Summary

- Midstream MLPs and C-Corps have been growing their payouts in recent years, supported by free cash flow generation and EBITDA growth.

- Several midstream companies have either provided guidance for 2025 dividends, announced increases, or given long-term forecasts for dividend growth.

- Rising payouts enhance MLP/midstream yields, which remain attractive relative to other income investments.

Energy infrastructure is known for its attractive income backed by fee-based businesses with stable cash flows, and dividend growth is a key priority for many companies. Free cash flow generation and EBITDA growth have helped support rising payouts. Today’s note looks at 2025 and long-term dividend guidance, as well as current yields.

To learn more about the 2025 outlook, please join us tomorrow, at 1 p.m. EST for our webcast, “After a Strong 2024, Do MLPs/Midstream Have More in the Tank?” Register here.

Midstream Dividend Growth as a Multiyear Tailwind

Energy infrastructure companies have been consistently growing their dividends in recent years, with the majority of names in benchmark indexes increasing their payouts year-over year (read more). Dividend growth has been supported by widespread free cash flow generation (read more), as well as continued EBITDA growth from fee-based businesses with steady cash flows.

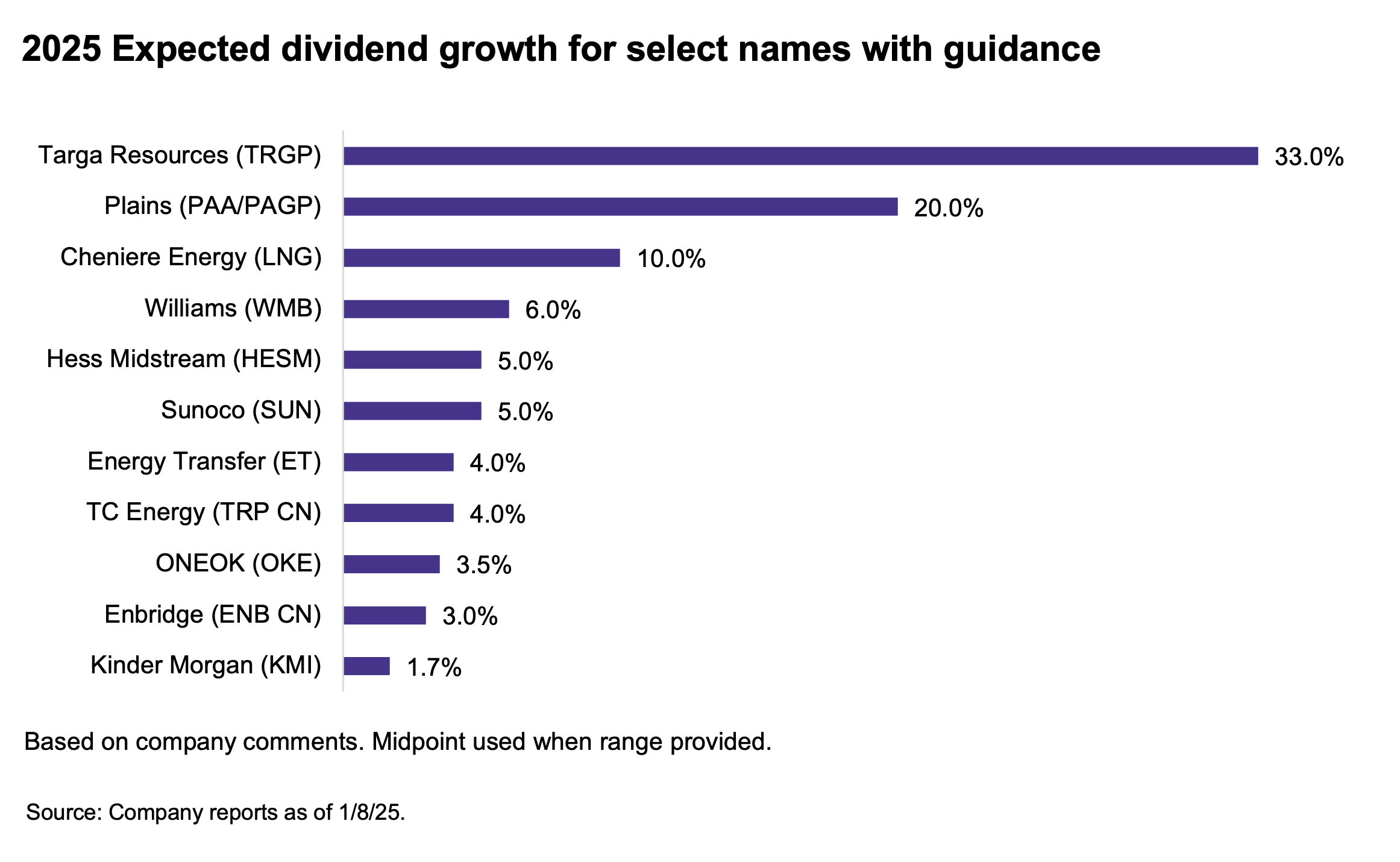

Several midstream companies have either provided guidance for 2025 dividends or already announced increases. Others have given long-term growth targets for their payouts. The chart below reflects expected 2025 dividend growth based on guidance or announced payouts. Note that dividend growth is widely expected, but the chart only includes companies with specific guidance. Companies may also provide more color around expected dividend growth during fourth quarter earnings season.

Companies are mostly expecting moderate dividend growth with a few exceptions. Namely, Targa Resources (TRGP) and Plains All American (PAA/PAGP) stand out for more significant growth. Both cut their payouts back in 2020, which helps explain the larger percentage increases. TRGP plans to recommend to its board a 33.0% increase to its dividend in 2025 as announced in November. The proposed increase for 2025 would take TRGP’s quarterly payout above where it was back in 2019. Last week, Plains All American (PAA) announced a 20% increase to its distribution (up $0.25 per unit annually), which was above its guidance for a $0.15/unit annual increase (read more). PAA’s quarterly distribution now exceeds 2019 levels.

Specific to 2025, Enbridge (ENB CN) already announced a 3% increase to its March payout. Kinder Morgan (KMI) plans to pay an annual dividend of $1.17 per share, which represents a 1.7% increase relative to 2024. Sunoco (SUN) is targeting 5% growth this year with quarterly increases.

Two companies are not included in the chart but bear mentioning. Last week, Enterprise Products Partners (EPD) raised its distribution by 1.9% sequentially or 3.9% relative to the same quarter last year. In recent years, EPD has raised its distribution at the start of the year and again in the middle of the year but has not provided specific guidance. On its November earnings call, the management of MPLX (MPLX) discussed the durability of the 12.5% annual distribution increase announced in late October 2024, noting that 12.5% growth is very doable for a period of time.

Long-term Targets Reinforce Expectations for Moderate Growth

Several midstream names have long-term targets for dividend growth. Long-term guidance provides helpful visibility to investors and represents a clear goal for management teams to execute against. Dividend growth expectations can align with or be informed by anticipated growth in fee-based EBITDA. (See next week’s note for more on EBITDA growth guidance.)

Most long-term targets tend to be around mid-single-digit percentages: ONEOK (OKE) at 3-4%, Energy Transfer (ET) at 3-5%, and TC Energy (TRP CN) at 3-5%. Hess Midstream (HESM) has guided to at least 5% growth through 2026 but has generally exceeded its target (read more). On the higher end, Cheniere (LNG) plans to grow its dividend by ~10% annually through the end of this decade as discussed on its last earnings call. Cheniere initiated a dividend in late 2021.

Midstream Yields Remain Attractive

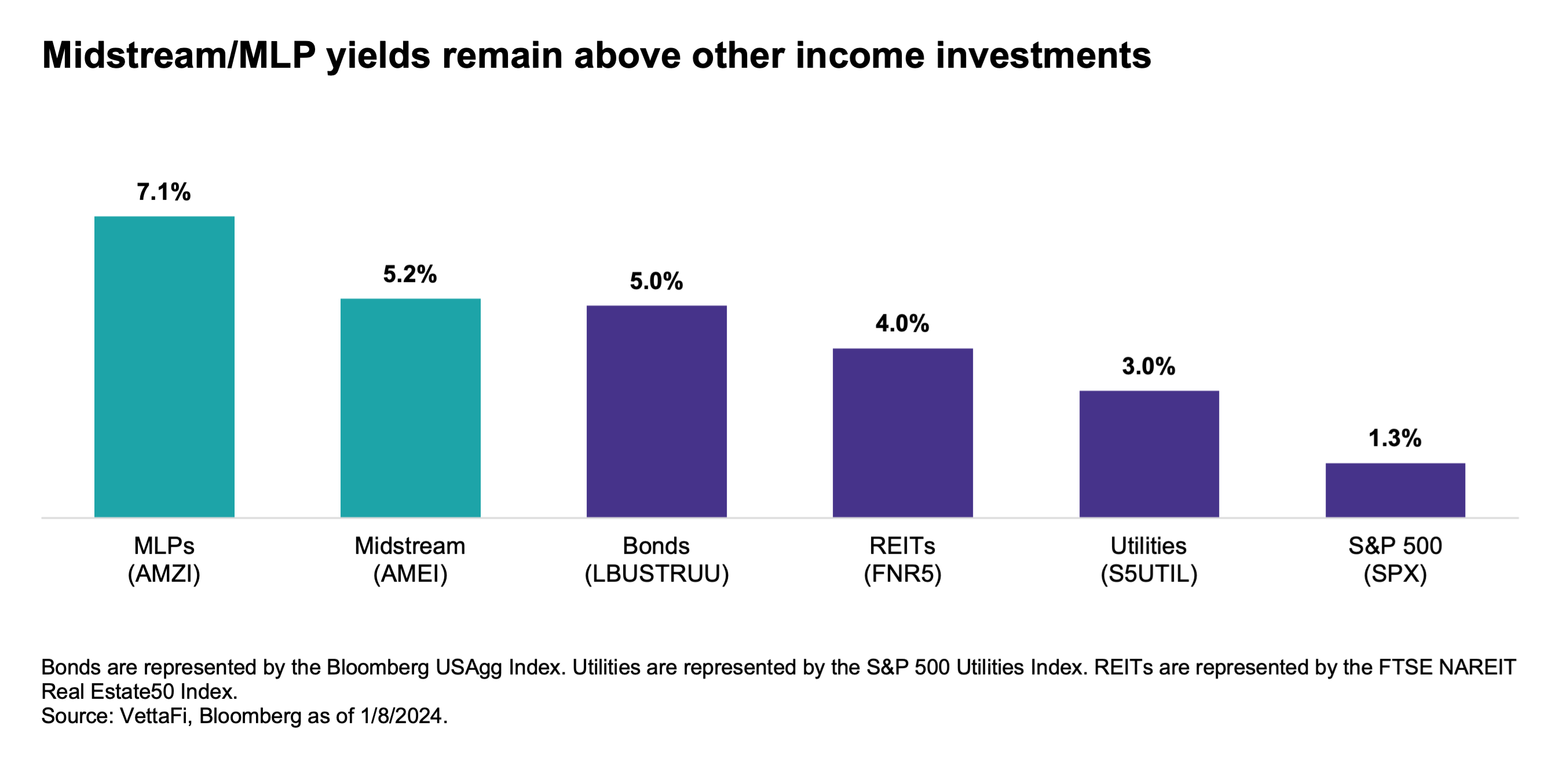

For midstream investors, dividend growth enhances what are already attractive yields relative to many equity income categories. These include REITs and utilities. The chart below shows current yields for MLPs and broader midstream relative to other popular income investments. MLPs are represented by the Alerian MLP Infrastructure Index (AMZI), and midstream is represented by the Alerian Midstream Energy Select Index (AMEI), which is 75% U.S. and Canadian C-Corps and 25% MLPs. Strong dividend track records and expected growth in payouts add confidence to MLP/midstream yields.

Bottom Line

Most midstream companies are expected to continue delivering dividend growth in 2025 and beyond. Guidance for 2025 and multiyear periods provide helpful visibility to investors and add to confidence in midstream payouts.

AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the Alerian Energy Infrastructure Portfolio (ALEFX).

Related Research:

3Q24: Another Strong Quarter for Midstream/MLP Payouts

Hess Midstream CFO: Growth Opportunities, Balance Sheet Strength & Shareholder Returns

Plains CCO Discusses Permian Outlook & Capital Allocation Priorities

Midstream/MLPs See Sustained Free Cash Flow

Vettafi.com is owned by VettaFi LLC (“VettaFi”). VettaFi is the index provider for AMLP, MLPB, ENFR and ALEFX, for which it receives an index licensing fee. However, AMLP, MLPB, ENFR and ALEFX are not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of AMLP, MLPB, ENFR and ALEFX.

For more news information and analysis, visit the Energy Infrastructure Channel.