Summary

- Investors typically allocate to MLPs/midstream in an income portfolio, given generous yields and potential diversification benefits.

- Energy infrastructure can also fit in a real asset sleeve and has typically outperformed in periods of elevated inflation.

- Investors may use energy infrastructure as a more defensive energy sector allocation, as it offers less exposure to oil prices than a broad energy benchmark.

- Given their special tax treatment, MLPs can also be considered alternative investments.

Within portfolios, investors typically use the energy infrastructure space for income. However, midstream is not just a one-trick pony. Investors can also use energy infrastructure for real asset exposure or less volatile energy exposure or as a liquid alternative investment. Because energy infrastructure offers multiple portfolio benefits, investors sometimes struggle with allocation and portfolio placement. This note discusses how advisors have typically allocated to energy infrastructure in portfolios and key considerations.

Income tends to be the most common use case.

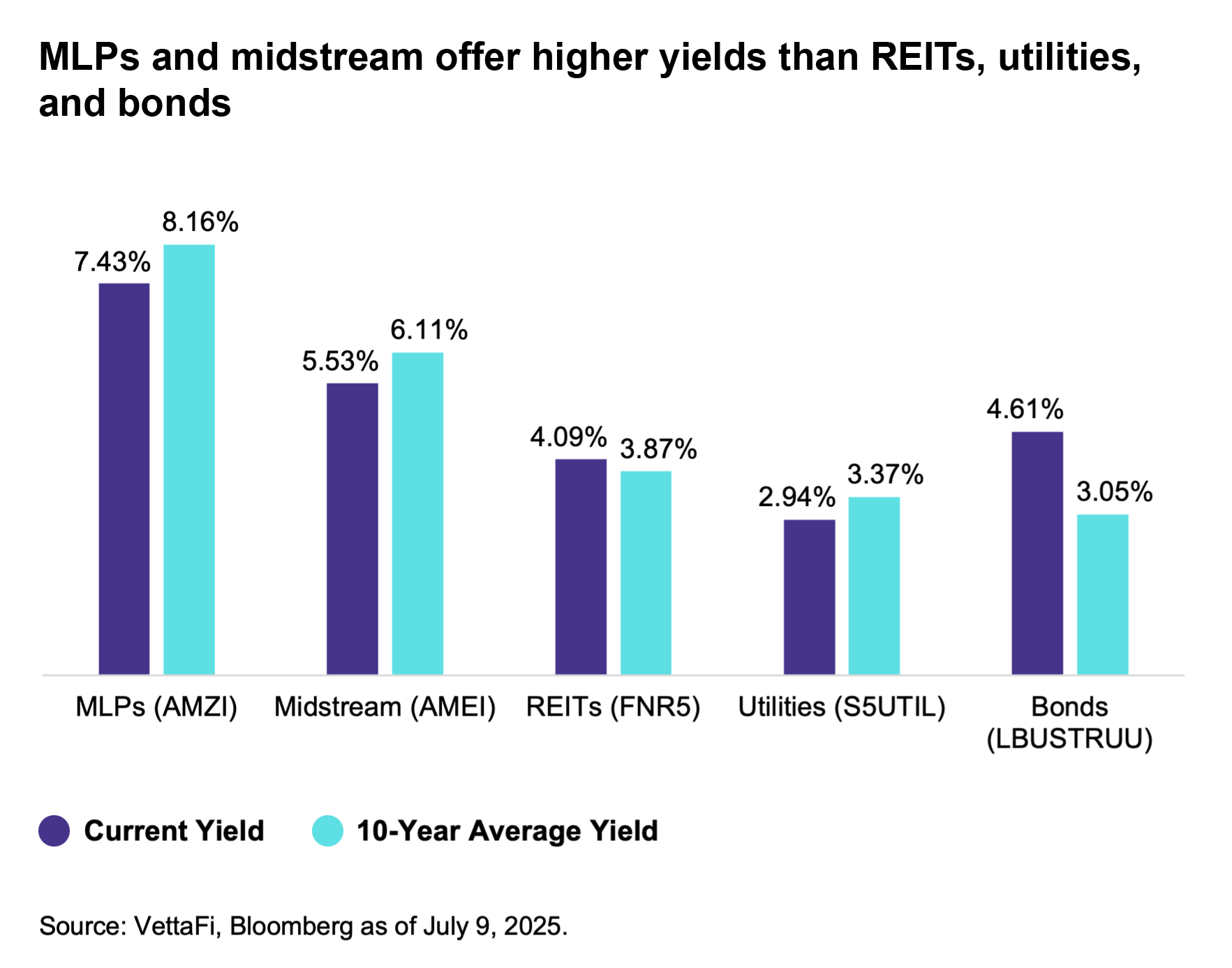

MLPs/midstream tend to be best known for their generous yields. As of July 9, the Alerian MLP Infrastructure Index (AMZI) was yielding 7.4%. The broader Alerian Midstream Energy Select Index (AMEI), which is 75% US and Canadian corporations and 25% MLPs, was yielding 5.5%. As shown below, AMZI and AMEI offer more generous yields than other equity income investments and corporate bonds.

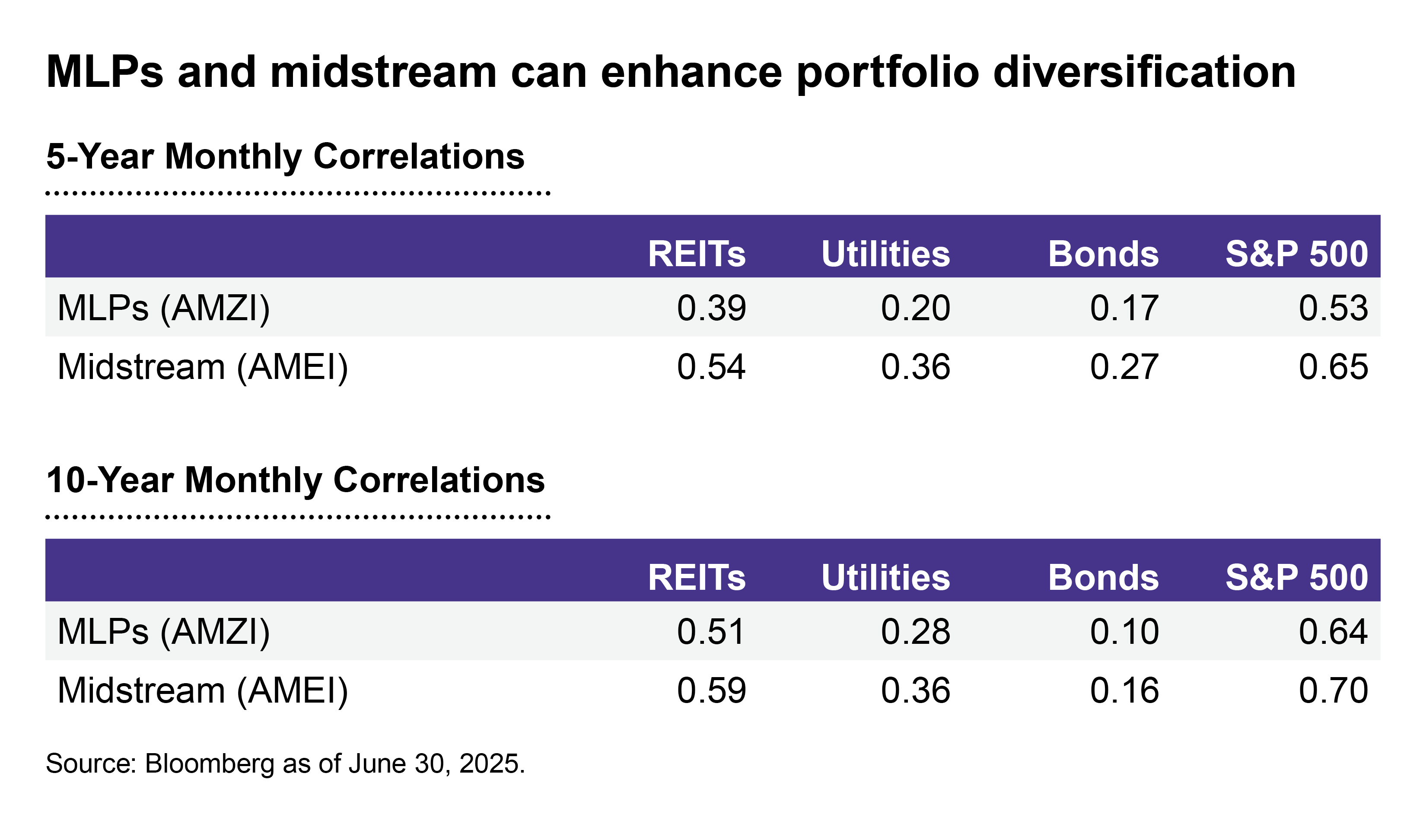

In an income portfolio, energy infrastructure can provide diversification benefits. For example, MLP and midstream yields do not fluctuate with interest rates. Furthermore, MLPs and midstream have modest long-term correlations with bonds, REITs, and utilities as shown. MLPs, in particular, demonstrated lower correlations in the five- and ten-year periods. As a reminder, MLPs are not in broad market indexes like the S&P 500, which can add to their appeal from a diversification standpoint.

How to allocate within an income sleeve.

Within an income portfolio, a typical allocation to energy infrastructure may be around 5%. Investors with a higher risk tolerance or greater income needs may allocate even more to MLPs/midstream, perhaps upwards of 10%.

Investors will typically prefer an allocation to MLPs if they are trying to maximize after-tax yield. A broader midstream investment is generally more suited for total return but still offers solid income. For tax reasons, ETFs or mutual funds predominantly own MLPs or limit MLPs to 25% or less of the holdings (read more). Sometimes investors prefer to own both MLP-focused products and broader midstream products in one portfolio.

Investors are particularly drawn to MLPs for their tax advantages as pass-through entities, including the potential for tax-deferred income (read more). MLPs’ tax advantages come with some complexity, including a Schedule K-1 if investors own individual MLPs directly. Some investors prefer to access the space through an ETF, exchange-traded note (ETN), or mutual fund to avoid receiving a Schedule K-1 and to avoid Unrelated Business Taxable Income (UBTI) for tax-exempt organizations or retirement accounts (read more). Investors should consult with their tax advisors for guidance specific to their situation.

Because of their special tax treatment, MLPs may also reside in the alternatives sleeve of a portfolio. Alternatives tend to have lower correlations with stocks and bonds, which is also true of MLPs as shown above. Note that MLPs will be discussed during VettaFi’s upcoming Alternatives Symposium on July 31 (register here).

Energy infrastructure in a real assets sleeve.

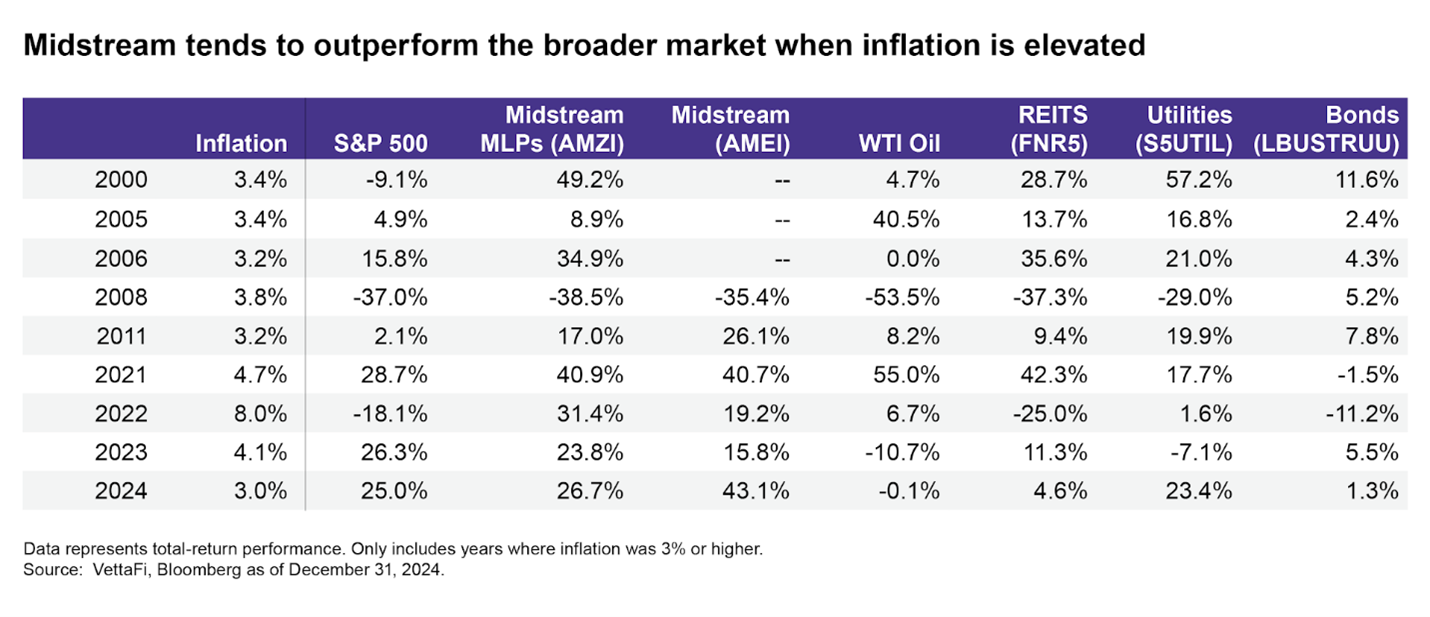

Aside from fitting in an income allocation, investors will often include energy infrastructure in the real asset sleeve of a portfolio. Real assets are typically used as an inflation hedge and tend to outperform when inflation is elevated. Midstream provides liquid real asset exposure as companies own and operate pipelines and other infrastructure. Additionally, midstream contracts tend to have annual inflation escalators (read more).

The table below shows total-return performance in years when US inflation was 3% or higher. AMZI and AMEI generally outperformed both the S&P 500 and bonds in the years shown, with 2008 and 2023 marking exceptions. Aside from 2008, AMZI and AMEI saw strong performance each year.

A more defensive energy allocation.

The other primary way that investors use energy infrastructure is as the energy allocation in an equity portfolio. Relative to a broad energy product, energy infrastructure offers better income and more insulation from oil price volatility. As discussed earlier this month, AMZI and AMEI gained about 7% in 1H25, as oil prices fell 9% and the energy benchmark traded flat (read more).

An investor may put some or all of their energy allocation into energy infrastructure based on energy’s weighting in a benchmark. To give an example, energy was 3.0% of the S&P 500 at the end of June. If an investor prefers more defensive energy exposure and less volatility tied to oil prices, he or she may allocate 3.0% to energy infrastructure in place of a broad energy allocation. Alternatively, an investor could split their energy allocation between MLPs/midstream at 1.5% and a broader energy product at 1.5%.

Bottom line:

Investors often allocate to MLPs/midstream in income portfolios given their yields and potential diversification benefits. However, energy infrastructure can also fit in a real asset or alternative portfolio. Investors may also choose to use MLPs/midstream as the energy exposure in an equities portfolio if looking for more defensive energy exposure or higher yields relative to a broad energy benchmark.

Looking for midstream insights in your inbox? Subscribe here to keep a pulse on midstream investing through our weekly updates.

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the ALPS Alerian Energy Infrastructure Portfolio (ALEFX).

Related Research:

Why Most ‘MLP ETFs’ Own Less Than 25% MLPs

Why Lower Inflation Won’t Rain on MLP/Midstream’s Parade

How to Get MLP Exposure Without a K-1 or UBTI

MLPs and MLP ETFs: Not Just Income, but Tax-Deferred Income

Midstream at Halftime: Defense Wins, Gas in Focus

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP, MLPB, ENFR, and ALEFX, for which it receives an index licensing fee. However, AMLP, MLPB, ENFR, and ALEFX are not issued, sponsored, endorsed, or sold by VettaFi. VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP, MLPB, ENFR, and ALEFX.