Summary

- Refineries convert crude oil into essential products, primarily transportation fuels like gasoline and diesel.

- California refining capacity has been shrinking for decades, with a challenging operating environment and emphasis on clean fuels driving plant closures or conversions to renewable fuel production.

- A product supply shortfall is creating a major opportunity for new midstream pipelines designed to transport refined products from Texas to meet demand in California and other Western states.

As of late, newbuild pipeline projects and major expansions have generally centered around natural gas or natural gas liquids. However, pipelines that move refined products (gasoline, diesel, jet fuel) have been in the spotlight lately, as California refinery closures require additional volumes of gasoline and diesel to move west. Learn how the changing landscape in California is creating new growth opportunities for refined product pipelines and the midstream companies involved.

What Refineries Make and Why It Matters

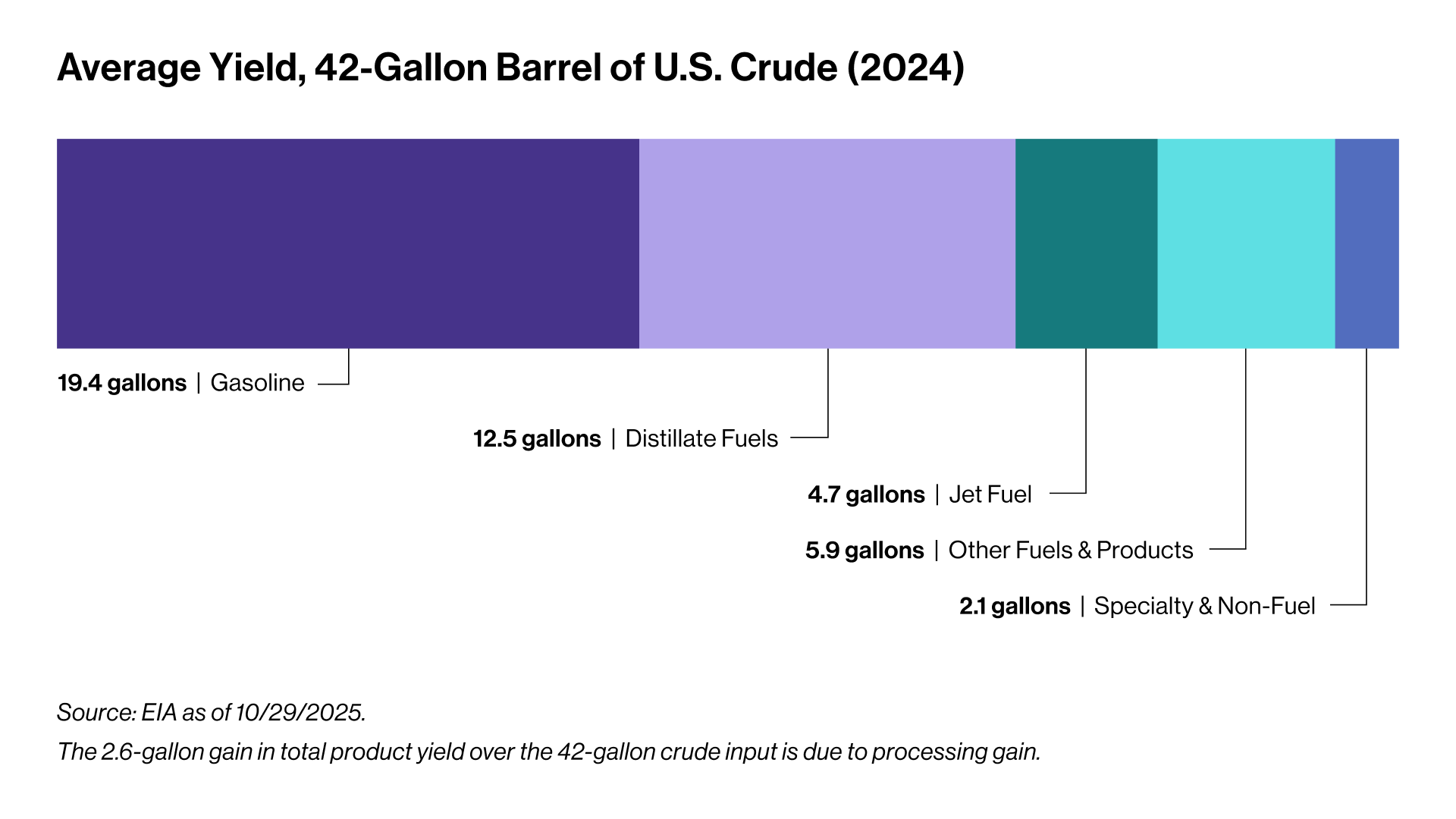

Refineries convert crude oil into various refined products. These include gasoline, diesel fuel, heating oil, jet fuel, feedstocks for the petrochemical industry (like naphtha), and other products (including asphalt and lubricating oils). According to data for 2024 from the Energy Information Administration (EIA), gasoline accounted for 46.1% of U.S. refinery yield, followed by distillate fuels (diesel and heating oil) at 29.7% and jet fuel at 11.1%.

According to EIA data for the 12 months ending July 2025, the U.S. consumed an average of 20.6 million barrels per day (MMBpd) of refined products. The transportation sector dominated this demand, accounting for 67.9% of all consumption, followed by industrial demand at 27.3%. The U.S. has 132 operable refineries as of January 2025 with a total capacity of 18.4 MMBpd, making the U.S. reliant on imports to fill the gap particularly on the East Coast and West Coast.

According to EIA data for the 12 months ending July 2025, the U.S. consumed an average of 20.6 million barrels per day (MMBpd) of refined products. The transportation sector dominated this demand, accounting for 67.9% of all consumption, followed by industrial demand at 27.3%. The U.S. has 132 operable refineries as of January 2025 with a total capacity of 18.4 MMBpd, making the U.S. reliant on imports to fill the gap particularly on the East Coast and West Coast.

California’s Dwindling Refining Capacity

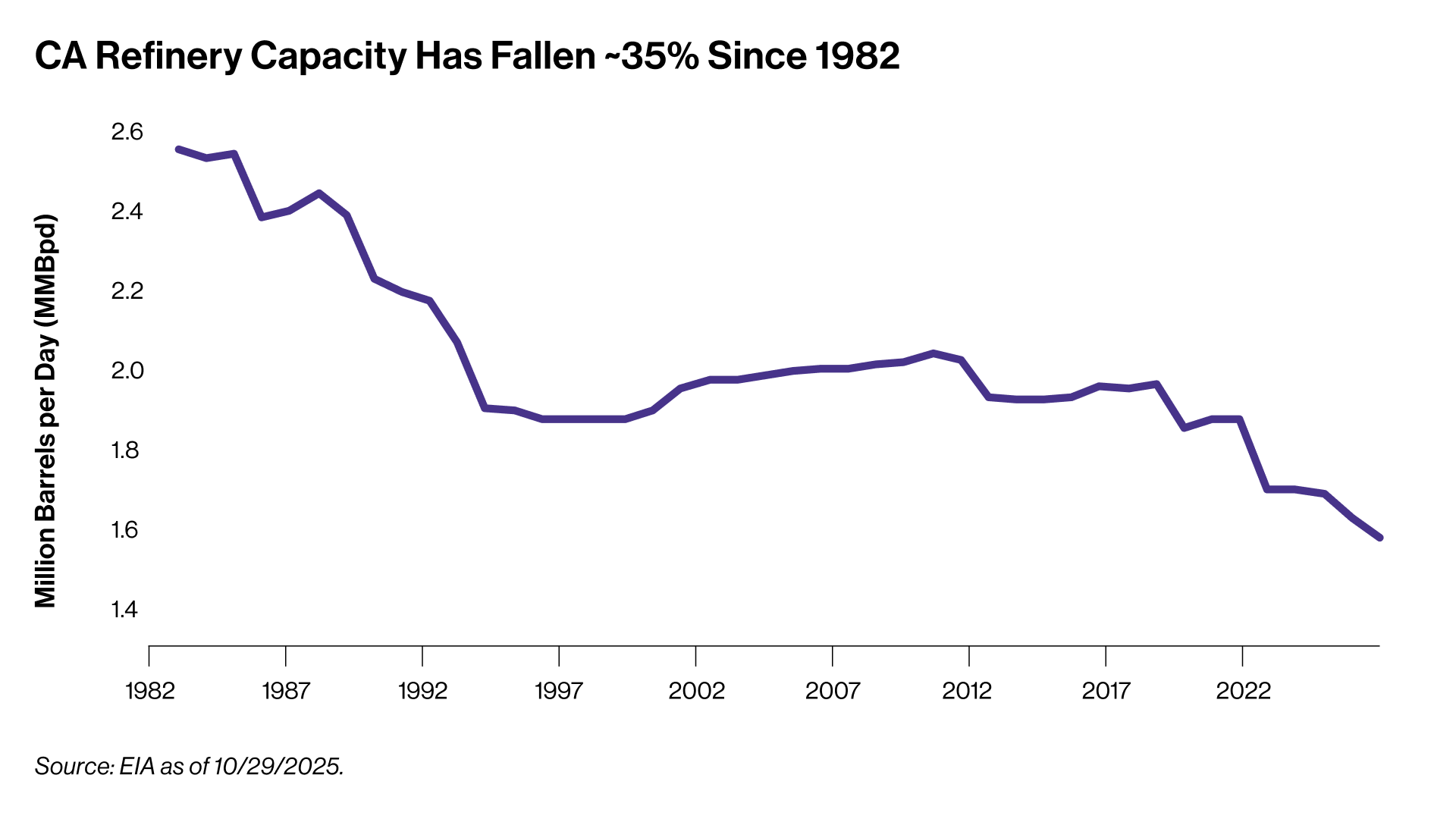

While perhaps hard to believe now, California was once a major oil producing state, with output above 1 MMBpd in the 1980’s compared to current production of 250 thousand barrels per day (MBpd). California was also home to significant refining capacity in its heydays of oil production. However, between 1982 and 2020, the state lost 28 refineries and ~625 MBpd of capacity. By early 2025, total capacity had fallen by another ~270 MBpd, bringing the total decline to ~35% below 1982 levels, as major plants began idling crude oil processing.

For many years, California has been a challenging environment for refiners, given tough regulations and unique fuel requirements that contribute to higher operating costs. California’s Low-Carbon Fuel Standard (LCFS), which aims to cut the carbon intensity of transport fuels, creates significant headwinds for traditional refining margins. California also requires a special, cleaner-burning gasoline called CARBOB, which is more complex to produce and can only be sourced from a limited number of refineries globally.

For many years, California has been a challenging environment for refiners, given tough regulations and unique fuel requirements that contribute to higher operating costs. California’s Low-Carbon Fuel Standard (LCFS), which aims to cut the carbon intensity of transport fuels, creates significant headwinds for traditional refining margins. California also requires a special, cleaner-burning gasoline called CARBOB, which is more complex to produce and can only be sourced from a limited number of refineries globally.

California regulations have largely pushed for electric vehicles and cleaner fuels. With this backdrop, traditional refineries have converted to renewable fuel facilities, including Marathon Petroleum’s (MPC) Martinez and Phillips 66’s (PSX) Rodeo refinery. Two more refineries are set to shut down by mid-2026, representing 284 MBpd of total capacity or ~17% of state capacity (PSX’s Wilmington and Valero’s Benicia).

California’s petroleum demand in 2023 averaged 1.78 MMBpd, while total refining capacity at the beginning of 2025 was 1.64 MMBpd (refineries do not operate at full capacity). This gap in local product supply forces California to rely more on imports, likely sourced from Asia. Shrinking supply not only leaves California vulnerable to price spikes, but has also created a shortfall for Nevada and Arizona, which also require a unique gasoline blend. Both states historically relied on California’s refineries. As a result, all three states now need to source refined products from the Mid-Continent or the Gulf Coast.

New Product Pipelines Target the West Coast

With California product supply set to continue falling, midstream companies are proposing new pipeline projects to supply western states. Today, California is not connected to the nation’s primary refining centers. Historically, pipelines moved surplus fuel out of California, but that dynamic is set to reverse.

On October 20, Kinder Morgan (KMI) and PSX announced a binding open season for their proposed Western Gateway Pipeline project, which will connect Texas with California. The open season, which ends December 19, is a period for gauging customer interest and securing long-term contracts. If the partners proceed, the system could be online in 2029.

Western Gateway consists of a new-build pipeline from PSX’s Borger refinery in the Texas panhandle to Phoenix, and the reversal of KMI’s existing SFPP pipeline that currently flows out of California to Phoenix. The project also includes reversing PSX’s Gold Pipeline to bring Mid-Continent refinery supply from the St. Louis area to Borger to feed Western Gateway. The system will also connect to Las Vegas through KMI’s existing CALNEV pipeline. The partners would jointly own the system, with PSX contributing more capital due to KMI’s contribution of its SFPP pipeline.

As context, PSX announced that it was buying out its 50-50 partner in the Borger and Wood River refineries in September. Wood River (near St. Louis) and PSX’s other Mid-Con refineries can produce Arizona and California gasoline. PSX sees strategic value in moving product from the Mid-Con to premium West Coast markets and the likely margin uplift available. On their earnings call, PSX management was confident Western Gateway would proceed.

Meanwhile, ONEOK (OKE) is holding a binding open season for its proposed Sunbelt Connector through November 7. This project involves constructing ~440 miles of new pipeline from El Paso, Texas, to Phoenix. It will facilitate long-haul movements of gasoline, diesel, and jet fuel to destinations including El Paso and Phoenix from the Houston area and southern Oklahoma. If greenlit, the project could be operational by mid-to-late 2029. On their earnings call last week, OKE management indicated that they would be open to adding a strategic partner to the project.

While Western Gateway and Sunbelt Connector have different origins, they are competing to move refined product west. It is possible that both proceed and are needed to meet product demand. An advantage of Western Gateway is that PSX as a refiner partner can help fill the pipelines.

Bottom Line

A significant decline in California’s refining capacity is poised to create a supply shortfall on the West Coast. This has created a major opportunity for midstream companies to develop new pipelines connecting Gulf Coast and Mid-Con refiners to Western markets.

For an informative 30-minute discussion with Energy Transfer (ET), don’t miss our webcast on Wednesday, November 12, at 12:30 p.m. ET. Follow the link here to register.

Looking for midstream insights in your inbox? Subscribe here to keep a pulse on midstream investing through our weekly updates.

Related Research

Kinder Morgan Q3 Results Buoyed by Robust Growth Outlook

It’s July 1 & US Liquids Pipelines Are Raising Rates

The Outlook for U.S. Energy Production & Midstream Impact

Pipelines Set to Expand Amid Successful Open Seasons

Gasoline Prices and How Midstream Helps Fill Your Tank

For more news, information, and analysis, visit the Energy Infrastructure Content Hub.