For years, high-profile advisors and investors have taken advantage of autocallable notes to lock in compelling income from equities.

Autocallables are market-linked notes that provide coupon payments and principal based on equity performance. Each autocallable note will be linked to a specific equity index, such as the S&P 500.

From there, the autocallable note generates income as long as its index does not drop beneath its coupon barrier level. For instance, if an autocallable uses the S&P 500 as its index and has a barrier of -40%, the autocallable will continue to pay out coupons if the S&P 500 does not drop below -40%.

Regardless of whether the index is up, down, or neutral, the autocallable note will continue to pay income until the note is called or the index drops below its barrier level. This gives autocallables a great niche as a way for investors to lock in monthly income, even when market performance is relatively mediocre.

CAIE Offers Easy Access to Autocallable Income

Recently named Most Innovative Product by SRP Americas 2025, the Calamos Autocallable Income ETF (CAIE) can make it easier than ever to gain access to autocallable income.

Considering their compelling use cases, it may seem surprising that autocallables are not more commonplace in investor portfolios. This is due to the relatively high barrier of entry for regular investors and advisors to cultivate autocallable notes. award-winning,

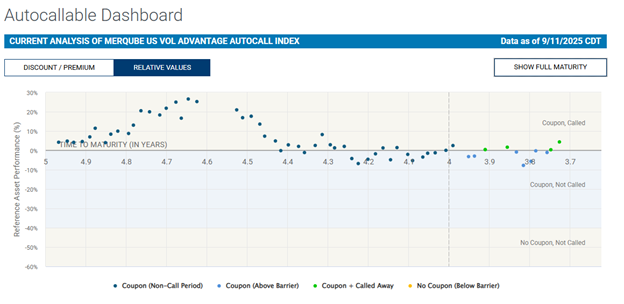

CAIE provides its investors with a laddered portfolio of more than 52 different autocallable notes within its portfolio. This creates continuous exposure to a selection of income-generating notes linked to the S&P 500. The Calamos Autocallable Dashboard allows investors to see the specifications of each autocallable in the reference index.

Source: Calamos, www.calamos.com/CAIE

Considering the uncertain macroeconomic environment, opting for an autocallable strategy may quickly pay off. Even if the market gets bumpy, CAIE’s autocallables will still be able to generate significant monthly income, as long as the S&P 500 doesn’t drop below the -40% barrier level.

CAIE’s trailblazing strategy has already ignited significant interest from the broader investment community. The fund is approaching $200 million in total net assets since its launch on June 25, 2025.

For more news, information, and strategy, visit the Alternatives Content Hub.

Before investing, carefully consider the fund’s investment objectives, risks, charges and expenses. Please see the prospectus and summary prospectus containing this and other information which can be obtained by calling 1-866-363-9219. Read it carefully before investing.

An investment in the Fund(s) is subject to risks, and you could lose money on your investment in the Fund(s). There can be no assurance that the Fund(s) will achieve its investment objective. Your investment in the Fund(s) is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency. The risks associated with an investment in the Fund(s) can increase during times of significant market volatility. The Fund(s) also has specific principal risks, which are described below. More detailed information regarding these risks can be found in the Fund’s prospectus.

The principal risks of investing in the Calamos Autocallable Income ETF include: autocallable structure risk, contingent income risk, early redemption risk, barrier risk, authorized participant concentration risk, calculation methodology risk, cash holdings risk, correlation risk, costs of buying and selling fund shares, counterparty risk, credit risk, derivatives risk, equity securities risk, index risk, interest rate risk, investment in a subsidiary, laddered portfolio risk, liquidity risk, market maker risk, market risk, new fund risk, non-diversification risk, premium-discount risk, secondary market trading risk, swap agreement risk, tax risk, trading issues risk, valuation risk, and volatility target index risk.

Autocallable Structure Risk –The Fund’s returns are correlated to the performance of a synthetic portfolio of autocallable notes tracked by the Laddered Autocall Index.

Unmanaged index returns, unlike fund returns, do not reflect fees, expenses or sales charges. Investors cannot invest directly in an index. Total return assumes the reinvestment of income. Current performance may be higher or lower than the performance data shown. Yields represented by trailing 12 month yield for: US Equity- S&P 500; U.S High Yield – Bloomberg US Aggregate Corporate High Yield Index; US 10-year – 10-year US Treasury yield; Equity Premium Income: Cboe S&P 500® 2% OTM BuyWrite Index; Autocallable Income: MerQube US Large Cap Vol Advantage Autocallable Index. MerQube US Large Cap Vol Advantage Autocallable Index is not a proxy for Calamos Autocallable Income ETF (CAIE). The results of the MerQube index will differ to those of CAIE. Investors should consider the risks of investing in CAIE and review the prospectus prior to investing. Performance data quoted represents past performance, which is no guarantee of future results. Current performance may be lower or higher than the performance quoted. The principal value of an investment will fluctuate so that your shares, when sold, may be worth more or less than their original cost.

Autocallable notes have specific structural features that may be unfamiliar to many investors:

–Contingent Income Risk: Coupon payments from the Autocalls are not guaranteed and will not be made if the Underlying Index falls below the Coupon Barrier on observation dates. This means the Fund may generate significantly less income than anticipated during market downturns.

–Early Redemption Risk: Autocalls in the Portfolio may be called before their scheduled maturity if the Underlying Reference Index reaches or exceeds the Autocall Barrier on observation dates. This automatic early redemption could force reinvestment of that portion of the portfolio at lower rates if market yields have declined.

–Barrier Risk: If the Underlying Reference Index falls below the Protection Level Barrier at the maturity of an Autocall in the Portfolio, that portion of the Portfolio will be fully exposed to the negative performance of the Underlying Reference Index from its initial level. This conditional protection creates a binary outcome that can result in sudden, significant losses if barriers are breached.

Weighted Average Coupon: The weighted average coupon of all autocallables as of last operation date

Total return assumes the reinvestment of income. Current performance may be higher or lower than the performance data shown. Yield represented by trailing 12 month yield for: Autocallable Income: MerQube US Large Cap Vol Advantage Autocallable Index. MerQube US Large Cap Vol Advantage Autocallable Index is not a proxy for Calamos Autocallable Income ETF (CAIE). The results of the MerQube index will differ to those of CAIE.

SRP Americas Awards Methodology: SRP typically conducts a comprehensive market survey involving institutions active in the structured products space. Industry professionals—including issuers, distributors, and service providers—are invited to vote on various award categories. For the “Most Innovative Product” award, the evaluation likely focuses on: product design originality, client-centric innovation, market impact and adoption, risk-return profile enhancements and integration of new technologies or strategies. Finalists are often reviewed by a panel of SRP editors and industry experts who assess the submissions based on qualitative and quantitative factors.