are in two different cities, but when they interact on a regular basis, the results can beneficial for investors.

A prime example of investors deriving benefit from a policy push is the recent passage of the American Rescue Plan, which fixed income market observers view as a plus for municipal bonds. There could be benefits for taxable munis, which are accessible with the Invesco Taxable Municipal Bond Fund (NYSEArca: BAB).

Most municipal bonds are tax exempt, but the 584 holdings in BAB are taxable. These bonds are usually issued by a state or city or county when the federal government won’t assist with funding. Usually, taxable munis raise capital for projects that don’t benefit the public at large, such as a sports stadiums or private real estate projects.

That’s not a detriment for BAB. In fact, the case for the Invesco ETF is bolstered by the American Rescue Plan.

“State and local governments are receiving $350 billion of direct aid from the American Rescue Plan,” writes Charles Schwab’s Cooper Howard. “The restrictions on what the aid can or cannot be used on are much less stringent than the aid provided under the CARES Act that was signed into law in March 2020.”

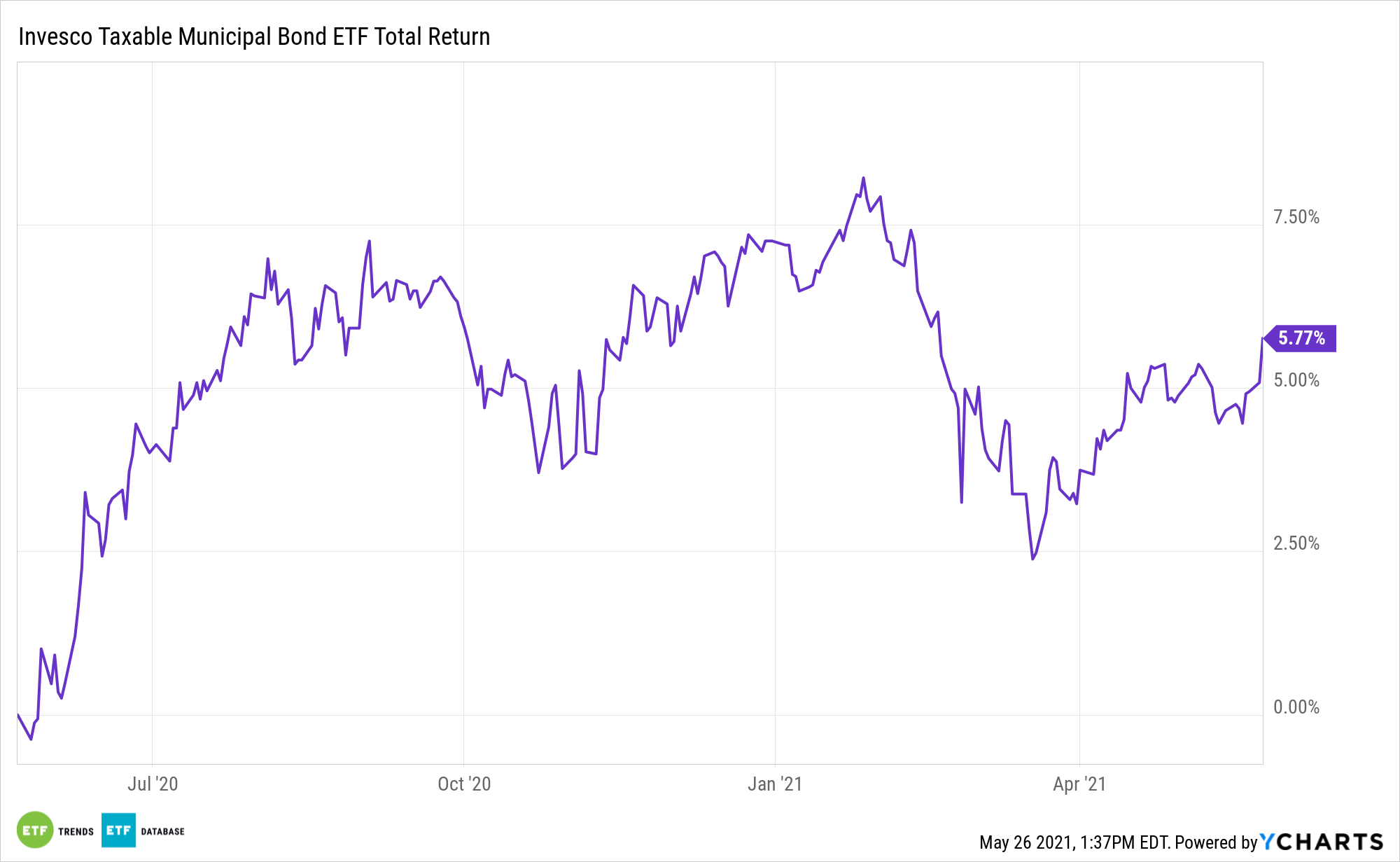

BAB: A Solid Bond Bet

While BAB lacks the tax benefits that come with traditional municipal bond ETFs, the Invesco fund makes up for it in other areas. For example, BAB has outperformed the S&P National AMT-Free Municipal Bond Index by 820 basis points over the past three years.

BAB also offers a higher level of income. It yields 2.88%, 77 basis points higher than the yield on the S&P National AMT-Free Municipal Bond Index. That’s an important point because the American Rescue Plan jumpstarted muni bond prices, meaning yields declined.

“Prior to the COVID-19 crisis, the five- and 10-year municipals over bonds (MOB) spreads averaged 88.9% and 94.5%, respectively. They quickly spiked in March 2020 due to the COVID-19 crisis and have since fallen. In fact, both the five- and 10-year tenors are the lowest going back to 2001,” according to Schwab’s Howard.

Over 28% of BAB’s components have maturities of one to five years or five to 10 years. BAB has a modified duration of 9.49 years, according to issuer data. Eighty-four percent of the ETF’s portfolio is rated AAA, AA, or A on the S&P scale.

For more news, information, and strategy, visit the ETF Education Channel.

The opinions and forecasts expressed herein are solely those of Tom Lydon, and may not actually come to pass. Information on this site should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any product.