While pure-play electric vehicle stocks have lost some of the interest seen in 2020-2021, demand continues to grow for the overall future mobility market including pure-play stocks like Tesla (TSLA) and Rivian (RIVN). On July 2, Tesla reported that it produced almost 480,000 vehicles and delivered over 466,000 vehicles in 2Q23. During that same time period, Rivian — which has dealt with supply chain issues and missed its previous targets — also increased production to almost 14,000 vehicles and delivered over 12,600 vehicles, which puts the company on track for 2023. Both Tesla and Rivian have surpassed analyst estimates and have illustrated that continued demand for electric vehicles despite several barriers to EV adoption along with higher interest rates restraining higher-end vehicle purchases.

Some non-traditional auto manufacturers are ramping up sales in the U.S.

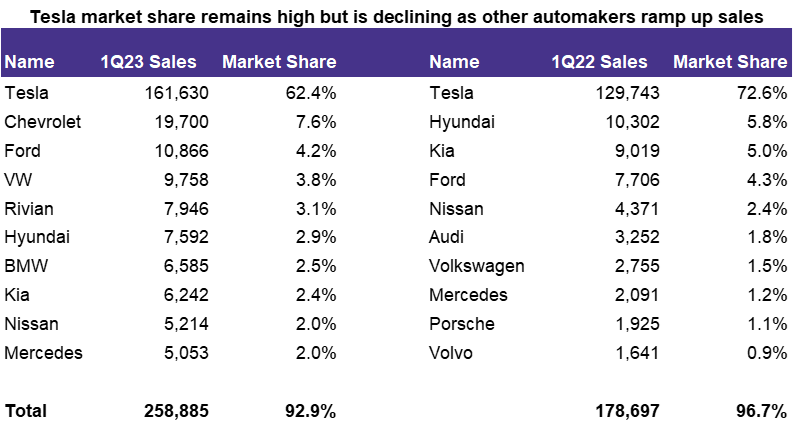

Pure-play EV companies, which were extremely popular during 2020 and 2021, were hit by production delays due to supply chain issues and many continue to miss their production targets and remain in pre-delivery and revenue stages. As EV manufacturers are starting to vertically integrate and/or bring production back into the U.S., they are beginning to gain market share alongside traditional auto manufacturers. In 2021, Tesla held majority of U.S. battery electric market share at around 72.2%. This number decreased to 64.5% in 2022 and 62.4% in 1Q23 (full 2Q23 data for the industry has not yet been released). While still a leader in the industry, Tesla has lost some market share to legacy automakers like Chevrolet and Ford. Chevrolet, which wasn’t even in the top 10 in 1Q22 was second in 1Q23 with 7.6% of U.S. market share. And as we are seeing with Rivian, there’s still a chance for smaller, pure-play companies to turn around. Rivian sales were only 0.7% of total U.S. market share a year ago in 1Q22. In 1Q23, Rivian held 3.1% in market share (ranked fifth). In 2Q23, market share is likely to be even higher since sales have increased significantly. Besides Rivian, there’s also been a shift in several other smaller pure-play manufacturers. Lucid Motors (LCID) and Polestar have also increased sales by almost 200% y/y and 115% y/y, respectively, illustrating that the race to electric doesn’t just belong to legacy automakers.

Despite growing sales, there are still some challenges to demand.

Pure-play EV companies face challenges including not being a “household name.” While these may have been popular stocks in the past, when it comes to actually buying a vehicle, many consumers prefer well-known manufacturers like Toyota, Nissan, etc. which are releasing new models including electric SUVs like the Toyota bZ4X and the Nissan Ariya. Charging infrastructure is still a large barrier for the overall industry even though there are plenty of public charging infrastructures, which may still be inconvenient for people that live in apartments, condos, or other living situations without a private garage. Higher interest rates are also a significant obstacle for retail consumers. While there are some budget EV models, electric vehicles tend to cost more than their internal combustion engine (ICE) counterparts and consumers may be more reluctant to finance at higher interest rates.

Profitability remains a bigger challenge than demand.

While there are certainly some barriers to adoption, demand and sales are still continuing to grow. The bigger issue comes from an investment perspective — besides Tesla, EVs are not yet profitable. Rivian, for instance, has undoubtedly made strides from a sales perspective. But the company still reported a net loss of $1.35 billion in 1Q23. Even legacy automakers which are profitable overall are still unprofitable in their electric segments. This was recently addressed by Ford, which provided analysts and investors with one of the most detailed, transparent plans regarding future profitability (see this note for more details).

So where do companies like Tesla and Rivian fit in EV ETFs?

Tesla is a top holding in all future mobility ETFs, given that it holds over 60% of market share in the U.S. The company also has a market cap of $878 billion and most future mobility ETFs follow a market-cap weighted index. It is also the highest performing holding YTD (+129.3%) after NVIDIA (+189.6%). Rivian is less common in future mobility ETFs since it has a relatively smaller market cap of $19 billion and has more recently started ramping up its production. But while it currently has less weight, it is important to the industry since it shows that it is possible to overcome production delays and gain significant market share in a still relatively nascent industry. And outside of traditional auto and EV stocks, it is also worth noting that future mobility ETFS have large allocations to semiconductor stocks and other EV enabling technologies (see this note for more details).

For more news, information, and analysis, visit the Climate Insights Channel.

VettaFi LLC (“VettaFi”) is the index provider for CARZ, for which it receives an index licensing fee. However, CARZ is/are not issued, sponsored, endorsed or sold by VettaFi, and VettaFi has no obligation or liability in connection with the issuance, administration, marketing or trading of CARZ.