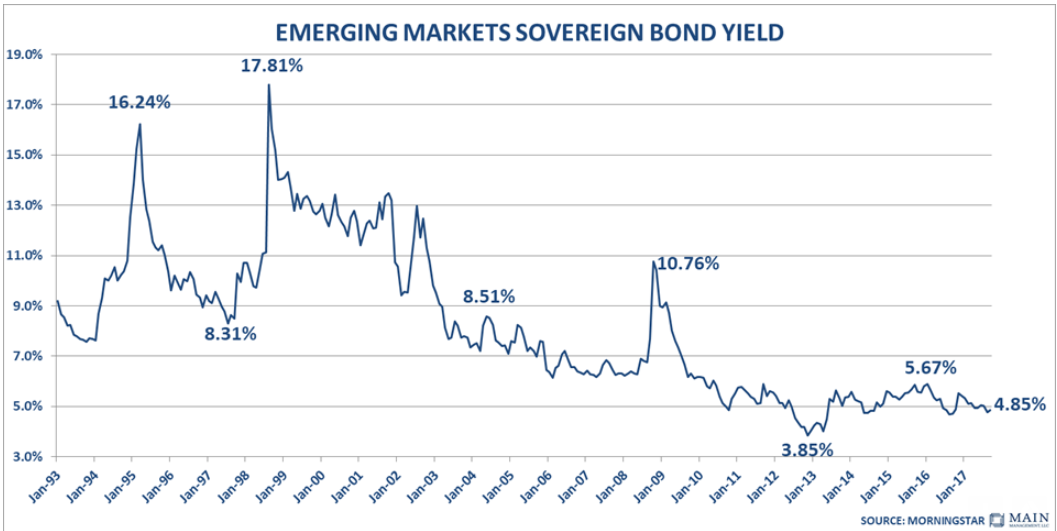

Interest Rates. Unlike the outlook which calls for rising interest rates trends in the Developed Markets, the Emerging Markets have recently experienced a decline in interest rates. The reason for the interest rate decline is a continued monetary easing by Central Banks in places like Russia, Brazil, Argentina, India and even China of late as well as from the impact of rapid global money supply growth. We believe the decline in rates is a very important factor in the outperformance for the Emerging Market. Just this year to date, the Emerging Market sovereign yields have declined from 5.42% to 4.85%. While a change of 57 basis points doesn’t sound dramatic, it is always the second derivative in rates that is important. That 57 basis points is a nearly 11% change in a little over 9 months. The decline in shorter term interest rates has been even more pronounced, dropping by approximately 70 basis points as Russia, Brazil, and India all eased and China stopped tightening in advance of its Communist Party Congress that takes place every 5 years. While the US, the Euro Area, and Japan have also had a slight decline in rates, the outlook is for their rates to rise as Central Bank tapering kicks in.

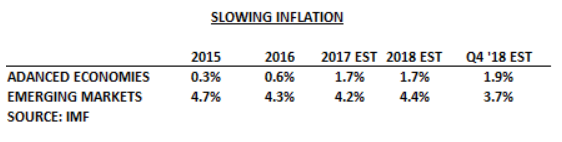

The next table indicates that consumer prices in the Emerging Markets are projected to decline from 4.6% in 2015 to an estimated 3.7% in the fourth quarter of 2018 according to the IMF. While we anticipate that world inflation will rise, we don’t believe that the change will be enough to derail the progress in the Emerging Markets. The same goes for interest rates. We expect a bottoming in interest rates as the Federal Reserve starts to reduce the size of its balance sheet and as the ECB trims its asset purchase policy. A bump in the Fed Funds rate is a virtual certainty by year end for the US, perhaps followed by another 1-2 moves in 2018. We believe rates will rise but less so in the Euro Area as the recent strength of the Euro is beginning to have a negative impact on growth there. In neither area, however, do we expect that a lift in rates would jeopardize growth prospects so, consequently, we agree with the direction (flat to higher GDP) of global trends predicted by the IMF. We expect more of the same in Japan, which is not much change at all in their rates. The other reason that the outlook for inflation remains tame is the longstanding deflationary impact of globalization, technology, and excess capacity worldwide.

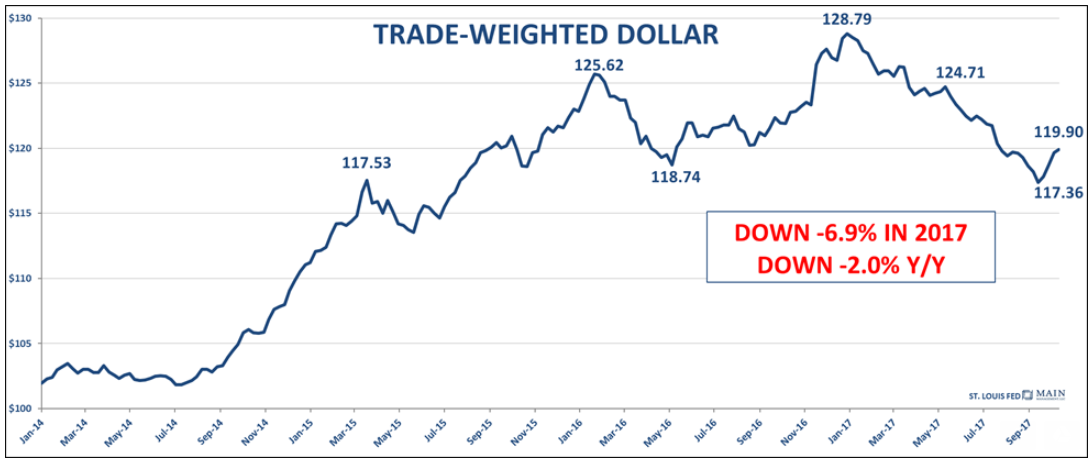

The dollar. A weak dollar allows the Emerging Market countries to continue to repair and rebuild their balance sheets. EM stocks have been negatively correlated to the dollar in recent times as higher US interest rates would negatively impact Emerging Markets as it increases their dollar-denominated debt burden. Since the trade weighted dollar is off about 7% in 2017, it has been a better environment in fiscal terms as well as stock market performance. Since we don’t believe that there will be much of a bump in interest rates between now and the end of 2018, we don’t believe the dollar will be an impact on the outlook for Emerging Markets.

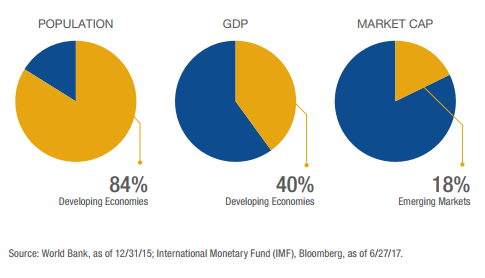

Investment Reallocation. Emerging Markets, as a class, are vastly under-represented in the investing world. The IMF suggests that the Emerging and Developing economies make up 60% of the total World GDP on a Purchasing Power Parity (PPP) basis. The World Bank data is even more dramatic as indicated by the facts that developing economies are 84% of the world’ population, generate 40% of world GDP (not on a PPP basis, but on an absolute basis in dollar terms), and only comprise 18% of the global market capitalization. Over time, we believe that indices will be rebalanced to reflect that reality and provide a constant demand for the shares.

Distribution of Population, GDP, and Market Capitalization

Valuation

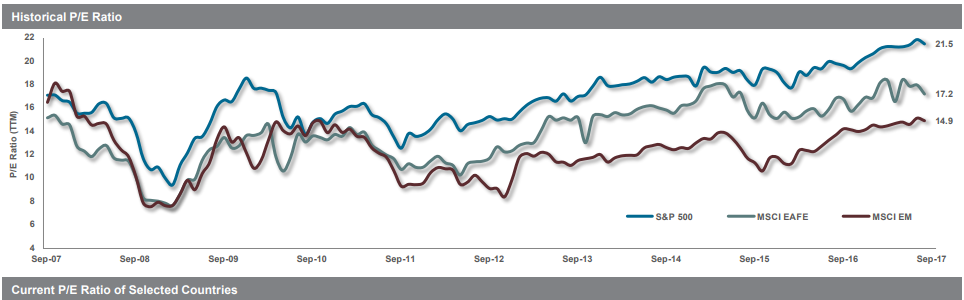

Our own work suggests that Emerging Market valuations are attractive. Relative to the S&P, the Emerging Markets have an advantage in P/E (14.6x vs 22.0x on trailing 12 months earnings); Price to Book Value (1.7X vs. 3.1X); and Price/Sales (1.5X vs. 2.1X). The chart below shows pictorially the different P/E multiples over the past decade for the S&P, the MSCI EAFE Index and the MSCI EM Index and clearly depicts the Emerging Market P/E discount to those indexes.

Global Stock Market Valuations as of September 30,2017

Source: Robert W. Baird & Co.

Conclusion

While Main Management has an overweight position in the Emerging Market space which has benefitted clients, we believe there is more room for appreciation. Recognizing that this is a volatile investment area, along with sustainable growth prospects for the world economy and even faster growth in Emerging Markets, coupled with improving fundamentals, the lagged effects of a benign interest rate picture, slowing inflation, a stable currency outlook, their diversifying character, the possibility of positive portfolio rebalancing, and an attractive P/E at around 11x 2018 earnings, all suggests to us that Emerging Markets is an area where continued exposure is warranted.

J. Richard Fredericks is founding partner at Main Management, a participant in the ETF Strategist Channel.

Disclosure Information

A pioneer in managing all-ETF portfolios, Main Management LLC is committed to delivering liquid, transparent and cost-effective investment solutions. By combining asset allocation insights with smart implementation vehicles, Main Management offers a unique approach that translates into distinct advantages for our clients, including diversification, cost efficiency, tax awareness and transparency. http://www.mainmgt.com