When 2021 draws to a close, it will go down as a banner year for the real estate sector and real estate investment trusts (REITs).

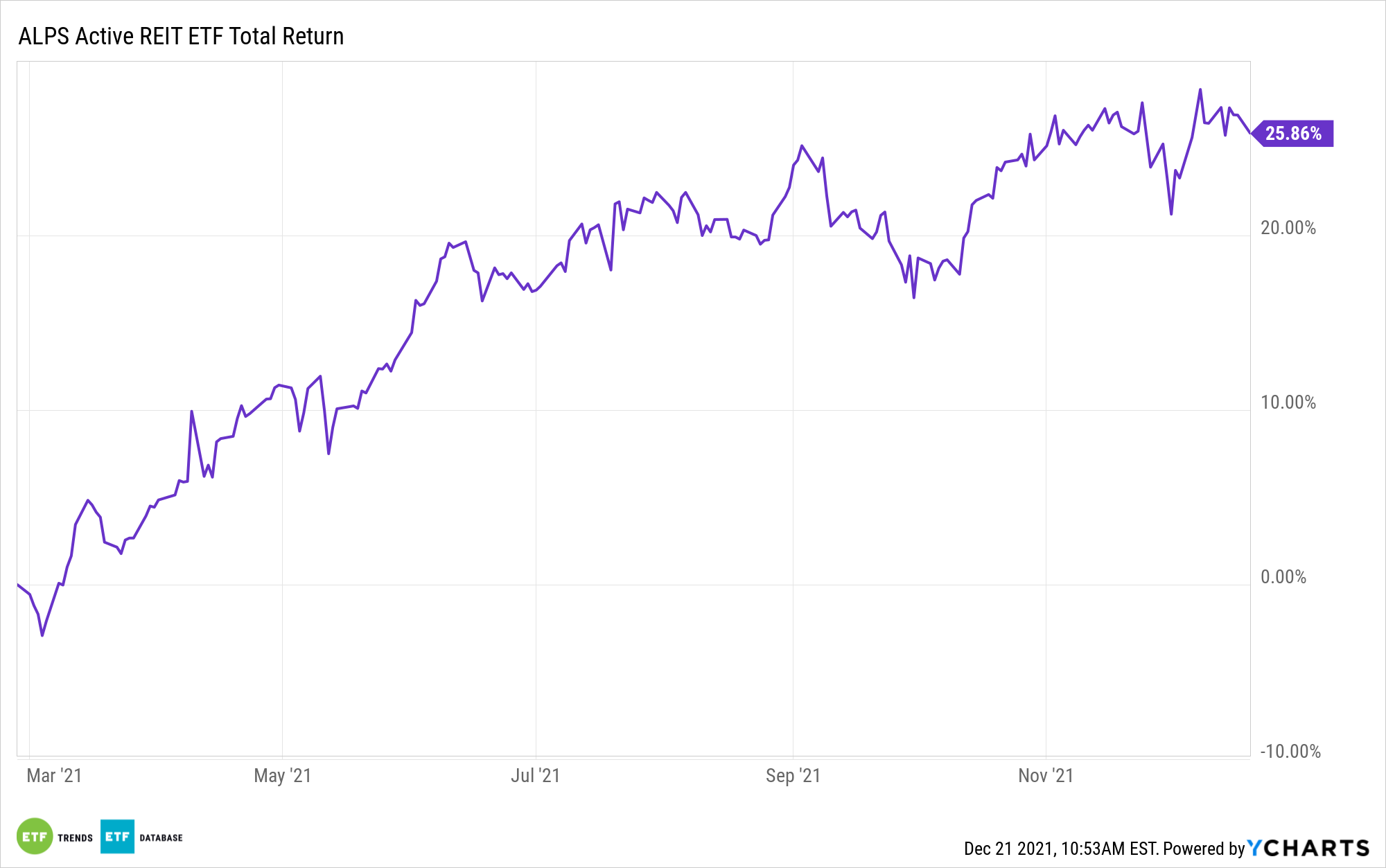

That’s a strong indication that the ALPS Active REIT ETF (NASDAQ: REIT) is one of this year’s more well-timed new ETFs, and that’s saying something since roughly 500 ETFs came to market in 2021. REIT debuted in late February, and it’s off to a solid start, but some market observers believe that REITs can continue delivering in 2022 even if interest rates rise.

“This year, however, REITs have provided a total return for the ages. The FTSE Nareit All REITs index has made 34%, versus 26% for the S&P 500 index,” reports Jack Hough for Barron’s. “That’s one reason the 10% prediction for 2022, which comes from Richard Hill, who runs REIT coverage for Morgan Stanley, looks bold. Doesn’t the group need a breather? Another reason is that the Federal Reserve just signaled an increased willingness to raise interest rates over the coming years. Aren’t rising rates a headwind for income investments?”

Managed by GSI Capital Advisors, REIT is actively managed, giving it an advantage over index-based strategies, particularly after REITs soared in 2021. Some real estate equities could be challenged to repeat 2021 in 2022, but the ALPS fund features a concentrated portfolio with high conviction names that could again outperform. That’s a plus, as is the broader bullish outlook for the sector.

“Hill’s forecast rests on the expectation that funds from operations, or FFO, a measure of REIT profitability, will rise 9.4% in 2022 and 7.7% in 2023, excluding a bigger bounceback for hotels. He expects share prices to lag slightly behind FFO growth. Don’t forget dividends—the aforementioned FTSE Nareit index yields just under 3%,” according to Barron’s.

Another benefit to REIT’s status as an actively managed fund is the ability of the fund’s managers to overweight real estate groups showing promise while avoiding those that could disappoint investors. An example of the latter category could be residential REITs in 2022.

“Increasing rents on new leases by mid- to high-teens percentages, but turns over only about a quarter of its homes a year to new tenants, suggesting years more of fast growth ahead,” notes Barron’s.

That speaks to REITs’ pricing power, a feather in the cap of REIT when inflation is expected to remain annoyingly high next year.

For more news, information, and strategy, visit the ETF Building Blocks Channel.

The opinions and forecasts expressed herein are solely those of Tom Lydon, and may not actually come to pass. Information on this site should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any product.