Emerging market ETFs are coming off their best weekly showing in about a year. Both broad-based and country-specific ETFs tied to developing nations enjoyed their best stretch of inflows since December 2023 — to the tune of $6 billion.

In the third quarter, many emerging market ETFs also racked up triple-digit gains or more on a total return basis. But a closer look at recent flows reveals a growing discernment among advisors and investors.

China Moves Are Changing the Game

China’s fresh slate of stimulus has lit a fire under China-focused equity ETFs since late September. Some of the initial fervor has waned due to a lack of clarity on policy specifics this week. But the story remains the same. Chinese stocks have ricocheted back to become the single best-performing global stock market in 2024. The Hang Seng index has surged 30% year to date. It’s now hovering more than 40% above its January low.

China ETFs have collectively suffered outflows of roughly $4 billion this year. And ex-China ETFs have consistently topped the flow charts, boasting $8 billion in inflows for the year. But the PBoC’s aggressive roll-out of targeted fiscal and monetary policy promises has thrown a wrench into the emerging market equation. The off-cycle timing and nature of the announcements were also hard to ignore. The central bank vowed to attack the housing market collapse head-on. It also announced lower reserve requirements for capital banks and fresh injections of stimulus for China’s stock market.

India ETFs continue to dominate EM flows with $5 billion in inflows year to date. But the pace of new money pouring into China ETFs has ramped up over the past week. China equity ETFs have seen an explosion of nearly $9 billion in net inflows since the central bank first spoke out on Sept. 27. On a NAV basis, the iShares MSCI India ETF (INDA) fund has risen 5% over the past quarter. And the iShares MSCI China ETF (MCHI) has rocketed higher by 20% over the same period.

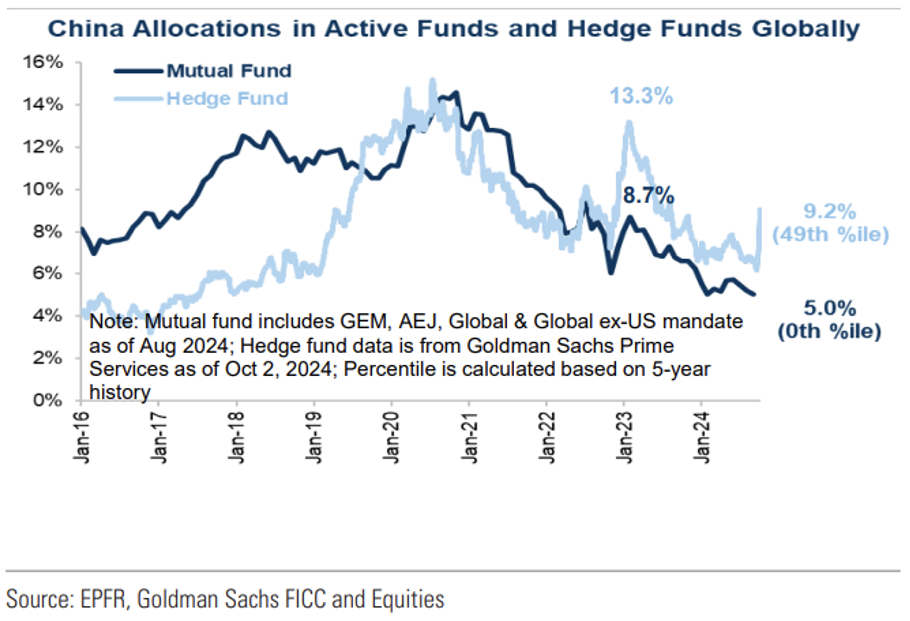

Until recently, capital market allocations to the world’s second-largest economy had been sitting at multidecade lows. Hedge fund exposure, for instance, remains historically low despite a recent rebound.

Given several false starts in recent years, many remain skeptical about China’s run-up. But others feel the rally may still have legs, thanks to investors’ severe under-allocation to China and a slowdown that’s pushed the central bank beyond its pain threshold.

Beyond China: Bringing More Balance

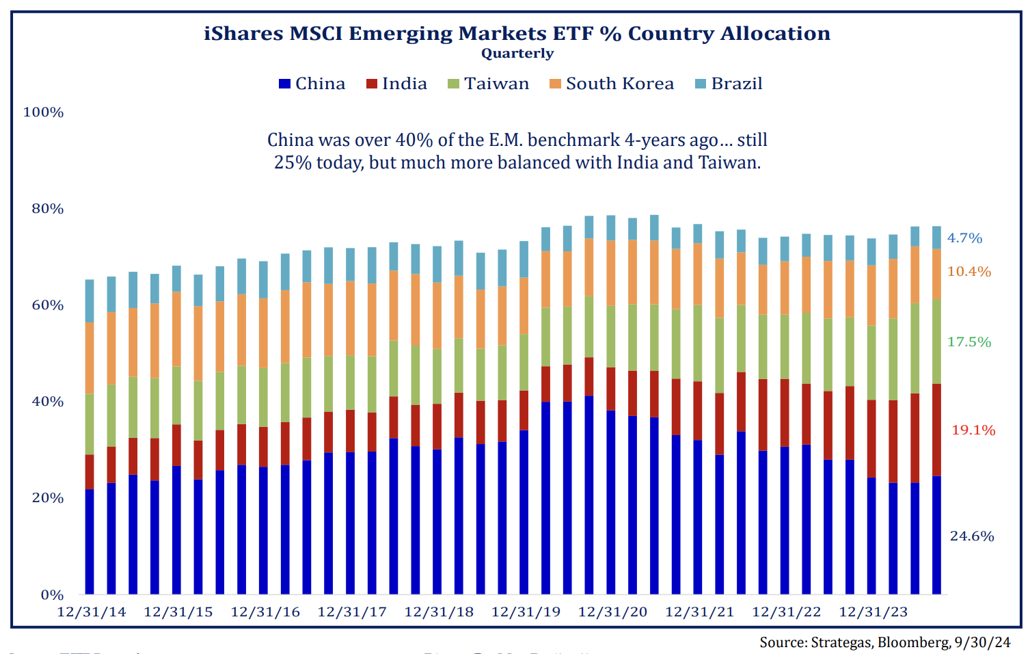

China’s massive rebound comes as the iShares MSCI Emerging Markets ETF (EEM), widely considered the EM benchmark due to its size and liquidity, is looking more balanced today than ever before. Just four years ago, more than 40% of the benchmark comprised China stocks. That compares to just a quarter of the fund’s weighting now, with India making up 19%, Taiwan accounting for 18%, and South Korea and Brazil making up the rest.

It’s been a similar story for the iShares Core MSCI Emerging Markets ETF (IEMG), which takes a broader-based approach with smaller-cap exposure. That fund topped the emerging market ETF flow charts over the past week — raking in roughly $660 million in net inflows — and comprising a 27% weighting in China stocks. Another behemoth, the Vanguard FTSE Emerging Markets ETF (VWO), gives an even greater weighting to India at 27%, while China stands at 20%. But unlike the iShares suite, which tracks MSCI indices, Vanguard tracks the FTSE Russell index, which does not classify South Korea as an emerging market.

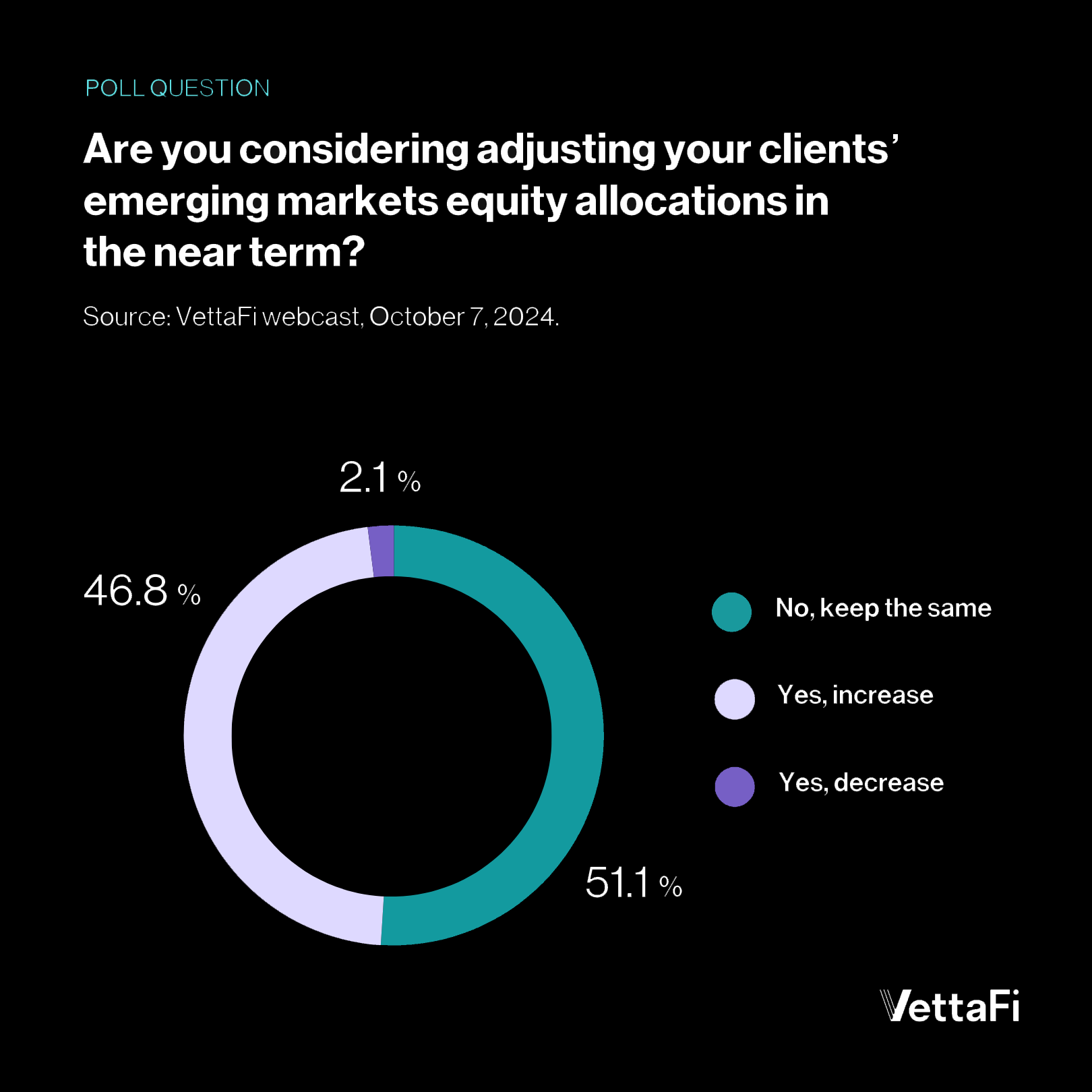

On a recent VettaFi webcast, when asked whether they were considering adjusting their clients’ exposure to emerging market equities, nearly half of all advisors said they were considering increasing allocations in the near term, while almost none said they would cut back on their emerging market exposure.

Getting More Systematic & Active

But there’s a growing divergence among broad EM equity ETFs, ex-China ETFs and several country-specific ETFs, as investors seek to fine-tune their exposure. The iShares China Large-Cap ETF (FXI) and INDA are attracting sizable inflows this year — approximately $2 billion each. Larger, all-inclusive index funds like VWO and EEM have seen net outflows of $1 billion to $2 billion each.

India has made powerful industrial and technological strides. The country has more than tripled the number of internet users in the last three years. It is now projected to see real GDP growth of 6.5% in 2025. The Nifty 50 index is set for a nine-year win streak, and INDA has risen 20% on a total return basis. The earnings-weighted WisdomTree India Earnings Fund (EPI) has also risen nearly 23% this year. It has seen more than $1.5 billion in new money.

Two funds consistently topping the list both last quarter and year to date are Dimensional’s Emerging Markets Core Equity ETF (DFEM) and Emerging Markets Core Equity 2 ETF (DFAE). This is further proof advisors are taking a more fundamental, systematic, factor-based approach to global equity investing at the expense of all-inclusive indexed ETFs. The Avantis Emerging Markets Equity ETF (AVEM) has also proven to be a popular choice, hauling in $1.7 billion. This is yet another fund relying on active stock selection expertise.

Between China’s bold stimulus plans, the Fed’s rate-cutting cycle, and India’s swift industrialization, emerging markets are enjoying a more favorable backdrop than they have in decades. These developments, coupled with relatively low valuations and more fine-tuning optionality, present a compelling case for taking a closer look at emerging market ETFs.

For more news, information, and analysis, visit VettaFi | ETF Trends.