“’We have perceptions about our experience, and we judge them: ‘This is good.’ ‘This is bad.’ ‘This is neutral,’’ the Dalai Lama explained. ‘Then we have responses: fear, frustration, anger. We realize that these are just different aspects of mind. They are not the actual reality. Similarly, fearlessness, kindness, love, and forgiveness are also aspects of mind.’”

– Dalai Lama, Desmond Tutu, and Douglas Carlton Abrams, The Book of Joy

The View from 30,000 feet

Putting it all together

- Macro drivers mixed with market narratives last week to sustain the volatility cocktail being served in July.

- The major macro drivers impacting pricing continue to be, Inflation/Interest Rates, Earnings and the S. Election.

- Better than expected growth mixed with a continued disinflationary trends data, falling commodity prices and weak housing numbers, to provide support for the narrative that both growth and disinflation can peacefully coexist.

- Like proverbial good and evil angels sitting on opposite shoulders of Powell, the one whispering “higher for longer”, became quieter last week, while the ones whispering “cut now” began to The inherent negative message made markets nervous.

- After Goldman Sachs wrote a paper saying what a lot of people have been thinking, which is – How’s this whole AI thing going to actually make money? – investors grew skeptical of high-flying AI stocks, and consequently less enthusiastic about rewarding stellar earnings As the Magnificent 7 names began reporting last week, markets began saying, “show me the money”.

- Sector rotation was alive and well again last week as the S&P500 fell for the second straight week, while the Russell 2000 rose for the third straight There are a lot of theories being thrown around as to why the Russell 2000 is in rally mode and how sustainable it is. We think it’s a combination of two things that we believe will turn into themes in the second half of the year:

- With 30% of the Russell 2000 financing at floating rates, versus 6% of the S&P500, the Russell 2000 has a lot more to gain than the S&P500 from lower rates. In fact, many of the S&P500 companies have massive cash balances and are benefiting from high interest rates.

- Looking at earnings growth expectations as the year progresses, earnings growth is expected to broaden beyond the Magnificent 7, so it seems natural price appreciation should also follow.

- We remain positive on risk assets, specifically equities, with a caveat, our view hinges on the employment and housing markets holding up to support consumption, while inflation remains benign.

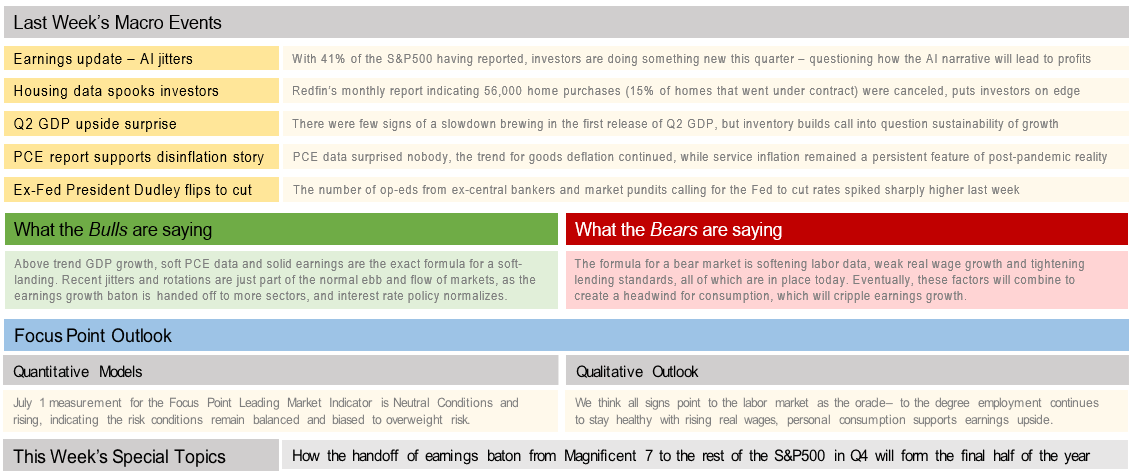

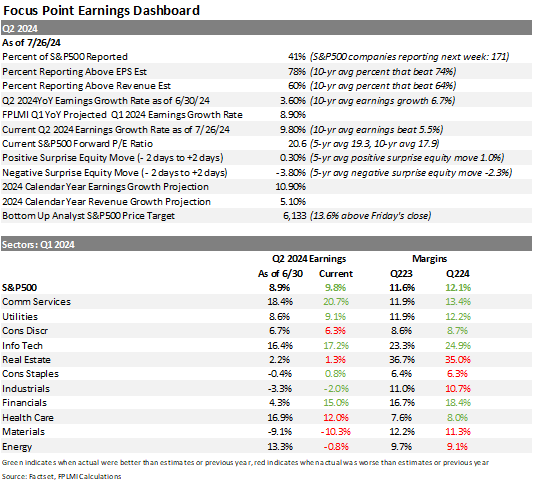

Earnings update – AI jitters

- With 41% of the S&P500 having reported earning for Q22024, some take-aways:

- On June 25, 2024, Goldman Sachs published a report titled “Gen AI: Too Much Spend, Too Little Benefit?”, that is being heralded as the pin that is popping the AI balloon, calling into question the reasoning behind $1t spend on AI, and raising the standard the AI titans are being held to for their valuations.

- Last week, was a good example of the new standards, as investors took Alphabet to the woodshed after beating their earnings estimate, questioning the sustainability of growth.

- Other trends:

- Earnings beats as percentage of companies are about average, but by a smaller dollar amount than average.

- Revenue beats as a percentage of companies falling are short of average.

- Companies being punished for earnings misses, and scantly rewarded for beats.

- Margins in old economy stocks are coming under pressure, while new economy stocks power ahead.

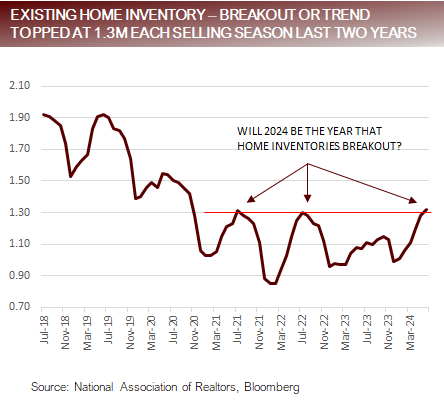

Housing data spooks investors

- The fireworks in housing started last week when Redfin published its monthly housing report. Highlights from the report include:

- 56,000 homes purchases were canceled last month, totaling 15% of the homes that went under contract.

- Specific geographies were especially hard hit, with areas within Florida, Texas and Nevada all having cancelation rates of over 20%.

- 20% of homes for sale last month underwent a price cut.

- The number of homes that sold dropped 1% last month during the peak of what is considered selling season.

- They noted that the median home sale prices last month hit a record $442,525, further pressuring affordability.

- Other negative news published by Redfin hitting the tape last week on the housing market included:

- Stale Inventory, defined as homes listed for more than 30 days, increased to 64.7%, and is climbing fast, with over 40% of listing having been on the market more than 60 days.

- Active listings are up 18.7% year-over-year, with number of months of supply at the highest level for this time of year in the past four years.

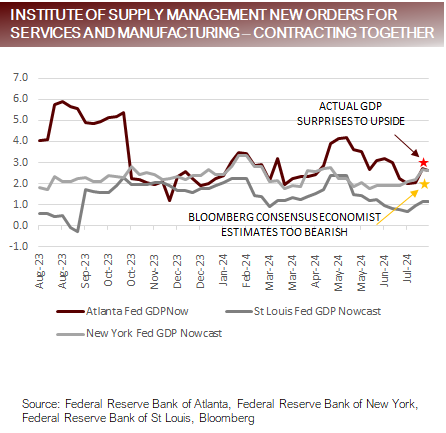

Q2 GDP upside surprise

- On Thursday last week, the first estimate of Q2 GDP was Prior to the release estimates included:

- Atlanta Fed GDP Now 2.6%

- New York Fed GDP Nowcast 2.6%

- St. Louis Fed GDP Nowcast 1.1%

- Bloomberg Consensus Estimate 2.0%

- Actual GDP was 2.8%, which was above all but one of the 69 economists who made up the Bloomberg Consensus Hats off to Nomura for standing out as the only optimistic one in the bunch.

- Much of the beat can be attributed to inventory, which added 0.8% to GDP for the quarter and not expected to repeat.

- We like to look at a Final Sales to Domestic Purchasers because it strips out the volatile inventories and import/export data. It looked good at 6%. The average Final Sales to Domestic Purchasers the quarter before each of the last five recessions was 1.3%, which would make the latest reading unusually strong if we were to be entering a recession today.

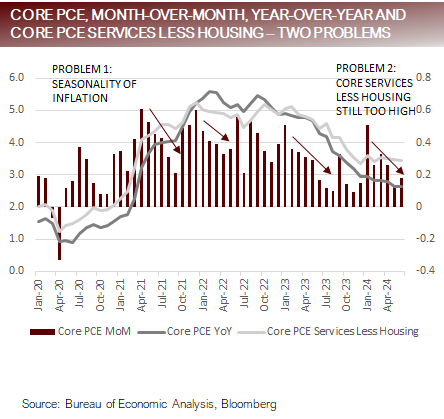

PCE report supports disinflation story

- PCE and Core PCE came in largely inline with expectations, showing a number of trends:

- Goods inflation continues to moderate, while Services remain solidly above the Fed’s comfort level. The same issue that is plaguing many other developed markets such as the UK and Canada.

- Economists and Strategists that are leaning towards expecting a rapid fall off in the pace of inflation were quick to point out the that the 3-month annualized pace of inflation is 5%. We don’t find much comfort in annualizing three months of data.

- Based on seasonality, things about to get harder from here.

- Since 2021, out of the 12 months of the lowest average monthly increase in PCE was in the month of July.

- The three-month average of June, July and August represented the lowest average three months of PCE in the preceding four years.

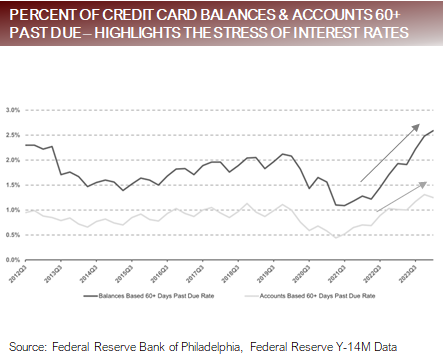

Ex-Fed President Dudley flips to cut

- Bill Dudley, who served as the president of the New York Fed from 2009 to 2018, and the vice-chairman of the Fed, wrote an op-ed titled “I Changed My Mind: The Fed Needs to Cut Now”. Highlights include:

- The facts have changed so Dudley has changed his mind from “higher for longer” to “cut now”.

- Pandemic saving have been drained.

- Only the wealthiest of households able to maintain spending.

- Lower income levels are being squeezed by high rates.

- Housing is faltering.

- Unemployment is rising and the labor market is weakening, which has the propensity to create a self-reenforcing feedback loop.

- Mohamed El-Erian, former chief executive officer at PIMCO, and chief economist at Allianz, also wrote last week “The Fed May Be Two Meetings Away From a Policy Mistake”.

- The Fed is risking a policy mistake by not easing now.

- Waiting will cause undue damage to the economy.

- Pain of higher rates is being concentrated in low income and small businesses.

- The 2.0% inflation target is flawed based on current market dynamics.

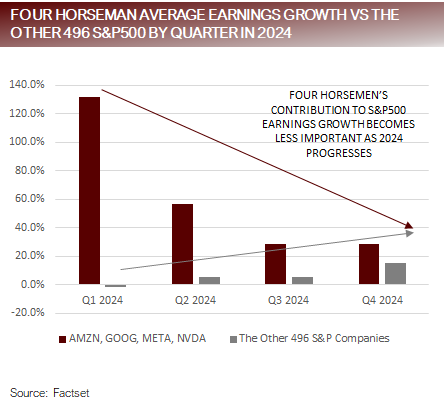

Earnings baton from Magnificent 7 to the rest of the S&P500 in Q4

- Four companies, the Four Horsemen (Nvidia, Amazon, Meta and Alphabet), in the Magnificent 7 are expected to be among the top five contributors to earnings in Q2 (the fifth being Merck).

- The Four Horsemen, are expected to post an average of 4% earning growth year-over-year, and collectively represent 15.8% of the market cap of the S&P500.

- Without the Four Horsemen, the earnings for the S&P500 would be up 7% for the quarter, but that number jumps to 9.7% with their addition.

- This is where it gets even more Each quarter during 2024, the impact of the Four Horsemen is expected to be smaller and smaller. The largest projection for quarterly increase in growth in 2024 for the S&P500 is expected to come in Q4. This means the baton for growth needs to be handed off to some combination of the other 496 stocks for earnings estimates to come to fruition.

For more news, information, and analysis, visit the ETF Building Blocks Channel.