By Stacey Morris, CFA, and Philip Segal

Summary

- Even though midstream capital spending has moderated and reliance on debt has eased somewhat, credit ratings are still important for energy infrastructure companies.

- By weighting, investment-grade names make up the bulk of Alerian energy infrastructure indexes.

- Energy infrastructure indexes, particularly the MLP indexes, are providing yields that are competitive with junk bonds, but the midstream income is coming from companies with much higher credit quality.

The midstream space has had a good year, as the broader energy sector has led gains in an overall challenging market. Resilient against elevated inflation and volatile oil prices, energy infrastructure companies have been executing well, with free cash flow generation fueling buybacks and dividend growth. Given a supportive macro backdrop and company-level tailwinds, the financial health of the midstream space has been more of an afterthought. Admittedly, it has been more than two years since we last detailed midstream/MLP credit ratings. This note provides an updated look at credit ratings at the company and index level using the Alerian energy infrastructure index suite.

Why do investment-grade credit ratings matter for midstream?

Midstream companies are arguably less dependent on debt financing than in the past. As detailed in this note from July 2022, the decline in capex from 2019 to 2021 can be measured in billions of dollars for the largest names in this space. Furthermore, many companies have used excess cash flow to reduce debt, and leverage metrics have improved over recent years (read more). Even though midstream capital spending has moderated and reliance on debt has eased somewhat, credit ratings are still important for energy infrastructure companies.

An investment-grade credit rating allows companies better access to debt markets and allows them to receive more favorable rates. A lower cost of debt saves money and allows for better returns on growth projects. The lower rates for investment-grade companies are perhaps a more notable advantage in today’s higher interest rate environment. For example, the yield difference between an investment-grade corporate bond benchmark and a high-yield benchmark was 420 basis points as of December 16, 2022. For full-year 2021, the average yield spread between the investment-grade and high-yield index was just 260 basis points. Companies continue to prioritize maintaining investment grade metrics, with Plains All American’s (PAA) and Cheniere’s (LNG) capital allocation frameworks from this fall including goals related to maintaining investment-grade credit ratings (read more).

Larger midstream players tend to have stronger credit ratings.

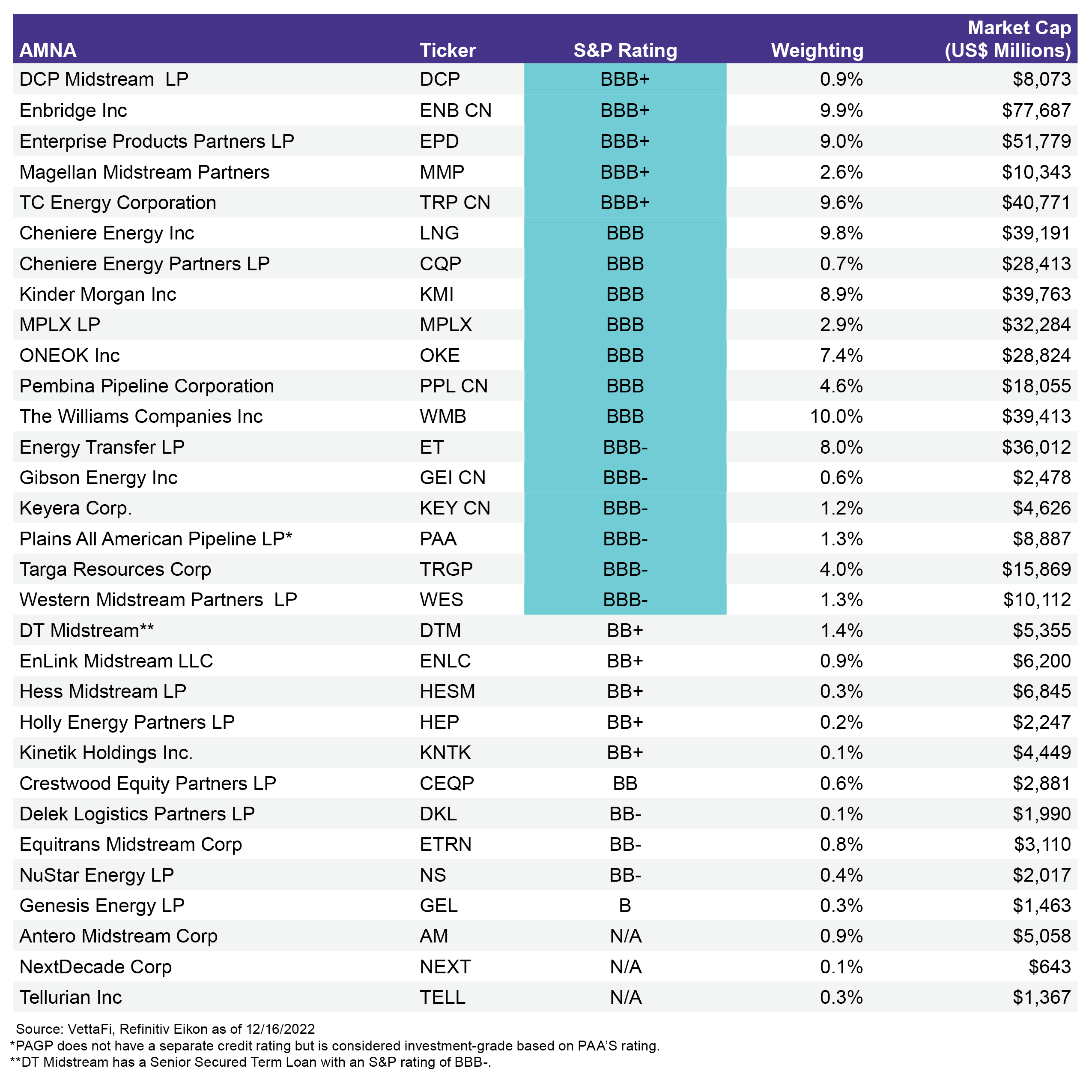

Looking at company-level credit ratings from S&P, larger names in the space tend to have stronger ratings. The appendix to this note includes a table showing credit ratings for the constituents of the Alerian Midstream Energy Index (AMNA). Of the 32 names in the index, 19 of those have investment grade credit ratings from S&P (BBB- or better, including PAGP as noted below). Of the investment-grade names, the average market cap is over $27 billion, while the average market cap of AMNA constituents that have lower than investment grade, or no S&P credit rating, is between $3.3-$3.7 billion.

Looking at investment-grade weightings at the index level.

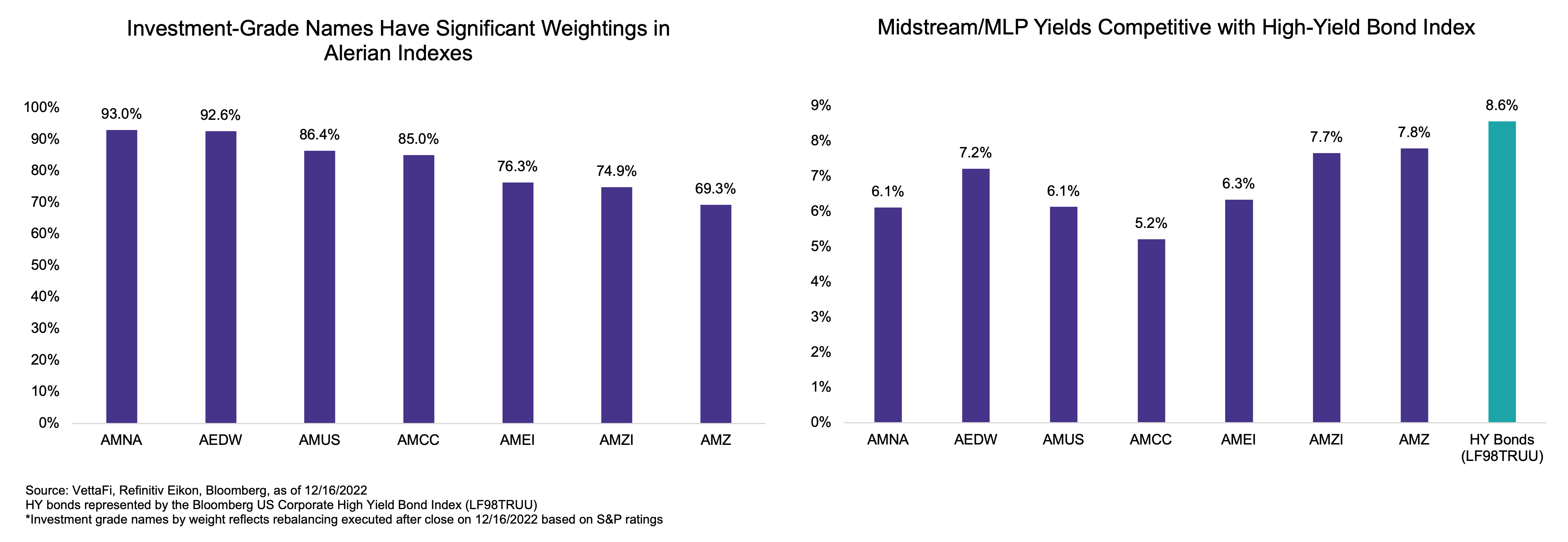

By weighting, investment-grade names make up the bulk of Alerian energy infrastructure indexes. The larger companies that tend to have healthier balance sheets also typically have greater weightings in the Alerian indexes given weights are based on float-adjusted market cap. The dividend-weighted Alerian Midstream Energy Dividend Index (AEDW) is an exception to this. Of note, all the indexes shown in the charts below have a 10% cap on individual names. Generally, midstream indexes that include corporations tend to have a higher weighting toward investment-grade companies, with AMNA having the greatest investment-grade weighting at 93.0% followed by AEDW at 92.6%. The Alerian US Midstream Energy Index (AMUS), which only includes US-based MLPs and C-Corps, comes in third at 86.4%. Meanwhile, the investment-grade weighting for the Alerian MLP Infrastructure Index (AMZI) and Alerian MLP Index (AMZ) is lower at 74.9% and 69.3%, respectively.

{kind=link}

Looking at index yields alongside investment-grade weightings provides interesting context. In general, indexes with higher investment-grade weightings tend to have lower yields, which relates to MLPs typically providing greater yields than their C-Corp counterparts. The dividend-weighting scheme for AEDW results in the highest yield among the indexes with MLPs and corporations. Also notable, energy infrastructure indexes, particularly the MLP indexes, are providing yields that are competitive with junk bonds represented by the Bloomberg US Corporate High Yield Bond index (LF98TRUU) in the chart above, but the midstream/MLP income is coming from companies with much higher credit quality. It also bears highlighting that MLPs provide the potential for tax-deferred income, with MLP-focused ETFs replicating those advantages (read more).

Bottom Line

Although less dependent on debt financing than in the past, an investment grade credit rating is still desirable to midstream companies. The better the credit rating, the easier it becomes to access debt markets as well as receive more favorable rates. In short, companies want to pay as little as possible to borrow money. The Alerian energy infrastructure indexes generally lean toward investment-grade names by weighting while providing yields competitive with much riskier assets.

AMNA is the underlying index for the ETRACS Alerian Midstream Energy Index ETN (AMNA). AMZI is the underlying index for the Alerian MLP ETF (AMLP) and the ETRACS Alerian MLP Infrastructure Index ETN Series B (MLPB). AMEI is the underlying index for the Alerian Energy Infrastructure ETF (ENFR) and the ALPS Alerian Energy Infrastructure Portfolio (ALEFX). AEDW is the underlying index for the Alerian Midstream Energy Dividend UCITS ETF (MMLP) and the ETRACS Alerian Midstream Energy High Dividend Index ETN (AMND). AMZ is the underlying index for the JP Morgan Alerian MLP Index ETN (AMJ) and the ETRACS Quarterly Pay 1.5x Leveraged Alerian MLP Index ETN (MLPR).

Related Research:

Midstream/MLPs: The Benefits of Capital Allocation Frameworks

Midstream/MLPs: Leveled Up with Leverage Down

Midstream/MLPs: Free Cash Flow Powerhouse

Beyond the K-1: Tax Treatment for an MLP Fund vs. an MLP

Appendix

{kind=link}