Key Takeaways:

- On a year-over-year basis, 96.0% of the Alerian Midstream Energy Index (AMNA) by weighting have grown their dividends.

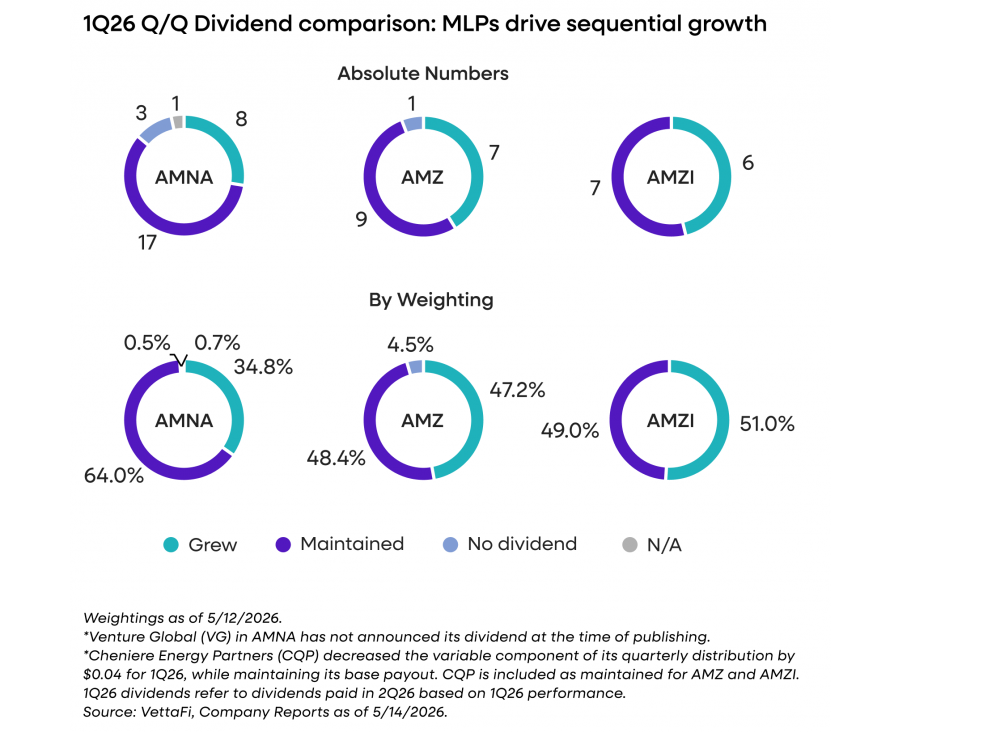

- MLPs largely drove sequential growth in payouts for 1Q26, while most corporations kept their dividends

steady. No AMNA constituent has cut its regular dividend since July 2021. - Midstream indexes have seen a strong 2026 thus far, generating robust total returns of over 20% year-to-

date through May 15 that handily outpace the broader market.

For the first quarter of 2026, most of the constituents in the broad Alerian Midstream Energy Index (AMNA) maintained their payouts, with a handful of MLPs and select C-Corps providing sequential growth. The vast majority of midstream companies have increased their dividends within the last year, with further growth expected this year. Learn more below about 1Q26 MLP/midstream dividends and why dividend growth is just one of multiple tailwinds for this space.

1Q26 Payouts: Notable Increases From MLPs & C-Corps

Dividend announcements for 1Q26 included increases from steady growers, as well as a few notable hikes from names that typically increase their payouts once a year. The largest sequential percentage increase was from C-Corp Targa Resources (TRGP), which raised its dividend by 25% to $1.25 per share, consistent with management’s guidance from November 2025. Notably, DT Midstream (DTM) increased its 1Q26 dividend by 7.3% as announced in February. Pembina (PPL CN) and Kinder Morgan (KMI), which typically raise their payouts annually for the first quarter, increased their dividends by 3.5% and 1.7%, respectively.

Sunoco (SUN) had one of the more notable increases among MLPs for 1Q26, raising its quarterly distribution by 6.25% sequentially. The increase, comprising a one-time 5% step-up and a 1.25% quarterly increase, aligns with the company’s target of at least 5% multi-year distribution growth. Besides SUN, other sequential increases came from MLPs with a track record of growing their payout each quarter: Energy Transfer (ET), Hess Midstream (HESM), Global Partners (GLP), and Delek Logistics Partners (DKL). Western Midstream (WES) grew its payout 2.2% and Star Group, which is only in the Alerian MLP Index (AMZ), increased by 6.8%.

The pie charts below show quarter-over-quarter changes to dividends for AMNA, AMZ, and the Alerian MLP Infrastructure Index (AMZI) by comparing 1Q26 payouts to those made for 4Q25. To be clear, 1Q26 dividends refer to dividends paid in 2Q26 based on operational performance in 1Q26.

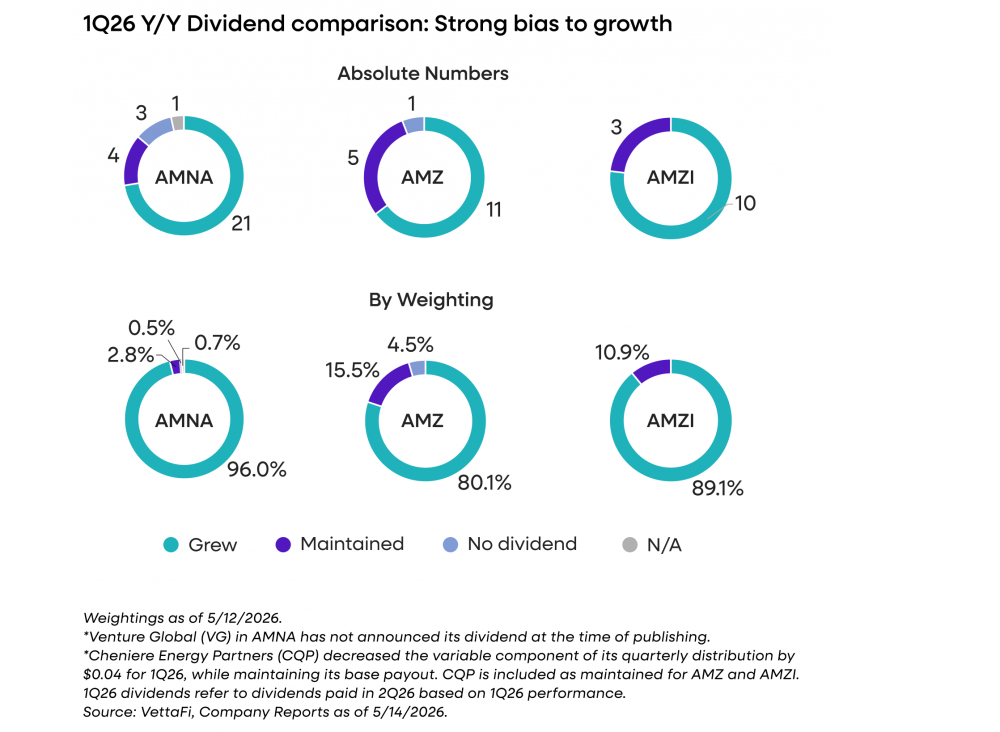

Year-Over-Year Comparison Highlights Widespread Dividend Growth

Year-Over-Year Comparison Highlights Widespread Dividend Growth

With many companies only increasing their payouts once each year, a year-over-year comparison can provide a clearer picture of dividend trends. The pie charts below show a clear bias towards rising payouts. Over 80% of AMZ and almost 90% of AMZI by weighting have increased their distributions within the last year. For AMNA, 96.0% of the index by weighting has grown payouts relative to 1Q25. Looking at the absolute numbers, the majority of constituents in each index have grown their dividends.

Midstream companies that prefer annual hikes typically make those announcements for 4Q or 1Q payouts. That could lead to a quieter 2Q26; however, companies are expected to continue prioritizing dividend growth. MPLX (MPLX) management expects to continue 12.5% annual distribution growth for 2026 and 2027. Cheniere (LNG) is committed to growing dividends by ~10% annually through the end of the decade. Additionally, both Hess Midstream (HESM) and Sunoco (SUN) are targeting multi-year distribution growth of at least 5% annually, with HESM’s outlook extending through 2028. EBITDA growth (read more) and ongoing free cash flow generation (read more) continue to drive a constructive outlook for midstream/MLP payouts.

Midstream companies that prefer annual hikes typically make those announcements for 4Q or 1Q payouts. That could lead to a quieter 2Q26; however, companies are expected to continue prioritizing dividend growth. MPLX (MPLX) management expects to continue 12.5% annual distribution growth for 2026 and 2027. Cheniere (LNG) is committed to growing dividends by ~10% annually through the end of the decade. Additionally, both Hess Midstream (HESM) and Sunoco (SUN) are targeting multi-year distribution growth of at least 5% annually, with HESM’s outlook extending through 2028. EBITDA growth (read more) and ongoing free cash flow generation (read more) continue to drive a constructive outlook for midstream/MLP payouts.

Midstream/MLPs Enjoying Strong Performance in 2026

Dividend growth has been just one tailwind for the midstream/MLP space this year. Energy equities have seen broad strength with oil prices rallying and ongoing supply disruptions in the Middle East. Midstream also continues to benefit from the tailwinds related to growing natural gas demand in North America, with companies enjoying robust opportunities for natural gas infrastructure. The space broadly saw a strong 1Q26 earnings season, with many companies beating expectations and raising their financial guidance for the year.

Year-to-date through May 15, AMNA has gained 27.6%, AMZ has gained 25.1%, and AMZI is up 25.0% on a total-return basis. Even with these gains, yields remain healthy, particularly for the MLP indexes AMZ and AMZI. As of May 15, AMZ and AMZI were yielding 6.4% and 6.8% respectively, while AMNA was yielding 4.2%. Energy infrastructure’s capital appreciation, paired with the compelling, stable income it provides, has delivered robust returns so far this year.

Bottom Line

Midstream/MLP dividend growth remains a reliable tailwind, reinforced by 1Q26 announcements. Consistent dividend growth supports generous yields and provides attractive returns for investors. Complementing this payout growth are equity repurchases, which will be discussed in detail next week. Stay tuned.

Looking for midstream insights in your inbox? Subscribe here to keep a pulse on midstream investing through our weekly updates.

For more news, information, and analysis, visit the Energy Infrastructure Content Hub

Related Research:

Broad-Based Growth in 4Q25 Midstream/MLP Dividends

2026 EBITDA Guidance Reinforces Midstream Stability

3Q25 Midstream/MLP Dividends: Payouts Stay Strong

Breaking Down MLP Distribution Outlooks With AMZI

Midstream/MLP Free Cash Flow Yields Still Strong

2Q25 MLP/Midstream Dividend Recap: MLPs Deliver Growth

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMZ is the underlying index for the JPMCFC Alerian MLP Index ETN (AMJB), the ETRACS Alerian MLP Index ETN Series B (AMUB), and the ETRACS Quarterly Pay 1.5x Leveraged Alerian MLP Index ETN (MLPR).

vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMJB, AMUB, MLPR, AMLP, and MLPB, for which it receives an index licensing fee. However, AMJB, AMUB, MLPR, AMLP, and MLPB are not issued, sponsored, endorsed or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing or trading of AMJB, AMUB, MLPR, AMLP, and MLPB.