The ROBO Global Healthcare Technology and Innovation Index (HTEC) returned -2.9% during the quarter, closing the year with an annual gain of 3.5%, outperforming the MSCI World Health Care Sector, which posted losses of -10.68% and -5.14% for the same period. HTEC saw four out of the nine subsectors delivering positive results.

Earnings Analysis

The earnings season brought encouraging results, with 66% of companies in the index reporting positive year-over-year EPS growth and 84% achieving positive sales growth. These results are particularly promising given the expectations at the start of 2024, when the focus was on regrouping, de-risking, and laying the groundwork for accelerated growth in 2025.

This quarter brought robust performance from liquid biopsy companies (cancer detection via blood draw) as well as heightened volatility following the U.S. presidential election. The appointment of Robert F. Kennedy Jr. as head of the Department of Health and Human Services raised policy uncertainty, particularly for those companies linked to vaccine development.

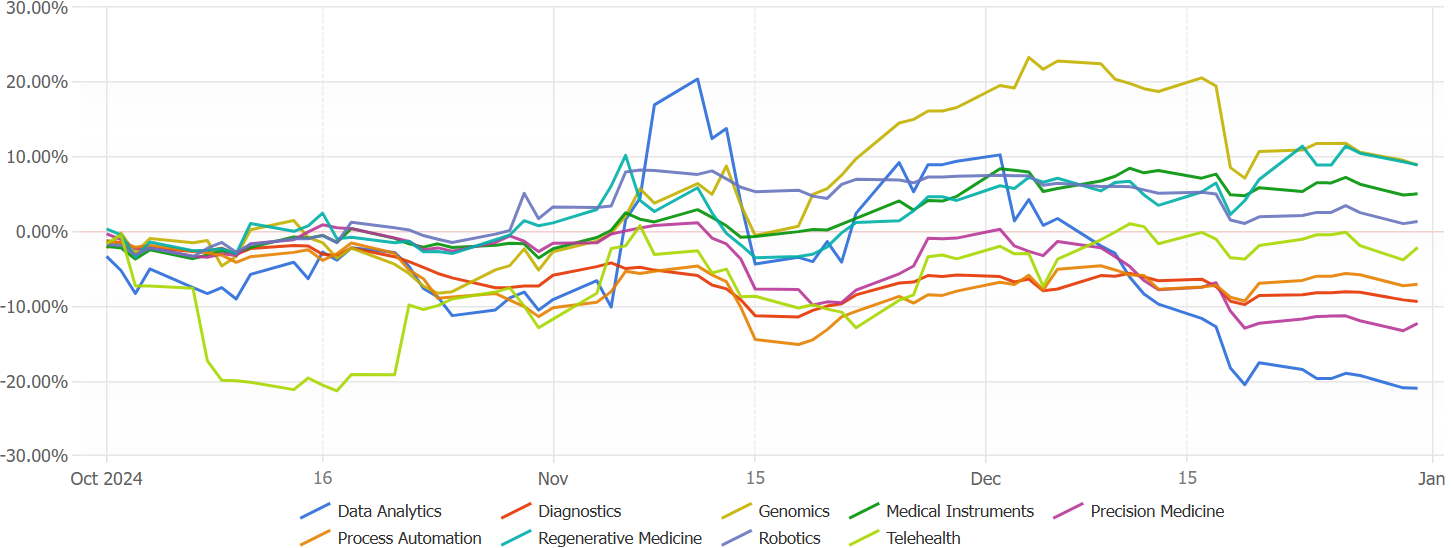

HTEC Group Returns

Genomics led the index with an 8.9% return, driven by Guardant Health, Grail, and Natera. October saw Guardant’s colorectal screening test, Shield, named to TIME’s Best Inventions of 2024, highlighting the transformative potential of liquid biopsy technology, a market valued at over $50 billion.

Regenerative medicine gained 8.9%, driven by Axogen’s strong performance and the FDA’s approval of its Advance Nerve Graft biologic license application and its expected high probability of success. Artivion sustained positive momentum, with its aortic stent grafts and On-X valve propelling global growth, supported by portfolio differentiation and positive trial outcomes.

Medical instruments ended the year strongly, with NovoCure achieving a Q4 return of 90.7% and a YTD return of 125.8%, driven by positive data from a pancreatic cancer study. Dexcom also showed recovery, posting a 16% return as it rebounded from a challenging sales force restructuring last quarter.

Precision medicine faced challenges, with Regeneron underperforming despite exceeding top and bottom-line estimates, due to concerns over Eylea HD adoption and biosimilar competition. Moderna also struggled, reflecting uncertainties regarding vaccine policies under the new administration.

Tempus IA, from the data analytics subsegment, experienced heightened volatility following its recent IPO and the expiration of its lock-up period, which enabled early investors to capture profits. This happened despite positive developments announced during its earnings call, including securing Medicare coverage for its cardiac dysfunction algorithms and achieving in-network provider status with Blue Cross Blue Shield of California and Illinois.

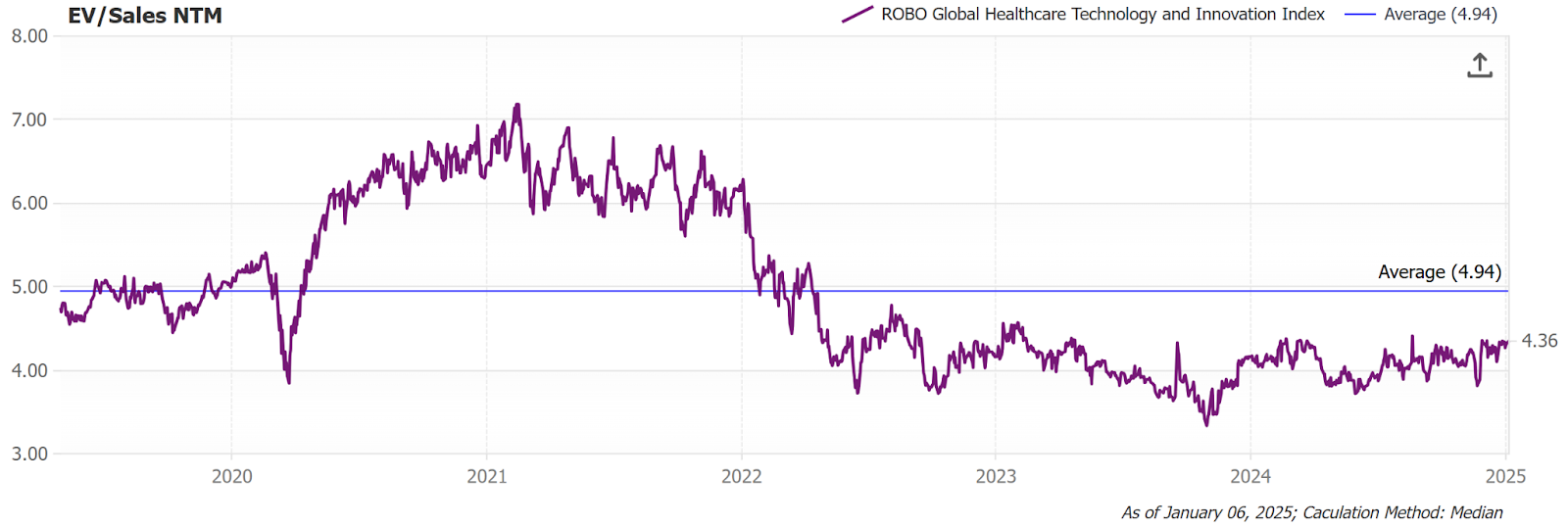

Valuations Remain Below Pre-Pandemic Lows

Looking ahead, annual reports are expected to provide greater clarity on 2025 forecasts. The easing of monetary policy and budgetary constraints could accelerate drug development and unlock delayed orders. While regulatory challenges in China persist, a focus on reshoring by the new U.S. administration may benefit segments such as Process Automation and Medical Instruments. Current valuations (NTM EV/sales) remain below pre-pandemic lows, presenting a potentially attractive entry point amid anticipated tailwinds for 2025.

VettaFi LLC (“VettaFi”) is the index provider for HTEC, for which it receives an index licensing fee. However, HTEC is not issued, sponsored, endorsed or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of HTEC.

For more news, information, and strategy, visit the Disruptive Technology Channel.