By Scott Opsal

The decade ending in 2019 was remarkable in that it contained not a single recession nor bear market, yet within this apparent stability, the return earned by the top-performing sector was more than 10 times that of the worst. In an age where stock trades are measured in milliseconds, we get a fresh perspective when evaluating sectors and industries over a ten-year window. This “decade in review” examines the performance of sectors and industries, looking at the best and worst groups to reveal the stories they have to tell.

Sector Returns

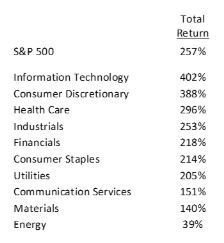

We begin at the sector level with Table 1 presenting total returns for ten S&P 500 sectors from 12/31/2009 to 12/31/2019 (the Real Estate sector is excluded as it did not appear until mid-decade). Only three sectors beat the overall S&P 500 index; portfolio managers who selected stocks from the broad market had little chance of outperforming. The top sectors were all driven by innovation and unit growth, and investors who focused on that particular aspect of a company’s business model were nicely rewarded.

The dominant economic story of the decade was the emergence of Social/Mobile/Cloud as a wide-ranging force in changing personal lifestyles, commerce, and business operations. Tech’s +402% return was led by titans Apple (up 1,021%) and Microsoft (+557%), as their huge market caps and outstanding returns boosted the sector into first place. A second theme driving the Tech sector was the exploding acceptance of electronic payments in all forms and fashions. This revolution helped Visa (+824%) and Mastercard (+1,126%) power ahead, even though credit cards are hardly a recent innovation.

Health Care had its fair share of winners in Biotech and Medical Devices, but the heavy lifting was done by Health Insurers and Managed Care companies. United Health (+1,020%), Humana (+803%), and Aetna (+638%) soared this decade following a beat-down caused by political worries over the 2010 passing of the Affordable Care Act. After being pummeled by concerns over their very existence, Managed Care companies rebounded from the Obamacare rhetoric and, combined with excellent business performance, made the industry far and away the top performing Leuthold industry group for the last decade.

Seeing Consumer Discretionary in second place is a bit unexpected, to say the least. One might be inclined to  say, “Whoa, wait a minute. Technology and Health Care are innovators, but Consumer Discretionary? I spent all decade reading about retailers going out of business, and the automakers are dull as dirt. What gives?” In a word: Amazon. The internet retailing colossus accounts for 30% of the Consumer Discretionary sector, and its +1,274% return during the decade provided a tremendous boost for what is often seen as a mature and cyclical sector. Amazon was not the only big influence here, as several other powerful retail brands chipped in with stellar gains. Home Depot (+856%), Starbucks (+794), Booking Holdings (+840%), and Netflix (+1,304%) did more than enough to offset the likes of Sears and J.C. Penney. Viewing returns across a ten-year period reminds us of one of the most important maxims of stock investing: winning companies can gain 1,000% or more, but losers can only fall 100%. The upside skew from Amazon and friends carried Consumer Discretionary to a wonderful decade of performance.

say, “Whoa, wait a minute. Technology and Health Care are innovators, but Consumer Discretionary? I spent all decade reading about retailers going out of business, and the automakers are dull as dirt. What gives?” In a word: Amazon. The internet retailing colossus accounts for 30% of the Consumer Discretionary sector, and its +1,274% return during the decade provided a tremendous boost for what is often seen as a mature and cyclical sector. Amazon was not the only big influence here, as several other powerful retail brands chipped in with stellar gains. Home Depot (+856%), Starbucks (+794), Booking Holdings (+840%), and Netflix (+1,304%) did more than enough to offset the likes of Sears and J.C. Penney. Viewing returns across a ten-year period reminds us of one of the most important maxims of stock investing: winning companies can gain 1,000% or more, but losers can only fall 100%. The upside skew from Amazon and friends carried Consumer Discretionary to a wonderful decade of performance.

Fundamentals Decide The Decade

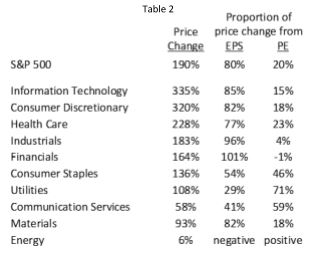

The Leuthold research team has written extensively about the elevated equity valuations that have existed since the 1990s, and how a high and rising P/E has flattered S&P 500 returns during this bull market. However, over the long run, it is the fundamentals that drive relative equity prices, and we explore the decade’s results in Table 2. The cumulative price change since 2009 is listed for each sector along with our estimates of the proportion of the price change coming from EPS growth (fundamentals) and P/E expansion (valuation).

We approximate that 80% of the S&P 500’s gains since 2009 came from growth in forward EPS, with the other 20% coming from P/E expansion. (We use forward EPS estimates because our preferred metric, trailing EPS, was severely depressed in 2009, and calculating 10-year growth rates off a cyclically low base would portray a distorted message.) The three sectors that outperformed the S&P 500 all had more than 75% of their price gains driven by business results, and the fact that each experienced widening valuations along with strong earnings made for a highly profitable decade.

Although the fundamentals powered most of the gains in the top performing sectors, three sectors did experience significant valuation gains. Consumer Staples and Utilities benefited from the ultra-low interest rate environment and the search for yield. These stable dividend payers became investor favorites, yielding more than bonds while offering the potential for growth. However, despite becoming a yield investor’s best friend, Staples and Utilities could not outperform the S&P 500. Their slow growth end-markets held these sectors back, even with substantial valuation upgrades. As for Communication Services, we believe its P/E expansion is an illusion. The sector began the decade holding telephone companies and, after a major GICS restructuring, ended the decade with the likes of Facebook, Alphabet, and Disney. This material upgrade in growth and quality certainly merits a higher valuation for this new economy sector.

Then there is Energy, by far the worst sector of the decade. The price of crude oil fell from $79 to $61 over the last ten years, a 23% decline that created a stiff headwind for Energy company earnings. Although crude prices were an issue, we believe the primary cause of the Energy sector’s dismal decade was the surging importance of fracking. The development of shale resources has radically changed the U.S. oil landscape, but it isn’t at all clear that shale is a profitable business model. The industry has been backed by oodles of cheap debt, yet analysts widely question whether the companies have ever been cash flow positive, or ever will be. Steep production decline curves mean companies have to run hard just to keep from sliding backward, and if the day comes when debt is neither cheap nor easy, this business model could collapse. Shale has done wonders for the country’s energy independence, but it has been a millstone around the neck of the decade’s worst performing sector.

Industry Groups

The Leuthold Group’s equity disciplines operate at a more granular group level, and this section highlights some

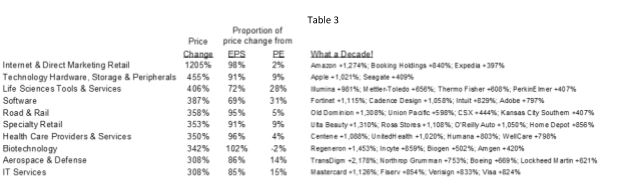

of the major winners and losers selected from GICS Level 3 industries. We repeat the methodology of showing total price change and the estimated proportion coming from EPS growth and P/E change. This exercise allows us to cast a sharper eye on the decade’s winners and losers. Table 3 parades the top industries by price change, and seven of the ten could be considered as inventors, innovators, or disruptors (eight if you include Aerospace). Eight industries earned at least 85% of their gain from earnings growth, reinforcing the notion that over the long run, fundamentals drive price performance.

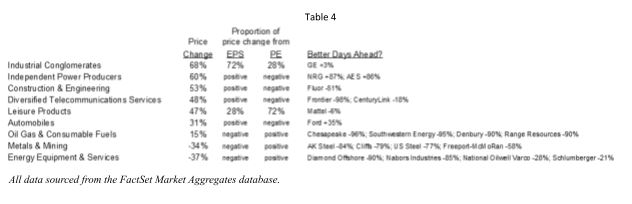

The sad sacks in Table 4 reflect the return drag that comes with unsuccessful businesses. Negative earnings growth in three industries and valuation declines in another four doomed them to price gains less than a third of the S&P 500. Four of the nine are connected to the Energy sector, and we believe a fifth, Construction & Engineering, is also closely linked to the energy complex. Wireline telephone companies are on the way out, auto companies have no forward momentum, and then there is poor old General Electric. Avoiding these secular losers would have benefited any investor who was paying attention to long-term economic trends.

Research Takeaways

- It was a top-heavy decade as only three of ten sectors outperformed the overall S&P 500. Broad-based or equally weighted investors faced a difficult challenge in keeping pace.

- Innovation, new business development, and unit growth powered the decade’s winners. The top sectors and groups realized the vast majority of their gains from EPS growth driven by excellent business fundamentals.

- Staples and Utilities finished middle of the pack despite their mature, slow growth businesses. They benefited from rising valuations triggered by the search for yield in stable dividend-paying stocks. Energy came up a dry hole as fracking changed the sector’s profile, making it dependent on easy and cheap debt financing to constantly offset steeply declining production rates.

- Investors do not need to play in risky areas like venture capital or biotech startups to reap portfolio-defining gains. Over a full decade, well known and reputable companies that are in the economy’s sweet spot can deliver ten-bagger returns without taking all-or-nothing risks.

Scott Opsal is Director of Research & Equities for The Leuthold Group, LLC, and co-portfolio manager of the Leuthold Core ETF (LCR).