2025 brings with it a number of likely challenges for the global market. Investors looking for contrarian opportunity need look no further than the Asia high yield bond market and the KraneShares Asia Pacific High Income USD Bond ETF (KHYB).

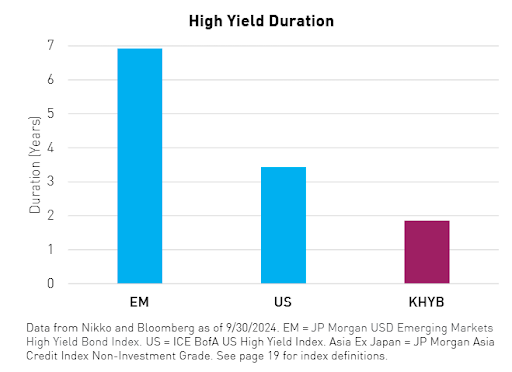

Bonds within the Asia Pacific region offer often overlooked opportunity for investors. The Asia region ex-Japan demonstrated stable growth in the last decade plus, increasing 264% in market cap between 2010-2024. It also offers the potential for a lower default rate than other emerging markets, specifically within high yield bonds. With average yields over 7% in the last decade and lower durations than U.S. high yield and broad EM, the asset class warrants consideration for those with the risk tolerance.

KHYB is an actively managed fund that invests in USD-denominated high yield debt securities from companies in Asia, excluding Japan. The fund is poised to capture ongoing recovery and growth within the Asia bond market.

KHYB currently offers a 12-month distribution rate of 15.67% with a 30-day SEC yield of 7.01% as of December 16, 2024. Distribution rate annualizes the most recent fund distribution and divides by the fund’s NAV at time of distribution.

Under the Hood of High Yielding KHYB

The fund is benchmarked to the JPMorgan Asia Credit Index (JACI) Non-Investment Grade Corporate Index and invests in high yield fixed income securities, or “junk bonds”. These bonds rate below the four highest categories (Ba1/BB+ or lower) by at least one credit rating agency. If unrated, the subadvisor seeks those of similar quality. Notably, high-yield corporate bonds in Asia historically default less than their peers. They also carry lower duration on average.

Image source: KraneShares

“The default rate of Asia high-yield corporate bonds has been lower than that of high yield bonds in other emerging market regions in six of the past thirteen years,” KraneShares explained on the fund’s page. Additionally, the default rate “was lower than the US high yield default rate in both 2019 and 2020.”

Nikko, the sub-advisor, uses top-down macro research and bottom-up credit research to create the portfolio. They also utilize a proprietary process that combines qualitative and quantitative factors used to value an issuer’s credit profile.

By moving the credit curve up, KHYB will be more defensive against the benchmark and have shorter-duration bonds than the index. When the bonds mature, Nikko decides how and when it wants to redeploy and invest in new bonds. It makes these decisions dependent upon market conditions.

KHYB carries an expense ratio of 0.69%.

For more news, information, and analysis, visit the China Insights Channel.