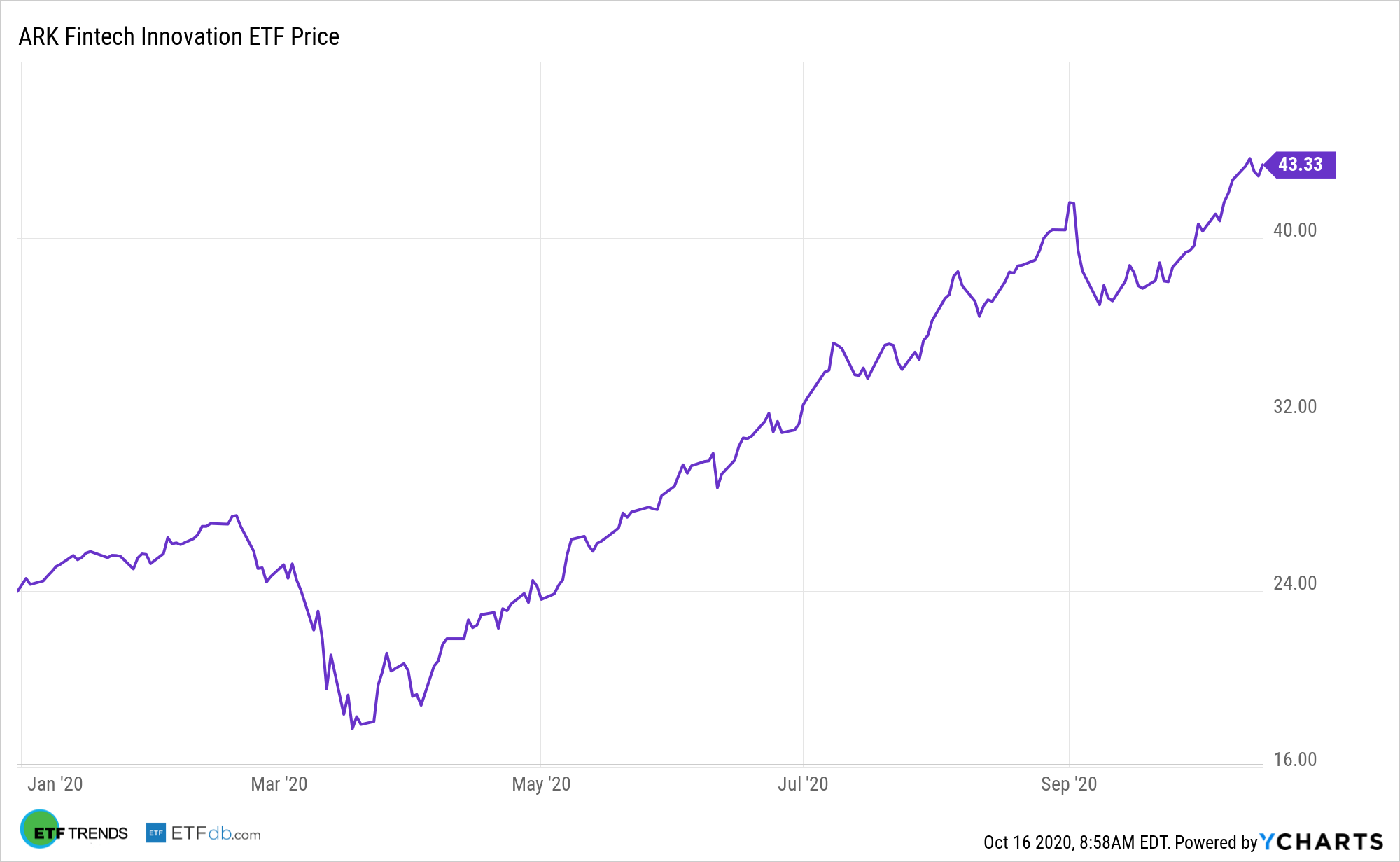

Digitization is disrupting myriad industries, including traditional financial services, opening doors to lucrative opportunities with assets such as the ARK Fintech Innovation ETF (NYSEARCA: ARKF).

Whether it’s lending, payroll or cashless payments, ARKF components are at the center of a groundswell that’s dramatically altering the financial services landscapes, leaving many old guard institutions in the dust. The retail payments space is a universe in which many ARKF holdings are already thriving at the expense of traditional banks.

“Competition in the retail payments sector is intensifying around the world,” said Moody’s Investors Service. “Fast-changing technologies are driving a rapid increase in online and mobile payments with new players, offering slick, single-click digital wallets and smartphone apps, grabbing part of the retail payments market, an area traditionally dominated by banks.”

ARKF invests in equity securities of companies that ARK believes are shifting financial services and economic transactions to technology infrastructure platforms, ultimately revolutionizing financial services by creating simplicity and accessibility while driving down costs.

ARKF’s Ascent and The Future of Finance

Adding to the allure of ARKF is that some of its components, such as Square (NYSE: SQ) and PayPal (NASDAQ: PYPL), are filling niches overlooked or under-serviced by traditional banks and doing so at more attractive margins, leading to market share increases at the expense of those older institutions.

“Historically, banks have been the main providers of retail payment services and have used their relationships with customers to sell consumer loans and other financial products,” said Moody’s. “In a digital world, as banks lose market share in retail payments they may lose their competitive advantage in consumer finance as well as valuable consumer financial data.”

ARKF member firms are companies that are powered by innovations and are working to disintermediate or bypass the current financial markets and challenge traditional institutions by offering new solutions that are better, cheaper, faster, and more novel and secure.

Cash might be king, but financial technology (fintech) might have something to say about that. The Covid-19 pandemic may have spurred an increase usage of digital forms of payment. Proving that ARKF components are disrupting banks is the theory that over time, banks may need to pay up to retain customers, something the companies are likely loathe to do as interest remains low.

“Increased competition for deposits with digital players is likely to undermine depositor loyalty, forcing banks to pay more to maintain deposit inflows. In addition, as digital services proliferate, payment management and budgeting tools may allow consumers to better regulate cash flows and so maintain lower deposit balances,” according to Moody’s.

For more on disruptive technologies, visit our Disruptive Technology Channel.

The opinions and forecasts expressed herein are solely those of Tom Lydon, and may not actually come to pass. Information on this site should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation for any product.