Figure 1 Source VettaFi

Overall, the ROBO Global Robotics and Automation Index saw a -5.6% return for the second quarter of 2024, underperforming the Vettafi Full World Index (VFWI) return of 2.87%, with only two of the eleven subsectors positive: Computing and AI (+8.58%) and Integration (+2.80%).

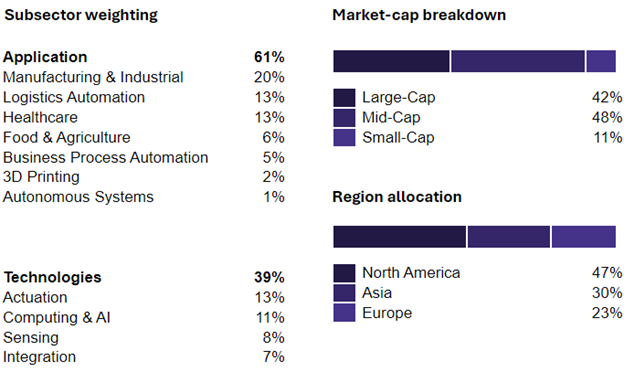

Figure 2 Source: FactSet/VettaFi

The decade ahead is shaping up to be defined by personal AI assistants and robotics, alongside breakthroughs in extended reality, climate tech, and biotechnology. We’re witnessing an unprecedented fusion of digital intelligence with our physical world, potentially transforming every aspect of how we live, work, and interact. The convergence of AI, Robotics and Energy innovation is the technology stack of our future.

Reflecting on the latest earnings season, the Robotics sector overwhelmingly saw year-over-year declines in EPS (-11.8%) and sales (-1.45%) on a weighted average basis, with 61.6% beating EPS and 67.6% beating sales estimates. Ultimately, this was unsurprising to due to 14 months of negative global PMI and slower growth in China.

Despite mixed performance, with 91% of reporting companies profitable, earnings commentary analysis shows signs of a recovery in core markets during the second half of the year., with consensus estimates currently aimed at 5.2% sales growth and 7.0% EPS growth in 2024 with a 2025 ramp up to 9.5% sales and 21.3% EPS growth (Factset, Weighted Avg. as of June 28, 2024).

Automation in Agriculture, which works to feed over 8 billion people worldwide, is seeing incredible adaptation to AI to streamline operations, increase energy efficiency, and hyper-target seeding, weeding, and increasingly picking, crop observation, and newer methods to support crop health. Additionally, robot arms and other automated solutions are increasingly being used to prep and cook foods.

In the Logistics subsector (-12.72%) GXO Logistics (-6.06%) announced an industry-first multi-year, commercial collaboration with Agility Robotics (private) Digit humanoid robot. Cargotec (+17.49%) spun out as part of a well-received demerger into two separate operating entities at quarter-end, Kaimler and Hiab, which operate in marine cargo handling and on-road load handling, respectively.

Figure 3 Source Factset/VettaFi

To those wondering how AI is already and currently impacting the robotics space, ROBO offers companies involved in manufacturing/inspecting semiconductor components, which are increasingly seeing automation beyond fabrication itself into less-automated areas (such as Apple looking to improve reliability across newer manufacturing regions through increased automation), including Teradyne (+31.51%), which offers chip inspection technologies. We continue to expect a “rising tide” scenario for companies providing underlying robotics technologies.

Additionally, many companies support the energy scale-out required by the energy transition, electrification, and growing data center demands, such as Delta Electronics (+13.74%), which enhances energy efficiency and enables smart automation within these facilities by providing advanced power electronics and automation solutions. Recent Q2 rebalance additions, such as Nvent Electric and Celestica, further emphasize this trend. Much of the energy transition requires increased robotic-enabled manufacturing capacity, key to the Manufacturing and Industrial Automation subsector, with companies like Emerson Electric (-2.56%), Yokogawa Electric (+4.75%), Yaskawa Electric (-14.3%), and companies in the Integration subsector leaders Schneider Electric (+7.37%) and Mitsubishi Electric (-3.84%). Remember this – more robots mean more energy, and vice-versa.

The ROBO index, on an index aggregate basis, saw its forward P/E decline from ~42.6x at the beginning of the year to 38.2X (Factset and Vettafi data, as of 6/28/2024), below the 5-year 43x average. Meanwhile, forward EV/Sales are closer to longer term average, at 3x. Our perspective remains that blue chip robotics companies are on discount, and that we are at the precipice of a new mass adoption cycle of robotics across society.

We believe that these blue-chip robotics companies are undervalued, presenting a prime opportunity as we approach a major mass adoption cycle. The robotics sector is at a pivotal inflection point, driven by structural and geopolitical advantages and breakthroughs in AI and energy. These advancements are enhancing capabilities and fueling demand, creating a virtuous cycle poised for substantial growthDis along a J-curve trajectory.

VettaFi LLC (“VettaFi”) is the index provider for ROBO, for which it receives an index licensing fee. However, ROBO is not issued, sponsored, endorsed, or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing, or trading of ROBO.

For more news, information, and analysis, visit the Disruptive Technology Channel.