It’s not hard to guess what the hot watercooler talk was this week: the regional banking crisis. Today, the VettaFi Voices weighed in on the risk of contagion, what impact it might have on the Fed’s rate policy, and what it all means for the rest of the market and banking ETFs writ large.

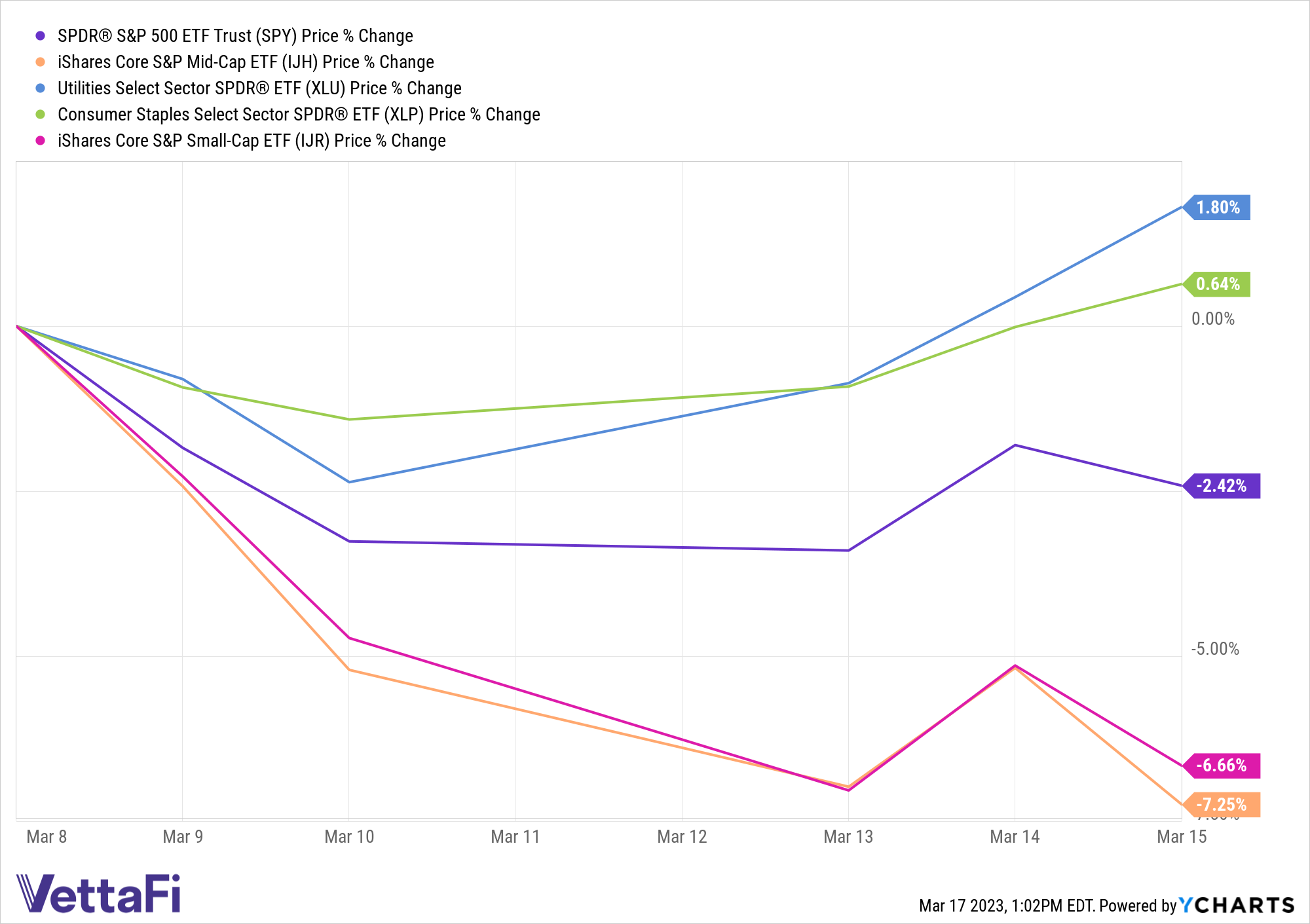

Todd Rosenbluth, director of ETF research: I’ll defer to Roxanna on financial ETFs specifically and look at the impact on the broader market. While the SPDR S&P 500 ETF (SPY) was down 2.4% in the week ended Wednesday, the iShares Core S&P Small Cap ETF (IJR) and the iShares Core S&P Mid-Cap ETF (IJH) were down 6.7% and 7.3%. Silicon Valley Bank (SIVB) was part of the large-cap S&P 500 Index, though, and was not a small- or mid-cap company.

Investors were selling out of higher-risk investments and turning to areas that were deemed safe havens, like the Utilities Select Sector SPDR (XLU), which was up 1.8%, or the Consumer Staples Select SPDR (XLP), up 0.6%.

Source: VettaFi and YCharts

Were interest rates to blame for how fast this spread? I think yes. The Federal Reserve aimed to jolt the U.S. economy with persistent, aggressive rate hikes over the past year, so it was inevitable there would be some parts of the economy not as well prepared to withstand the impact. But I expect we are going to see plans for more financial regulation to make sure something like a bank failure in two days doesn’t occur like this again so quickly.

Roxanna Islam, associate director of research: I just released a short research note on this: “Regional Banks: What To Watch For Next.” But there’s so much more to say on the topic.

First of all, March has been really rough on the financial sector. We’re seeing a bunch of different things happening at the same time, all of which are contributing to this downturn — which is basically the definition of contagion. In early March, Silvergate Capital (SI) announced plans to wind down, followed by the collapse of both Silicon Valley Bank (SIVB) and Signature Bank NY (SBNY). Now, we’re seeing issues with Credit Suisse (CS) and Financial Republic Bank (FRC), among others.

There are some structural deficiencies within the financial sector, particularly with how regional banks are regulated, compared to “systemically important” global banks, like Credit Suisse, for example. Regional banks aren’t subject to the same regulatory requirements, stress tests, etc. Many of these are also more “pure-play” relative to commercial banking activities when compared to larger banks, which have non-interest income like investment banking and trading activity.

Then there were some company-specific issues with a few of the banks — a large portion of which is psychological, including bank runs and the recent sell-offs for peer companies within the regional banking industry. I don’t think it matters how much of is psychological, though. The effect on stock prices and investor money is real, regardless of whether or not the sell-off is justified. Psychological fear can either increase or decrease over the next few days, depending on how government regulators handle these issues.

Specific to Silicon Valley Bank, the speed of which the bank run happened was accelerated due to social media (especially Twitter). A large portion of this bank’s customers were higher-risk venture capital firms, tech start-ups, etc. instead of retail customers. Meaning there were several issues at play:

- Weaker deposits, given the recent tech environment.

- These customers are stereotypically part of the Fintwit community, Reddit, and other social media forums.

- Many of these customers had deposits > $250,000, which is past the FDIC insured limit, so in the event of a bank run, they would be more likely to withdraw funds.

After news broke that Silicon Valley Bank needed to raise more capital, customers started tweeting about the bank’s capital and liquidity issues and pulling out deposits. Bank runs can be like self-fulfilling prophecies, and there’s basically no risk to withdraw your funds and a huge risk to leave your money in the bank. So many customers decided not to risk it and withdraw funds.

Unfortunately, here is where higher rates came in. Like most banks, Silicon Valley Bank had a bond portfolio to earn interest income, but a large portion of its bonds were long-dated Treasuries classified as “held-to-maturity” on their balance sheet, meaning they’re recorded at their original purchase cost. But with rising interest rates, bond prices fall. Faced with selling their bond portfolio to make up for the increase in deposit withdrawals, the company actually had a bond portfolio worth much less than was listed for in its financial statements.

All of this is pretty unique to Silicon Valley Bank. First Republic, for example, has been hit by the contagion partly because it is another bank based in the Silicon Valley. But it has over 1/3 of its customers’ deposits from retail customers and less of a balance sheet gap than SIVB. Similarly, Western Alliance Bank (WAL), which has a large portion of corporate clients, has only about a 15% exposure to tech and life sciences deposits and less than 2% of HTM securities.

Rosenbluth: The good thing for investors is that the directly impacted regional banks represented a small slice of the Financial Select Sector SPDR Fund (XLF) or even the SPDR S&P Regional Banking ETF (KRE). Regional banks represent a slice of the broader financial sector, which itself is only 10% of the S&P 500 Index. One of the benefits of using ETFs is diversification!

But the bad news is the fear of which bank might fail next could lead to broader pressure on these ETFs. As Roxanna said, sentiment is quite negative, and it might take more involvement from the government to change that.

Islam: Yes, good point. At the time of its collapse, Silicon Valley Bank was only 1.0% of KRE and 1.4% of the iShares U.S. Regional Banks ETF (IAT). As of yesterday, FRC was only 0.8% of KRE and 1.9% of IAT. So for the regional bank ETFs, there’s definitely some diversification in there to individual companies.

The issue is if the contagion spreads to the whole sub-sector. Also, interesting to note: If we look at some of these fintech ETFs, like the ARK Fintech Innovation ETF (ARKF), these are actually up close to 7% since last Friday, as many of these companies are more technology- or crypto-related and are becoming more attractive given the recent pullback in yields.

Rosenbluth: I love it when we come back to what’s inside an ETF. Not all “financial” ETFs are the same. I presume Silicon Valley Bank gets removed from the indexes behind these ETFs in coming days.

Islam: Yes. Also, since both banks were closed by regulators over the weekend, that means trading was halted on both Silicon Valley Bank and Signature Bank. Silicon Valley Bank last traded on March 9, while Signature Bank last traded on March 10.

Stacey Morris, head of energy research: Briefly, on the topic of contagion, investors may have been surprised by how much oil prices and energy stocks sold off on Wednesday. Concerns for the broader economy and the risk-off sentiment in the market weighed on energy commodities. U.S. benchmark oil prices fell over 5% to levels not seen since December 2021. The weakness in commodities in turn pressured energy stocks.

Importantly, energy infrastructure was more resilient than broad energy benchmarks or other energy subsectors, given its defensive qualities and fee-based business model. In volatile markets, the income on offer from the midstream space can be particularly attractive for enhancing total return.

Rosenbluth: That’s a good point, Stacey. While this seems like a banking or a broader financial story, banks can touch all sectors. Investors worried about a slowing U.S. economy will move away from cyclical sectors like energy. But not all energy stocks are impacted by the price of oil the same.

Morris: That’s right, Todd. Oil is clearly sensitive to the outlook for the global economy. To be fair, oil had a rough day on Tuesday as well (down 4.6%), but the down move clearly accelerated on Wednesday as Credit Suisse came into focus.

Rosenbluth: All that said, we do seem to be finding some stability. XLF and KRE were down just fractionally on Thursday, while the broader U.S. markets were higher. So perhaps this will not have long-lasting effects for the patient advisor and end clients who use dips in the market as a chance to buy.

For more news, information, and analysis, visit the Disruptive Technology Channel.