The world’s largest asset managers are scrambling to devise new ways to package private investment opportunities into a passive ETF wrapper. Private assets are the fastest-growing market in the financial world — but could also prove the most challenging field for ETF providers to penetrate.

Private markets are alluring for investors due to their potential for higher yields, diversification and substantial returns. For asset managers, high fees and profit margins are hard to ignore. Traditionally, private assets like private equity, private debt, real estate, infrastructure, and venture capital have been the exclusive domain of large institutional investors and the wealthy elite. Family offices have increasingly embraced private equity, with allocations surpassing public equity allocations for the first time.

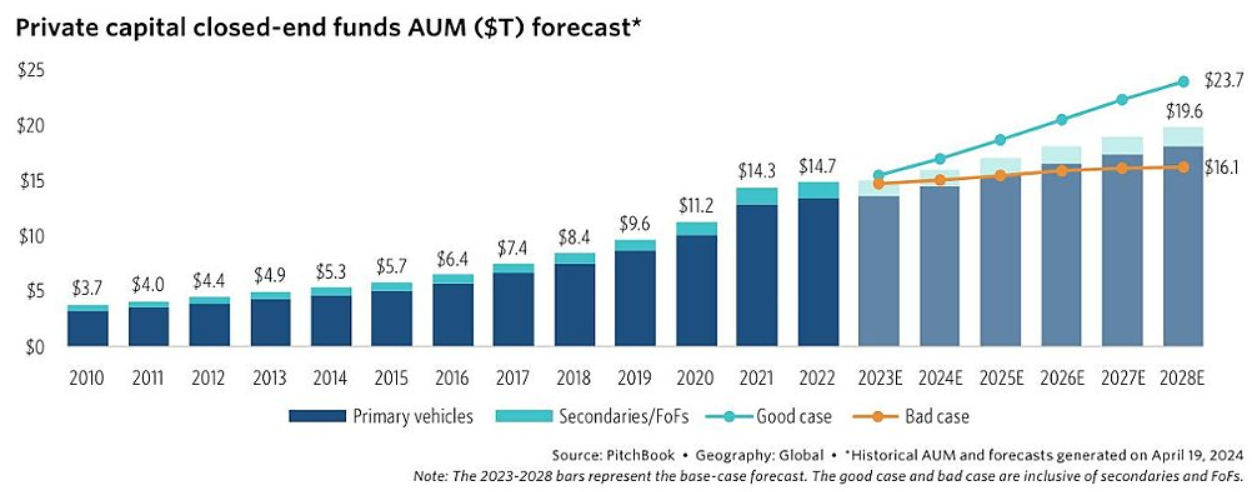

Currently worth more than $13 trillion, the private market is projected to reach nearly $20 trillion through 2028, according to PitchBook. Retail investors presently have zero direct exposure to private markets. But bundling them into an ETF wrapper would set the stage for retail consumption at a fraction of the cost.

Behemoths like BlackRock and Invesco are at the forefront of the push to democratize private markets, clamoring to construct private asset ETFs. BlackRock just inked a $3.2 billion deal for U.K.-based alternative asset data company Preqin – underscoring its commitment to “indexing private markets.” Apollo Global and Goldman Sachs are also exploring opportunities in this space.

Existing Paths to Private Assets

Currently, the only avenue to private equity is through ETFs that provide limited exposure to private equity companies. Invesco offers its own Global Listed Private Equity ETF (PSP), which has risen 12% this year and has seen a smattering of net inflows. The $246 million fund invests in globally listed private equity firms across the U.S., Europe and Asia – providing indirect access to hundreds of private companies and charging a net expense ratio of 1.06%. Top holdings include KKR, Blackstone and the Carlyle Group.

The ProShares Global Listed Private Equity ETF (PEX) similarly invests in publicly traded PE firms predominantly in the U.S. and Europe and charges a heftier fee of 2.79%. Other ETFs offer indirect exposure via access to IPOs and special-purpose acquisition companies.

Several firms attempt to replicate PE funds by investing in small- or micro-cap companies, perceived to share similar attributes with private equity. KraneShares just filed for a new ETF that will track an index of small- and midcap stocks thought to be similar, though not identical, to the kinds of companies in buyout funds.

Investors have also increasingly sought access to the more developed private debt space. Bank loan ETFs have been all the rage this year, serving as proxies for private credit, which has filled a big void in the wake of last year’s regional banking crisis. The Invesco Senior Loan ETF (BKLN) and the SPDR Blackstone Senior Loan ETF (SRLN) are the two largest and most popular on the market.

Private Asset ETF Pushback

The push for private asset ETFs faces plenty of regulatory and educational challenges. Private markets, which are valued infrequently, don’t align well with the ETF model, which relies on daily trading, huge liquidity, transparency, and low costs. The SEC’s mandate that open-ended funds hold no more than 15% in illiquid assets complicates the pricing of such ETFs. If not managed carefully, these products could trade at significant discounts or premiums to their net asset value. Proponents might argue perfect replication isn’t necessary if such ETFs can still capture the bulk of the risk/return profile that private assets bring to the table.

Some have suggested using synthetic exposure, or swaps written against private equity portfolios, but this approach essentially uses a liquid vehicle to trade illiquid assets. Liquid alternative ETFs, which use leveraged or derivatives strategies, are another option, though they can be costly. The ARK Venture Fund, a closed-end interval fund that invests in both private and public equities tied to disruptive tech, charges a total expense ratio of 2.90%.

Despite these hurdles, the ETF industry has shown an incredible capacity for innovation for virtually every type of product imaginable. Where profits are possible, there’s usually a way. If successful, these innovations could pave the way for retail to gain access to a once-exclusive private market party.

For more news, information, and analysis, visit VettaFi | ETF Trends.