Investors looking to add energy exposure to their portfolios might want to consider the midstream sector as a defensive play against the volatility that ensued in May following a breakdown in the U.S.-China trade deal. Furthermore, a yield-challenged environment from possible rate cuts by the Federal Reserve could spur strategic movements toward yield–something the midstream energy sector could also provide.

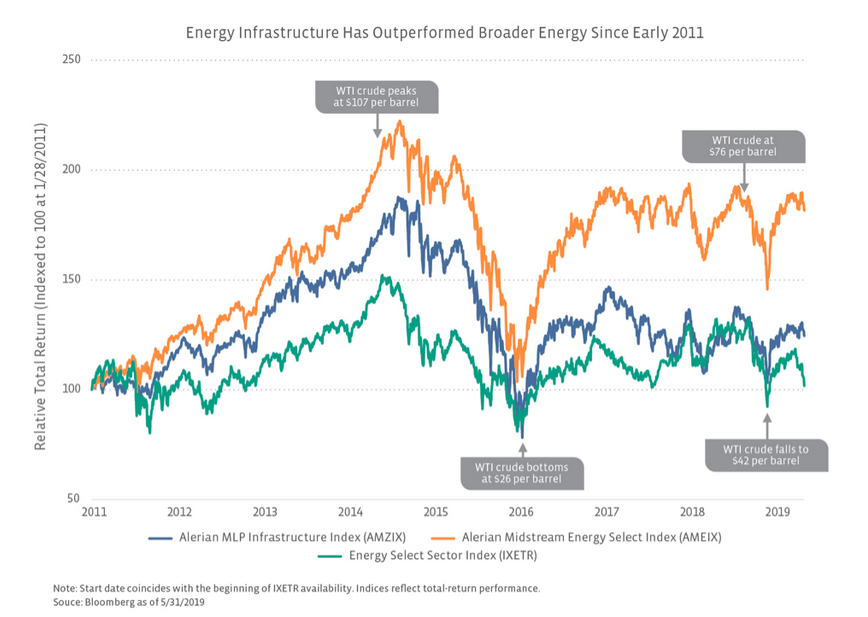

“Midstream has been the relative bright spot in energy despite commodity price volatility,” an Alerian research study noted.

Bottom Line for Investors Seeking Energy Exposure: If comparing midstream products with an investment in the majors like XOM or CVX, or a broader energy product like XLE, there are tradeoffs to consider based on investor preferences or outlooks:

- Yield – Advantage midstream. An MLP or midstream product will typically provide a greater yield than the majors or a broad energy sector product, while still providing energy exposure. Investment in an MLP or MLP-focused product may provide the added benefit of tax-deferred income.

- Concerned about oil prices (prefer defensive investments) – Advantage midstream or majors. Midstream companies are defensive by nature of their business model, but the majors are defensive due to their size, credit quality and consistent dividends.

- Bullish Oil – Advantage energy sector product. Typically, a broad energy index with a heavy weighting towards E&Ps would be expected to outperform midstream in an environment of rising oil prices, though that hasn’t been the case this year. Rising oil prices are likely to be constructive for midstream but more so from a sentiment standpoint than in terms of impacting actual bottom lines. For E&Ps, rising oil prices should more directly benefit revenues and profitability.

- Diversification across energy sectors – Advantage majors or energy sector product. An investment in the majors or an energy sector product will provide greater diversification across the energy value chain.

Exchange-traded funds (ETFs) structured as a partnership are unincorporated business entities so they are not subject to the double taxation of a corporation. If the partnership does not elect to be taxed as a corporation, then it also benefits from pass-through taxation so any realized gains and losses flow directly to investors in the fund.

Partnerships are flexible in terms of the types of investments they can make. Unlike grantor trusts, partnerships can invest in other types of commodities like oil or natural gas due to their flexibility.

However, ETFs structured as a partnership fall under the regulatory measures of the U.S. Commodity Futures Trading Commission. As such, these ETFs are subject to reporting and other financial disclosures.

One specific type of partnership in the ETF world is the MLP.

MLPs are typically classified into three categories:

- Upstream MLPs: involved in the exploration, recovery, development and production of crude oil and natural gas.

- Midstream MLPs: involved in the gathering, processing, storage and transportation of oil and gas.

- Downstream MLPs: involved in the distribution of fuels to end customers such as residential, industrial and agricultural entities.

MLP ETFs, in particular, are gaining traction as their own niche market in the energy sector.

To improve tax efficiency, MLP-related ETFs limit exposure to MLPs to 24% at each quarterly rebalance. Traditional MLP funds that hold more than 25% of their portfolios in MLPs are structured as C-Corporations and must pay corporate income tax on distributions before passing them on to investors, which incurs additional tax headaches come tax season that translates to lower overall returns.

For more market trends, visit ETF Trends.